All About Stock Crash: US Exceptionalism, Stagflation, and A Safe-Haven Asset

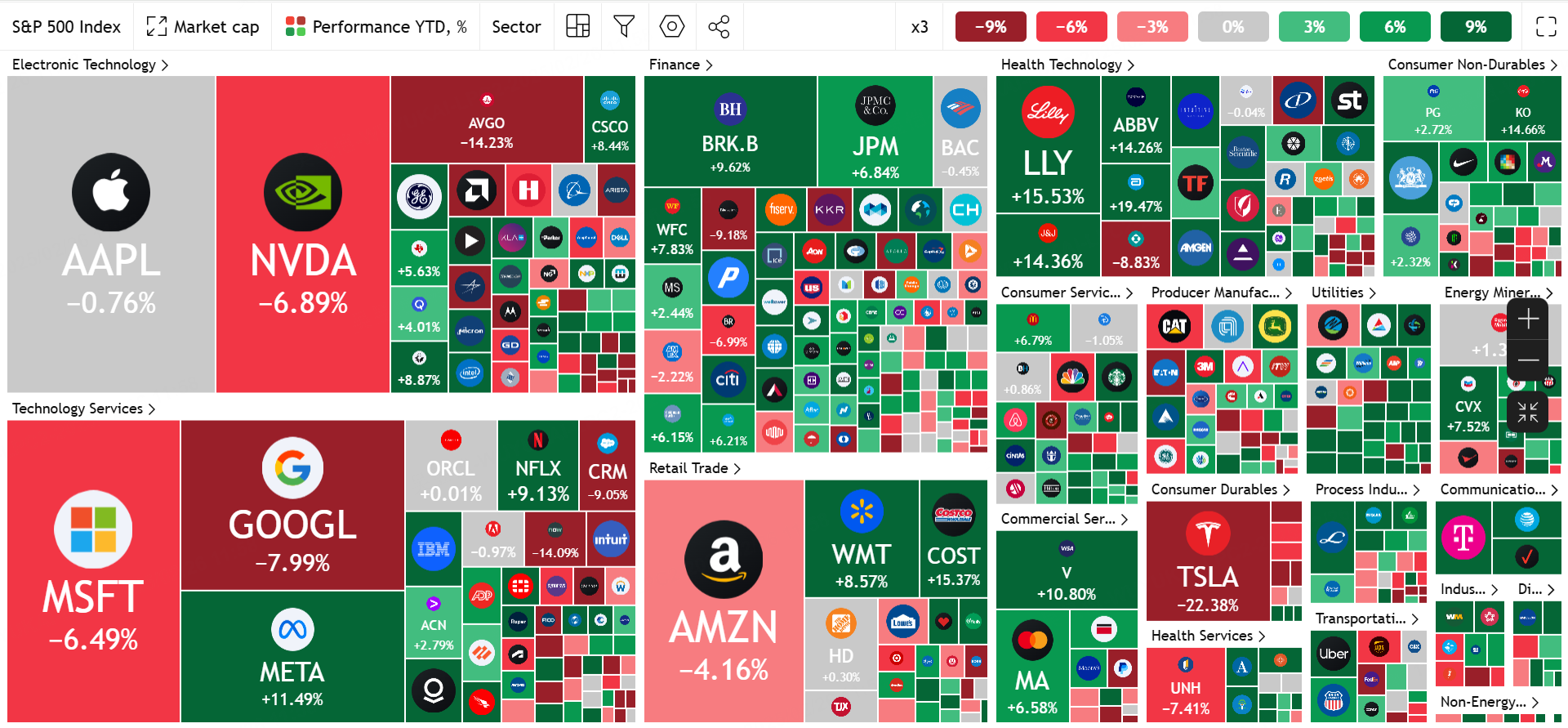

The pullback in U.S. equities has extended from highly valued growth stocks (e.g. $Palantir Technologies Inc.(PLTR)$ $AppLovin Corporation(APP)$ .) into the larger $NASDAQ 100(NDX)$ broader market range.

In the Mag 7, only $Meta Platforms, Inc.(META)$ has closed higher year-to-date, while $Tesla Motors(TSLA)$ with both fundamental and policy risks, has pulled back more than 22% on both performance risk and policy risk.

In contrast, $S&P 500(.SPX)$ has been less volatile, with significant movement between sectors, also stemming from risk aversion.

Even $Apple(AAPL)$ among tech stocks has been a risk aversion in the absence of bright spots.

Can "U.S. exceptionalism" be supported for how long?

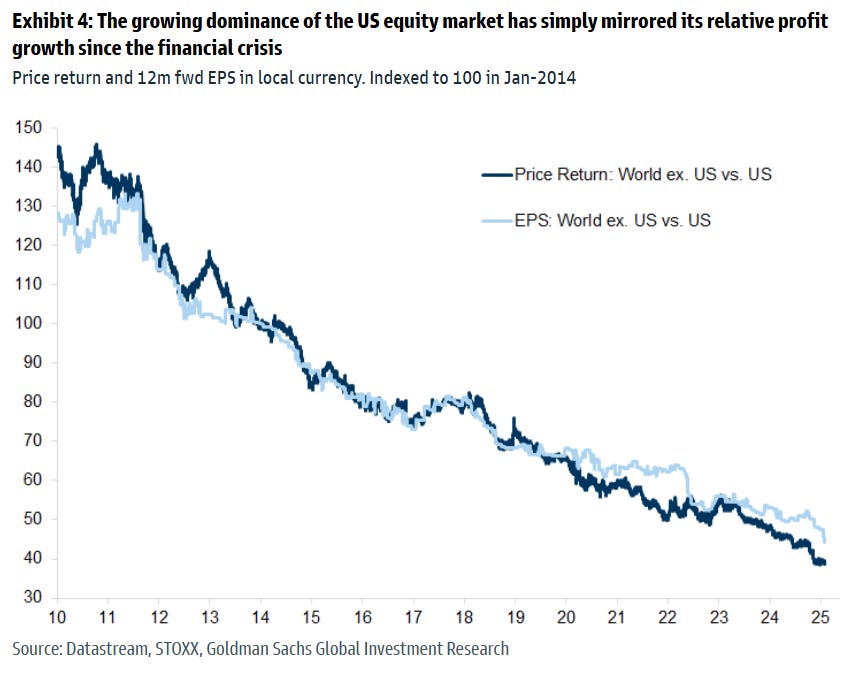

The U.S. technology sector, with its superior profitability and high growth rate, has supported the U.S. market's earnings growth at a rate far exceeding that of other countries.As a result, it has been an "outperformer" in the secondary market.

Concentration is too high a risk.The high concentration of US equities, the technology sector and the dominant Magnificent 7 stems from strong historical fundamentals, but can make the overall market vulnerable and increase volatility on pullbacks (consistent trading).

A recent study by BofA suggests that investor confidence in the "US Exceptionalism" is waning, mainly in light of recent signs of geopolitical turmoil and uncertainty.

With DeepSeek as the trigger, U.S. exceptionalism is beginning to fade and international equities could be the best performing asset in 2025. While the U.S. market could rise further, the report suggests that its exceptional earnings growth will moderate, creating opportunities to diversify into other regions.

Intersector flows stem from risk aversion

One source of uncertainty: Trump's faster-than-expected policy pace.Since his inauguration, the policy sequence has been "tariffs first, tax cuts later, saving money first, spending money later", and the headwind policies with austerity effects have been the first to come into force intensively, which has had an impact on business and consumer confidence.

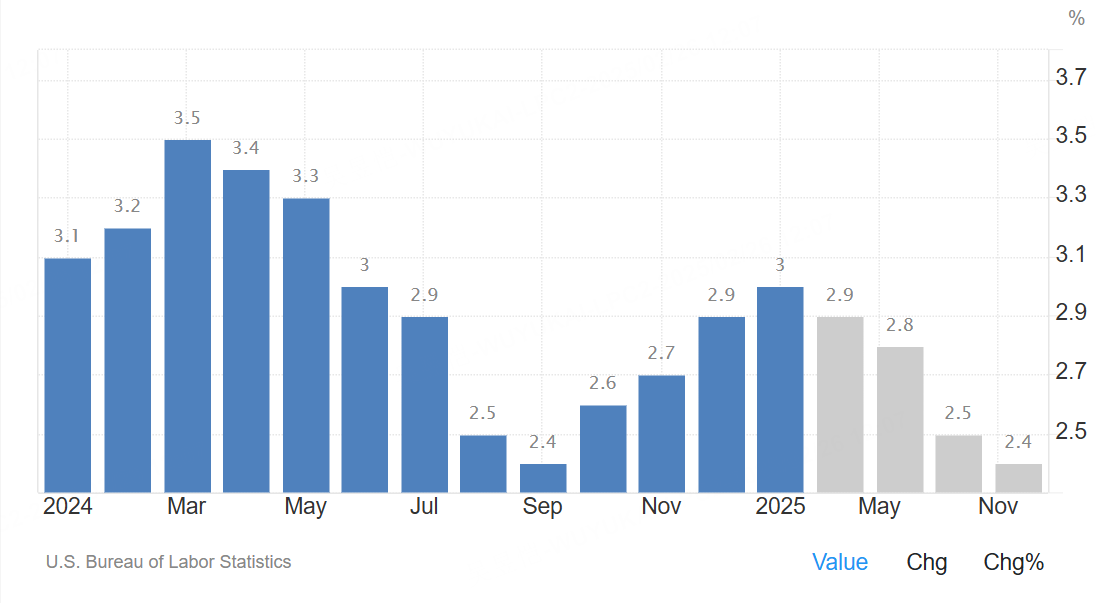

Stagflation concerns: its policy mix (trade protection + fiscal contraction) may exacerbate the downward pressure on the economy, while tariffs push up commodity prices, forming a self-reinforcing cycle of "low growth + moderate inflation"; recent CPI, consumer confidence and other data are also on the weak side;

Elon Musk's DOGE department has pushed forward with a federal employee "buyout program" (layoffs), and the DOGE cuts are not large, but government layoffs could have a knock-on effect on the job market.

Diversification is the key to hedging.

For now, the recent market decline is viewed as a correction, not a bear market; tech stocks are overpriced and vulnerable to disappointment.

Diversification across asset classes, geographies, sectors and investment styles has instead improved risk-adjusted returns.Specifically , "Russia-Ukraine truce", "Europe's autonomous defense", "China's DeepSeek-led tech boom", hawkish expectations of Japan's CPI rebound, are all becoming better places for money to go.

East rises, west falls discussion

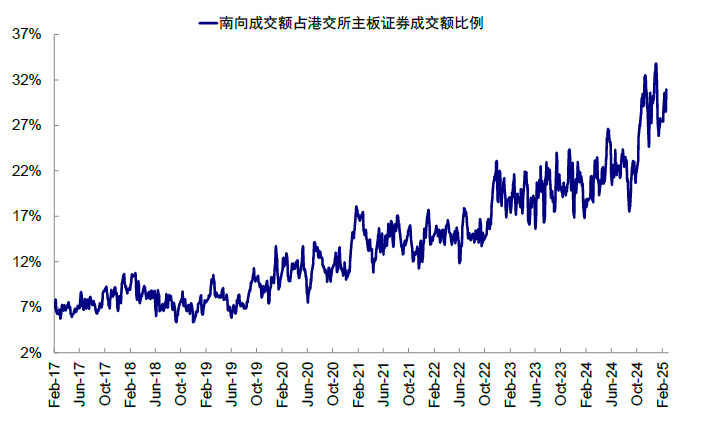

Chinese equities $HSI(HSI)$ have significantly outperformed the S&P 500 and European equities in February.

The trigger was AI: while the market currently expects the actual impact of AI on China's corporate earnings to remain limited, investor visions of this have driven valuation revaluations (changes in risk premiums) in related stocks;

Fund flows are not yet fully reflected: the gains in HSCEI were mainly driven by southbound funds.Foreign flows into mutual funds and ETFs in the Mainland China and Hong Kong markets are inconsistent with the positive signals; inflows are still dominated by trading and passive funds, with active outflows narrowing;

$HSTECH(HSTECH)$ is now entering a technical "bull market", but with a narrow upward range, driven by a handful of individual stocks in the technology sector and with low dependence on the macro environment.

Three major event nodes expected: two sessions, tech earnings (guidance), Trump's visit to China (tariff talks)

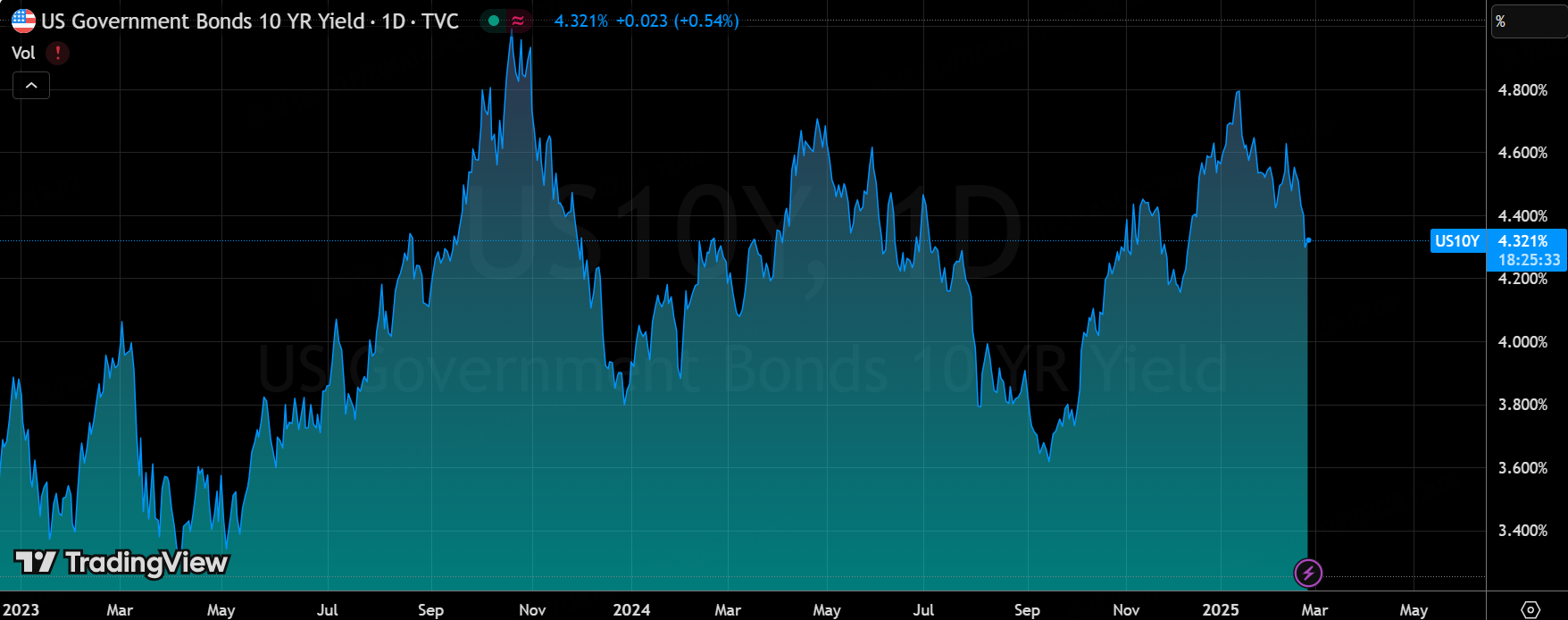

A Safer Assets

First, the U.S. economic outlook concerns can be more reflected in the bond market, $iShares 20+ Year Treasury Bond ETF(TLT)$ $US10Y(US10Y.BOND)$

Secondly, the current concern about "inflation" has turned into a concern about "stagflation", which will further promote the Fed's interest rate cut expectations; and on the corporate side, the representative Walmart's profit warning has also strengthened the concern about the lack of economic growth.

From the trading side, risk assets retreated, conceptual themes were weak (e.g., Trump trading), and the dollar, digital currencies, etc. all performed very poorly. $USD ETF - PowerShares DB (UUP) $ Bitcoin (BTC.USD.CC)$

The current short-term view on the 10-year U.S. bond could hit the 4.15% level, which could stabilize after some of the uncertainty settles in, but is still in a continued downtrend.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- pixiezz·2025-02-26High risk hereLikeReport