Zoom Q3 Earnings: A slowdown in the upward way?

$Zoom(ZM)$ reported results for the third quarter of fiscal 2025 (ended October 31), despite a strong quarter and elevated guidance.The company's shares still pulled back after hours, with investors slightly concerned about the challenging overall market environment.

But Zoom's shares have also rallied more than 40% since their lows.

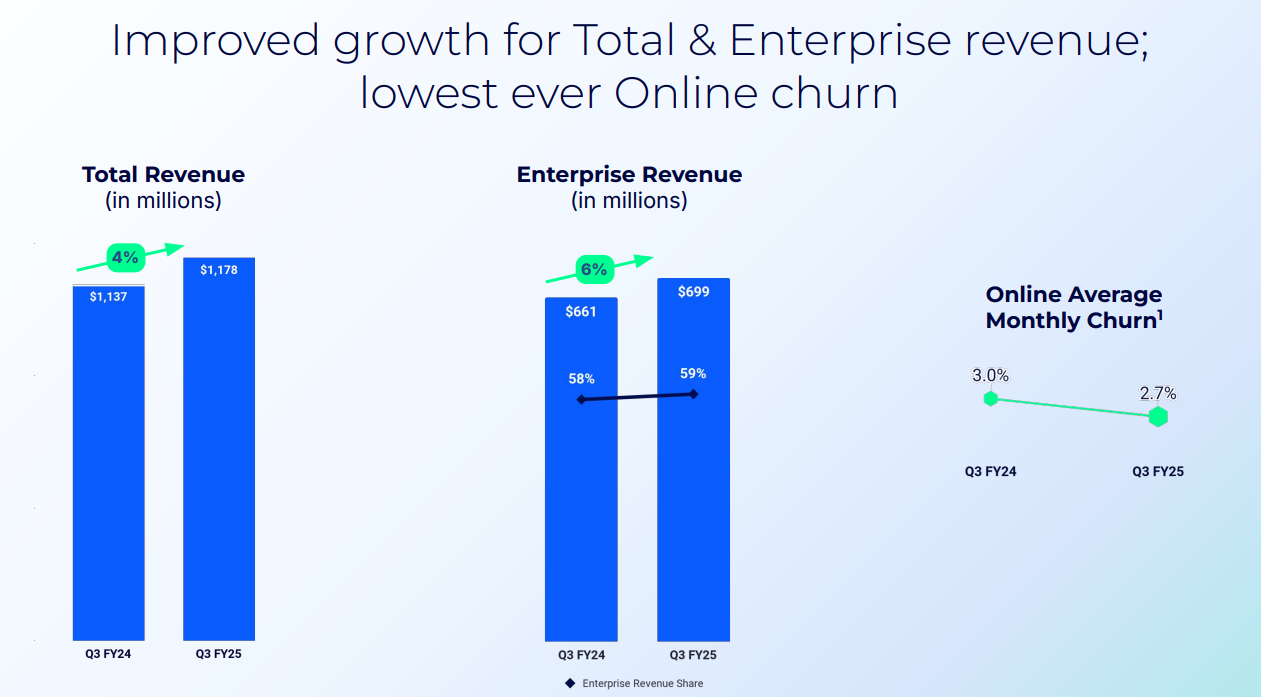

Zoom reported total revenues of $1,177.5 million for the third quarter of fiscal 2024, up 3.6% year-over-year, beating analysts' expectations of $1.16 billion.

The Enterprise business was a particularly strong performer, with Enterprise customer revenue up 8% year-over-year to $661 million, benefiting from steady demand from SaaS customers.Despite a slowdown in overall user growth, the predictable revenue streams offered by enterprise customers make Zoom attractive in an uncertain economic environment.

New products such as Zoom Phone and Zoom Contact Center are also showing strong market demand, with the former having more than 7 million paying subscribers and the latter growing its customer base.These new businesses provide new growth drivers for the Company's future development.

Future Outlook.

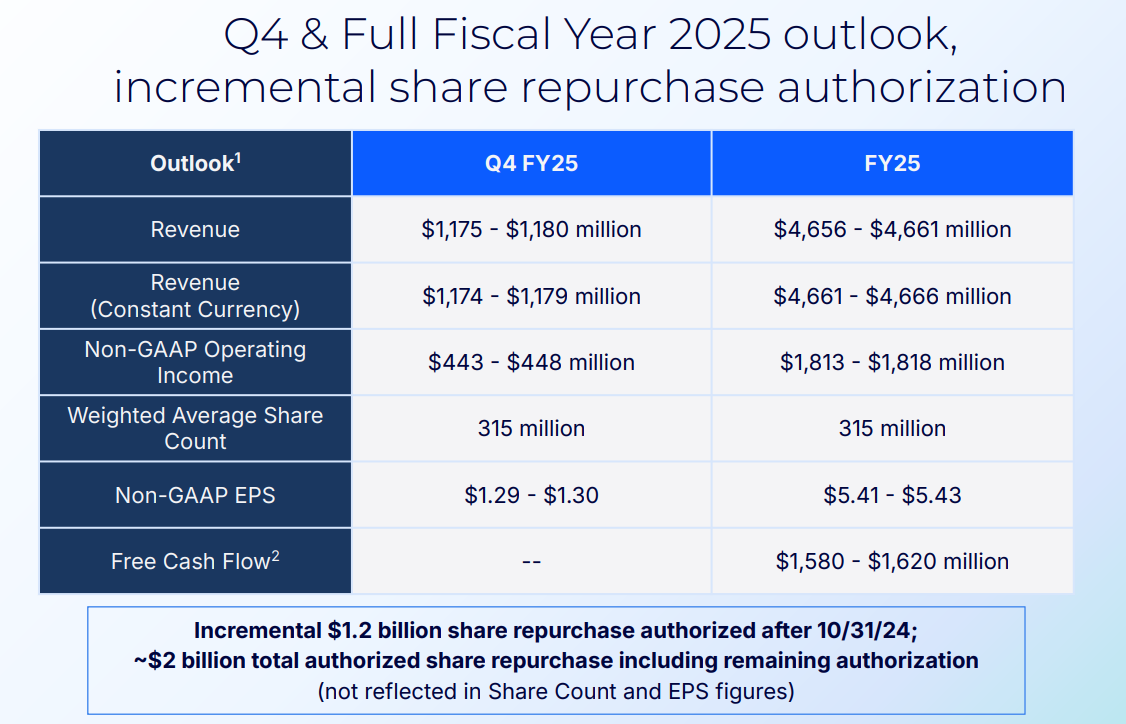

Looking ahead, Zoom's management raised its revenue guidance for fiscal 2025 upwardly revised its revenue guidance for fiscal 2025 and expects to realize approximately $4.65 billion to $4.66 billion in revenue.They emphasized a continued focus on innovation and product development to meet market demand and enhance profitability.This guidance reflects management's confidence in the future development of the business and shows that the company has achieved some success in controlling costs.

Despite Zoom's favorable results in the third quarter, there were a number of factors that fell short of expectations.

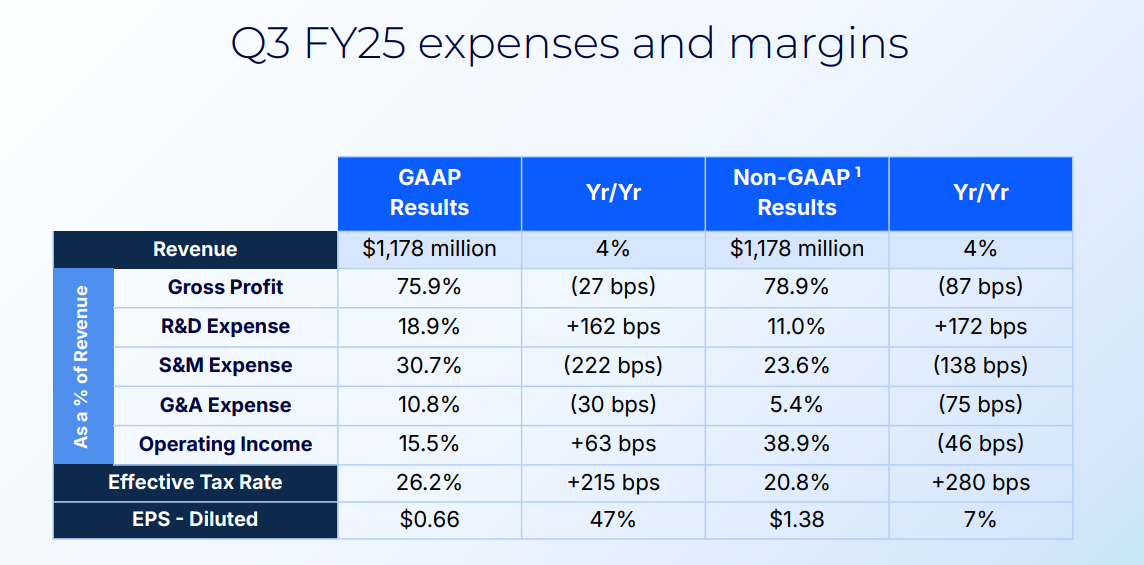

First, the company's online customer churn rate declined slightly year-over-year, but remained at a high of 3% per month, and net dollar expansion for enterprise customers declined from 109% to 105%, indicating slower growth in customer spending.The company said that the stability and long-term contracts of its corporate customers are helping to mitigate this issue, and it plans to further reduce churn through enhanced customer service and support.

Secondly, uncertainty in the macroeconomic environment and pressure on IT budgets could also affect the company's long-term growth potential.Management mentioned that the lengthening of the sales cycle for new customers as well as the shortening of the billing cycle for existing customers may affect the stability of future revenues.

In addition, the market acceptance of new products such as Zoom Phone and Contact Center will have a direct impact on the company's growth prospects.Currently, Zoom Phone has over 7 million subscribers and Contact Center is attracting an increasing number of corporate customers.Management emphasized that these new products provide new revenue streams for the company and will continue to drive future growth.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- ChrisColeman·2024-11-26Great insights on Zoom's earnings! [WOW]LikeReport