Some important reasons of Netflix's Q4 tumble

What makes $Netflix(NFLX)$ a 20% slide after the Q4 earnings?

Summary

- A real miss on paid subscribers, and new season's price rise could be catastrophic. With the high inflation, price of service is under pressure;

- Fierce competition makes the streaming content company anxious, excellent content reachesthe bottlenecks. With more users accepting video content, it is easier to get tired. The more popular the "squid game" is, the less quality content appears;

- Mixed financial outlook, a miss on "break-even point".Cash flow from operating activities turns negative again, and the capital expenditure on content is for dramas on the one hand and game business on the other. the annual target of free cash flow break-even point hardly meet. Content expenditure too large, with other costs rising too fast, but difficult to pass it on to users;

- Change of market style, growths are unpreferred, and the market is mean to growth stocks. If a goal is not achieved, it may be simply judged as "Missed". Bulls and bears are not in balance, market has been bearish on Netflix's growth.

A plummet of 20% by such a top technology company is not easy to seen, since $Meta Platforms, Inc.(FB)$ 's Q2 earnings in 2018. Shall the reported American technology giants become the benchmark again?

Obviously, Netflix's financial report is very critical.(In the previous financial report outlook, we stressed the importance of this earnings, click to view)

From the perspective of company operation, Netflix has two short-term intractable problems.

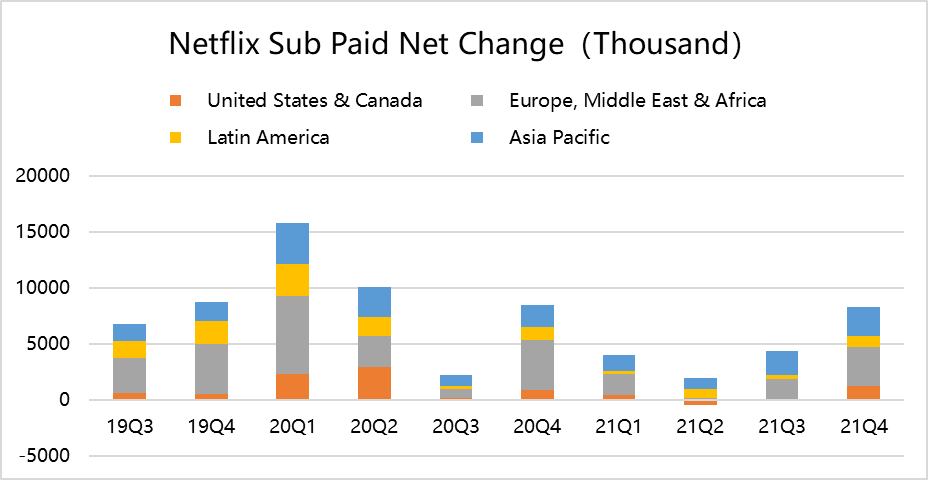

First, new paid subscriptions are expected to decline.

This new user is originally an incremental value. As long as the incremental value is positive, it means that the growth continues.

But the question is whether Netflix can continue to retain users after the pandemic?

Because the growth of users has a ceiling, the population.

The main regions of growth are Asia-Pacific and EMEA, especially the former. In other words, developing countries have made great contributions. In developed countries, it is somewhat weak, People who are interested in streaming media and can afford it should have bought it almost.

It is not surprised that miss the expectations. There are two ways to compare.

ONE, is the comparison between the actual and the analyst's Consensus.

The estimates are different among analysts, and they also change their expectations constantly, this expectation consensus is just an average.

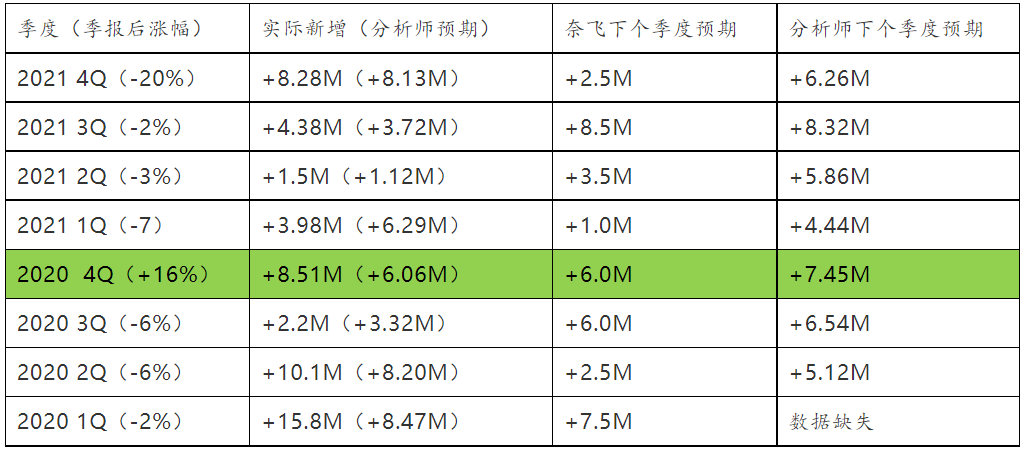

For example, analysts' consensus on 21Q4 was to increase by 8.32 million at the 21Q3 earnings release, but soon before 21Q4 earnings, the consensus had dropped to 8.13 million.

So, when actual result is an increase of 8.28 million,just between the two expectations. it is difficult to judge whether meet or miss, but at least within the range.

TWO. Comparing between the actual and the company's guidance.

Netflix will give guidance for the next quarter every quarter. In 21Q3, Netflix's guidance to Q4 was to add 8.5 million yuan, and the actual value of 8.28 million, obviously less than guidance.

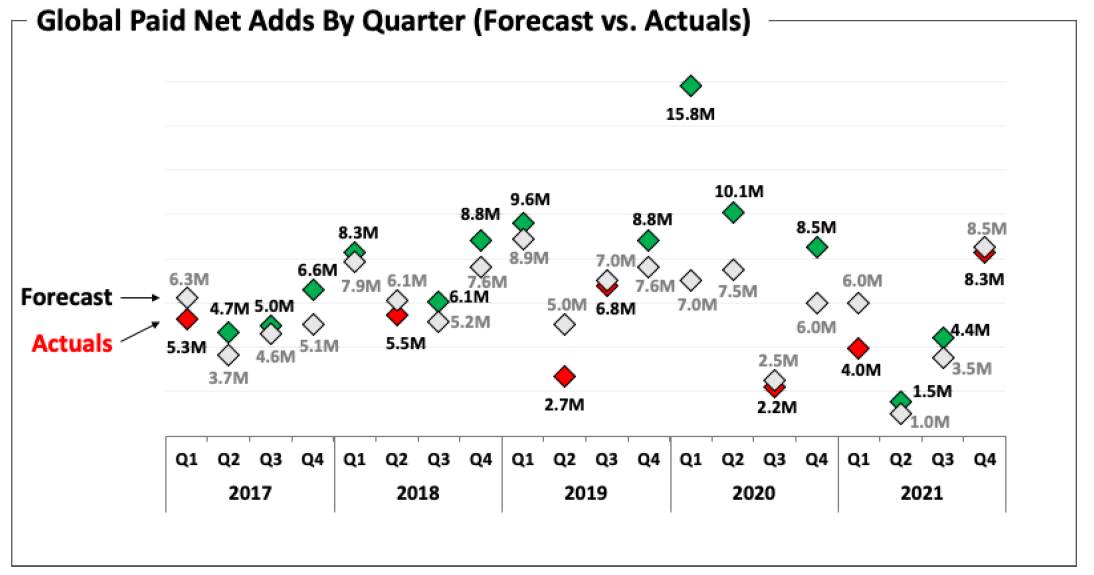

Most of time, the actual value can exceed the company's guidelines.

Therefore, Netflix lowered the guidance of 22Q1 to 2.5 million, which is also lower than the minimum estimate among analysts,

Second, content anxiety makes it more and more difficult to attract users.

Movies and TV Series are not always excellently attractive, it's the rule of industry, even Hollywood has "Small Years". But as streaming media,a longtime "content shortage", you may lose users.

"Squid Game" did make the popularity in Q4,

But it just demonstrates the shortage of popular classic dramas in the current environment. If large numbers of Netflix's new dramas are excellent , there will be no extremely popularity.

This problem is not only faced by Netflix, but also by streaming media content producers like, $Walt Disney(DIS)$, $Comcast(CMCSA)$ .

From the perspective of financial report, Netflix is far less glamorous than it seems.

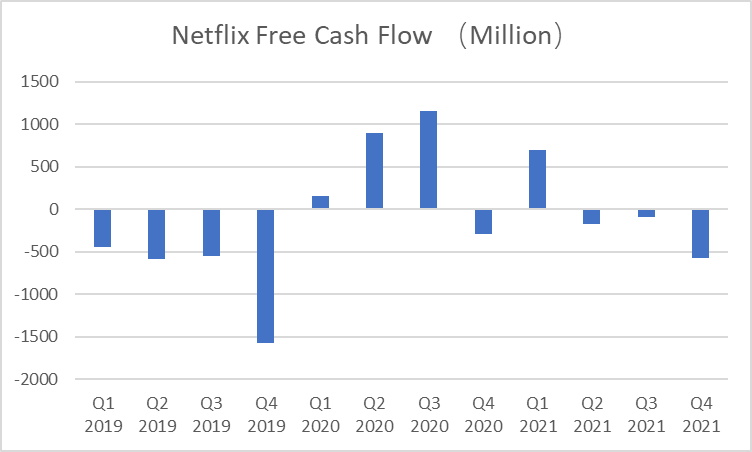

We also mentioned in Q3 that Netflix's profit can't just define by the income statement, its biggest expenditure, content expenditure, is not included in income statement, but in the cash flow statement.

The net cash flow from operating activities, excluding the impact of the pandemic, gradually turns"positive" until 21Q3 of 82.4 million.

However, due to the increase of content cost, the net cash flow from operating activities turned again into a loss of 403 million, directly led to the annual FCF of negative 158 million, which actually did not meet the company's previous goal of "Approximately Break-even".

Therefore, only looking at Q4's EPS of $1.33, slightly exceeding the expected EPS of $0.81, does not mean a beat.

Besides,the gross profit margin and operating margin in 21Q4 have also dropped.

Gross profit margin is due to increased amortization of content costs. Of course, there are also factors such as the rising cost of infrastructure such as broadband; Net interest rate is the increase of marketing and management costs.

This is easy to understand, under inflation, all the costs rise, For example, the cost of filming dramas and advertising costs increase, the wages increase, that hurt the profit margin.

More importantly, it is difficult for Netflix to transfer costs to users. Although Netflix raised its price in North America in early January, which is higher than that of its peers, the price increase is likely to also bring about a decline in the number of users (which is one of the reasons why the company lowered the growth of Q1 users), and the price increase that should have brought higher profit margins may not actually cover the upward cost.

While inflation continues, industry involution also continues, and overseas growth of developing country users are more price-sensitive, and the US dollar in the interest rate hike cycle will lead to exchange rate losses. There is not much room for Netflix to continue to raise prices.

From the perspective of the secondary market, growth stocks may experience "dark ages".

The change of market style has begun. Growth stocks are no longer preferred, and the funds are becoming more and more balanced towards value stocks.

(Click to learn about the classification of growth stocks and value stocks)

Netflix is the first big tech collapsed in growth stocks.The market is becoming more and more strict to growth stocks. If a goal is not achieved, it may be judged as "less than expected" and fall sharply.

As a result, the bulls of growth technology companies is getting weaker, the buying and selling power is unbalanced.

For investors, the earnings season is certainly a coexistence of opportunities and risks. Netflix's performance after the earnings may be just a sign of investors' atittude towards the technology stocks, and may also set a tone for the whole earnings season.

Will you buy of Netflix Q4 earning's dip?(Single choice)

Will you buy of Netflix Q4 earning's dip?(Single choice)Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

This is good