What causes Adobe's -22% YTD Performance?

$Adobe(ADBE)$ announced its Q4 FY24 results on December 11th, and while the quarterly results remained strong and exceeded market consensus expectations, particularly in the areas of digital media and digital experience, investors' expectations for the AI era have also risen even further.

But the beauty is that the company's guidance for 2025 is less than what the market expects, partly because expectations have been plucked so high, and partly because the company's caution could make investors skeptical of the company's AI transformation strategy and one of the monetization capabilities that could arise from competing with emerging AI companies, as well as OpenAI's Sora.Hence the 8% after-hours plunge.

Adobe is also one of the few companies that has benefited from AI plus but has had negative returns so far this year.

The company's valuation is also relatively inexpensive at the moment, and the guidance could also put pressure on the 2025 trend.

Financials versus market expectations

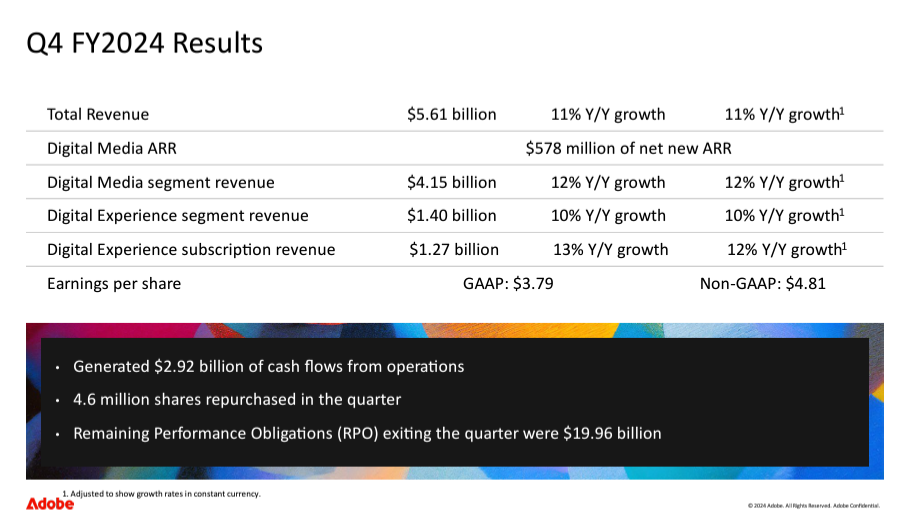

Adobe reported its Q4 financial results on November 29, 2024, and the numbers show:

Revenue: $5.61 billion, up 11% year-over-year, beating market expectations of $5.54 billion

Earnings per share: adjusted EPS of $4.81, also ahead of market expectations of $4.66

Digital Media: Revenue of $4.15 billion, up 12% year-over-year

Digital Experience segment: revenue was $1.4 billion, up 10% year-over-year

Q3 performance exceeded analysts' expectations, particularly in the core business segments of Digital Media and Digital Experience.

Segment business performance

Digital Media: annual recurring revenue (ARR) reached $17.3 billion, slightly ahead of analyst expectations.Revenue, including creative and document processing software, grew 12% year-over-year.

Digital Experience: segment revenue, including marketing and analytics software, grew 10% year-over-year.In addition, the document cloud business grew 18% year-over-year, showing increased user activity

Company Outlook

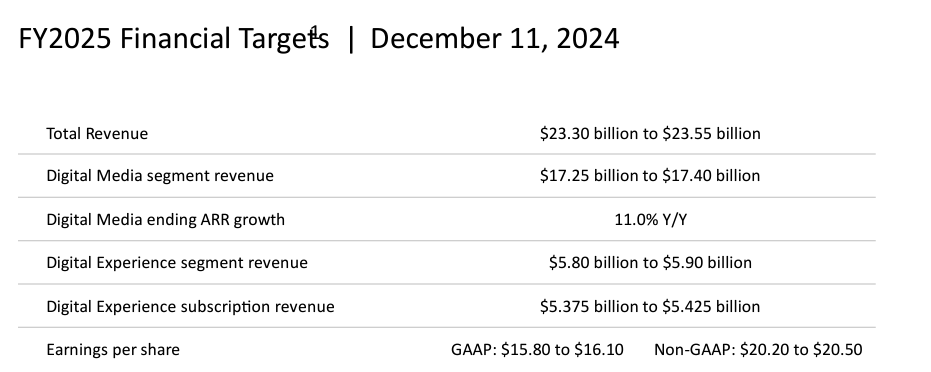

Adobe's revenue guidance for fiscal year 2025 was disappointing, despite fourth-quarter results that beat expectations.

The company expects fiscal 2025 revenue to reach approximately $23.4 billion, below the average analyst estimate of $23.8 billion[2][8].This conservative guidance stems largely from market concerns about the impact emerging artificial intelligence technologies could have on its business.

Adobe's chief financial officer said it will continue to roll out new tiered subscription services and add-ons to drive future revenue growth.This strategy is aimed at increasing user stickiness and expanding market share.

Analysis of the reasons for the performance variance

Reasons why we were able to continue to exceed expectations in the current quarter

Strong Demand: Adobe's Creative Cloud, Document Cloud and Experience Cloud are playing a key role in driving the AI economy, and customer demand for its products continues to grow.

Innovative products: the company's innovations in generative AI, such as the Firefly platform, have enhanced the competitiveness of its products and attracted more users

Reasons for missing expectations

Conservative future guidance: Revenue expectations for FY2025 were lower than market expectations, raising investor concerns about the company's future growth potential.

AI competition and market concerns

The AI disruptor vs. disrupted debate:

With the development of AI technology, Adobe's positioning in the market has sparked a hot debate.On the one hand, there is the view that Adobe could be disrupted by emerging AI startups; on the other hand, there are those who believe that Adobe has launched its own AI products quickly and is equipped to respond.

However, despite Adobe's launch of several AI products, it remains a challenge to monetize these products effectively.

Market expectations of AI profitability:

Investors generally believe that having an AI product means being able to turn a profit quickly, but in reality, it's not easy for the software industry to turn a profit in the AI space. it will take time for Adobe to explore the monetization path for its AI products, which is closely related to the changes in its SAAS sales model

Comparison with Sora:

Since the rise of the AI trend, Adobe has oscillated between the roles of "AI disruptee" and "AI disruptor", and the comparison with Sora has gotten a lot of attention.The user doesn't think Adobe will be the "disrupted" because it's moving fast and has its own AI products to deal with it, but also doesn't think Adobe can quickly become a "disruptor" due to AI because the path to monetizing AI products isn't easy.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- WalterD·12-12Investors seem nervous about Adobe's AI monetization strategy.LikeReport