JD’s Q1 Shines, But New Biz Loses, Food Delivery Drags?

$JD.com(JD)$ Q1 results overall exceeded expectations, but growth relies on policy dividends and new business investment increases uncertainty.High shareholder returns provide a safety cushion, but need to be wary of takeaway & logistics drag.Neutral rating, awaiting clearer medium to long term guidance. $JD-SW(09618)$ $JD LOGISTICS(02618)$

Performance and Market Feedback

Core performance overview

Key Operating Metrics

Self-operated e-commerce growth driven:

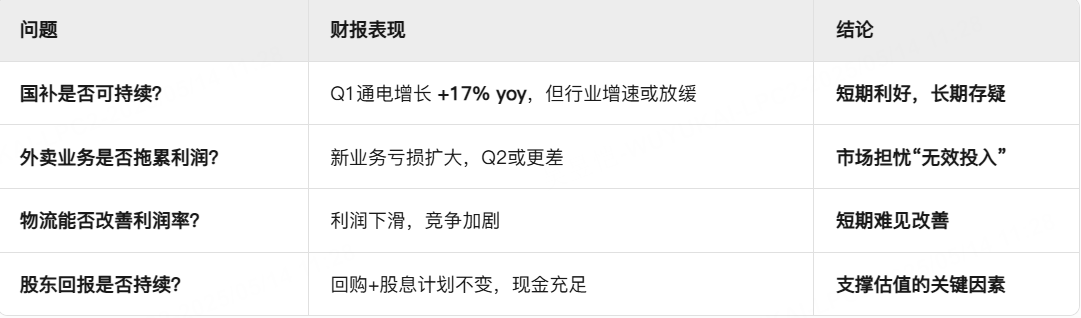

E-commerce products (home appliances/3C): revenue +17% yoy (~50% share), benefiting from the "national subsidy" policy stimulus.

General merchandise (supermarket category): revenue +15% yoy, cross-selling effect.

Gross margin improvement: overall gross margin 15.6% ( +0.3pct yoy ), mainly due to state subsidies to reduce platform subsidy costs.

Expense control:

Marketing expenses: +14% yoy (below revenue growth).

Administrative expenses: +24% yoy (due to new business expansion).

Logistics expenses: +18% yoy (higher than logistics revenue growth).

Profit distribution:

Jingdong Mall: operating profit ¥12.6B ( +38% yoy ), margin 4.8% ( +0.8pct yoy ).

Jingdong Logistics: operating profit ¥1.5B ( -32% yoy ), margins dragged down by increased competition.

New business: loss ¥1.33B (widened yoy), increased investment in takeout.

Market Feedback

After-hours share price: +3% after earnings (market recognizes profit beat), but retreats to +1% after opening the next day (concerns about widening losses from new business).

Investor sentiment:

Optimism: Revenue & profit growth driven by state subsidies, shareholder returns (buybacks + dividends) support valuation.

Points of concern: ① the sustainability of national subsidies in doubt; ② takeaway business losses may be further expanded; ③ logistics margin decline.

Investment highlights

1. Core growth: driven by state subsidies, but the continuity is doubtful

State subsidy policy is the biggest catalyst in Q1: government subsidies to reduce the selling price, stimulate sales, and not counted in the cost of Jingdong, directly pushing up gross margins (Mall gross margin +0.6pct yoy ).

But the policy dividend or difficult to sustain:

Semiconductor Manufacturing International's (SMIC) recent guidance shows a slowdown in growth in the communications/IoT industry, which may affect subsequent pass-through demand.

If the state subsidies to withdraw, Jingdong need to pay for subsidies to maintain growth, profit margins may be under pressure. 2.

2. Takeaway new business investment increase, the market is worried about "ineffective volume".

Takeaway business strategic significance: Jingdong APP low-frequency (rely on electricity products), takeaway can enhance user activity, but the difficulty of profitability (the United States only low single-digit profit margin).

Q1 has seen losses widen: new business loss ¥1.33B (worsening y/y), market expects Q2 losses to widen further.

Key issue:

Scale of investment: the annual budget of the conference call is not clear, if it exceeds $1B, it may suppress the profit expectation.

The effect of infusion: if it fails to effectively increase the repurchase of e-commerce, it may be regarded as "burning money without return".

3. Logistics segment: revenue growth but declining profit margins

Revenue: +13% yoy (Dada contributed to the growth rate), but operating profit -32% yoy.

Competition intensifies: rivals such as Gigabit and Shunfeng cut prices, and Jingdong Logistics may need to increase subsidies to protect its share.

4. Shareholder returns: high dividends + buybacks to support valuation

2025 Plan: Dividend: $1.5B (~3% annualized return).Buybacks: $1.5B used ($3.5B remaining), $4B expected for the year (~7% annualized return).

Cash reserve: net cash $22B, sufficient to support current repo pace.

Valuation anchor: current 8x PE, limited downside if maintain 10% shareholder return.

5. Market's previous concerns & call answers

6. Valuation & Market Sentiment

Short-term (1-2 quarters) catalyst: if state subsidies continue and takeaway investment can be controlled, share price may be repaired to 10x PE. risk: if takeaway loss exceeds expectation, market may reprice.

Medium and long term key observation points: ① natural growth after the withdrawal of state subsidies; ② takeaway business flow effect; ③ logistics competition pattern.

Valuation logic: the current 8x PE has reflected the growth concerns, but if the new business drags down profits, the valuation may be further pressured.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- EVBullMusketeer·2025-05-14It was definitely affected by the price war with Meituan.LikeReport

- predator007·2025-05-14It's wise to remain cautious.LikeReport