💸 Premium Revenue Up 5%, Fuel Costs Down 11%: Delta's Profit Magic Trick

$Delta Air Lines(DAL)$ demonstrated industry-leading operational and financial performance in Q2 2025, with premium growth and cost control delivering solid profitability despite lower guidance.EPS beat estimates and shares rose 11% reflecting market recognition of its Q2 performance. $United Continental(UAL)$ $American Airlines(AAL)$ $Southwest Airlines(LUV)$ $Alaska Air(ALK)$

Performance and market feedback

Key financials vs. market expectations

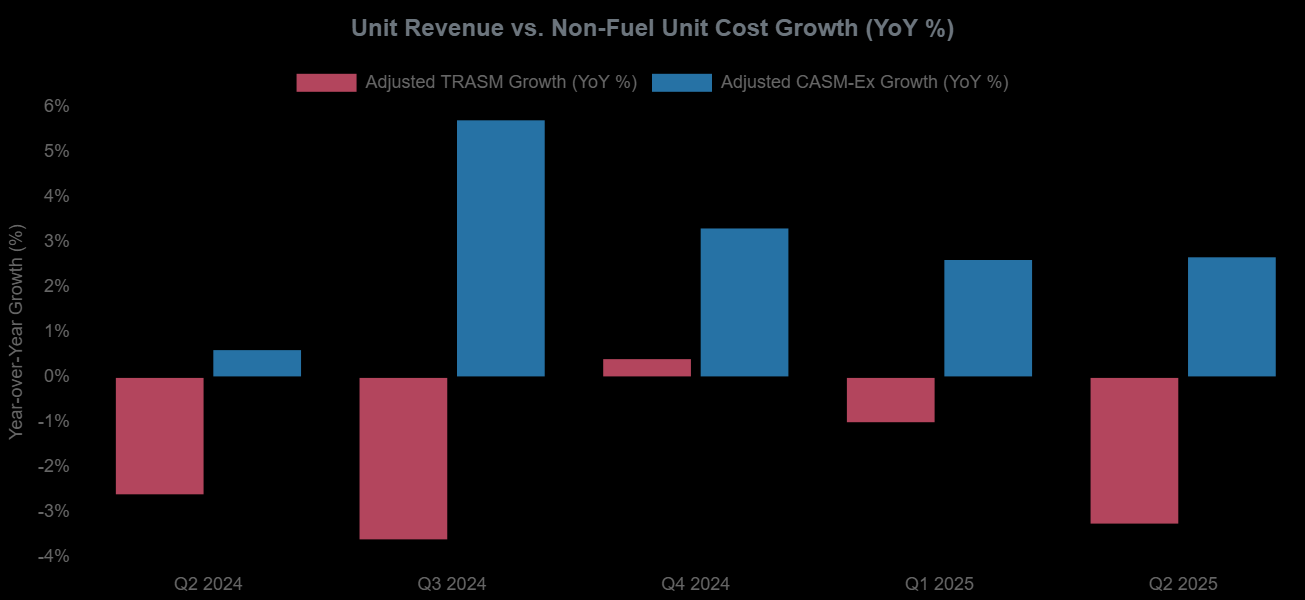

Revenue was $15.5 billion (non-GAAP), up 1% year-over-year ($15.35 billion in Q2 2024) and above market expectations of $15.44 billion.The market had previously lowered its estimates, though revenue growth was limited by a 3% decline in unit revenue (TRASM)

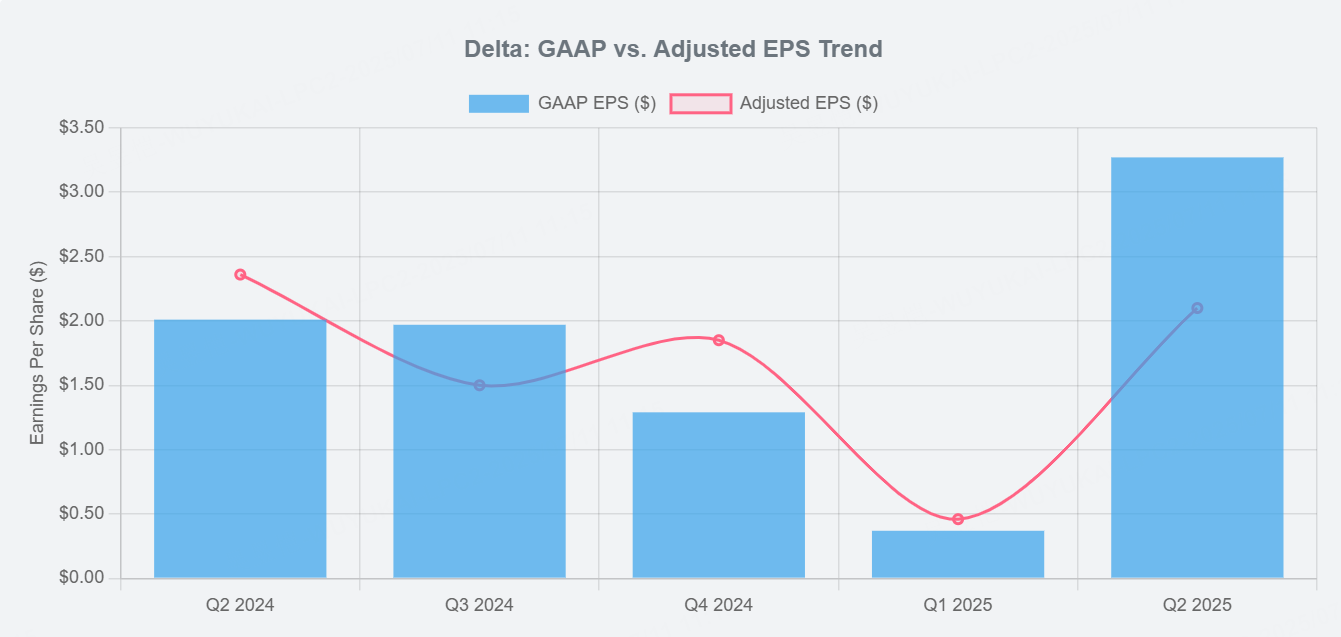

Adjusted earnings per share (EPS) of $2.10, down ~11% year-over-year ($2.36 in Q2 2024), but slightly ahead of the market's estimate of $2.07. GAAP EPS of $3.27 was impacted by a one-time gain.

GAAP operating margin was 12.6% and non-GAAP was 13.2%, demonstrating strong profitability and outperforming industry averages.

Non-GAAP free cash flow of $733 million, with the company still generating significant cash flow after capital expenditures

Cost structure: non-fuel CASM up 2.7%, fuel expense down 11%, average fuel price of $2.26/gallon, down 14%.

Ancillary businesses: strong growth in loyalty revenue (+8%), cargo revenue (+7%), and MRO revenue (+29%) provided Delta with a diversified revenue stream.

The company announced a 25% increase in its quarterly dividend and an annual dividend commitment of approximately $500 million

Share price performance and investor sentiment

Delta shares rose 11% after the earnings report and drove other airline stocks higher, with market feedback on its Q2 performance being more positive, but mainly due to the fact that previous expectations were really low, as well as downward revisions to full-year guidance reflecting concerns about tariffs and weaker consumer demand.that could limit upside.

Investment highlights

Revenue growth constrained but structurally optimized with stable high-end demand

Revenue growth was limited by a 3% decline in total adjusted revenue units (TRASM), linked to weak consumer demand and fare pressure.However,, despite capacity growth of 4% and strong performance in premium markets and ancillary businesses:

Premium revenue grew 5%, with demand for premium travelers remaining strong.

Loyalty revenue grew 8%, with the card partnership with American Express bringing in over $2 billion, up 10%, as the loyalty program (SkyMiles) continued to demonstrate its attractiveness.

Revenue diversification was also supported by 7% and 29% growth in the cargo and MRO businesses, respectively.

Growth in higher margin businesses helped Delta offset lower unit revenue

Cost Control and Profitability

Q2 saw an excellent performance in cost management, with non-fuel unit costs (non-fuel CASM) increasing 2.7% to 13.49 cents, slightly above inflation but in line with 4% capacity growth, with fixed costs effectively spread.

Fuel costs declined 11% to $2.5 billion and average fuel prices fell 14% to $2.26 per gallon, boosting profitability.

Incidentally, Delta's operating margins (non-GAAP 13.2%) and pre-tax margins (non-GAAP 11.6%) are industry-leading

Full Year Guidance Reduction and External Challenges

Delta lowered its full-year 2025 adjusted EPS guidance to $5.25-$6.25 from $7.35+, reflecting the impact of tariff policies and weak consumer demand.Company executives said bookings have stabilized after a drop in demand in early 2025, but are lower than expected at the start of the year.

Q3 2025 EPS guidance of $1.25-$1.75 is slightly below Wall Street's expectations of $1.31. Delta is cautious about growth in the coming quarters, which could affect the market's repricing of its valuation.

Key Takeaways from the Conference

Capacity & Demand Management: Industry proactively contracted capacity to match demand, Delta responded to economy class weakness by adjusting flight schedules and network optimization, premium market remains core to growth.

Technology and Strategic Investment: Accelerating the implementation of AI technology (e.g. Fetcherr) to improve operational efficiency, while deepening cooperation with American Express to consolidate loyalty program revenue.

Financial & Capital Allocation: Prioritize debt repayment and increase dividend, cash usage is on the robust side, optimistic about consumer confidence, but wary of demand divergence in some industries.

Risk response: Mitigating external pressures such as tariffs and fuel through cost control and supply chain negotiations, showing strong confidence in Q4 and long-term performance.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- FranklinMorley·07-11Wow, such impressive results from Delta! [WOW]LikeReport

- snappyz·07-11Great performance! 🌟LikeReport