Lucid stock crashes:will it be an opportunity?

A lot has happened sinceLucid Group(NASDAQ:LCID)went public in July 2021. Its Air Dream Edition with 520 miles became the longest-range electric vehicle (EV) yet and attracted rave reviews once it hit the roads in late October. With the company also expanding production capacity,Lucid stock rose a stunning 280% in 2021.$Lucid Group Inc(LCID)$

In the past three months, though, the stock has lost more than 50% of its value, partly because of the broader sell-off in growth stocks and largely because of a subpoena from the Securities and Exchange Commission (SEC) in December, regarding its merger with a special purpose acquisition company and unnamed "projections and statements." (There have been no updates on the SEC matter.)

Lucid investors have since pinned all hopes on its fourth-quarter numbers and outlook to help the stock bottom out and rebound. Instead, the earnings report sent the stock plunging even further, with itsshare price dropping 19% at one point this morning.

The big question now is whether Lucid's numbers and outlook warrant such a knee-jerk reaction or has the market overreacted and in doing so, presented you with a golden opportunity to buy the once-hotEV stockbefore it rebounds?

Before you jump to conclusions, here are the most crucial numbers from Lucid that you must know.

Reservations: Lucid had secured more than 17,000 reservations across all of its four models (the Air Dream Edition, Air Grand Touring, Air Touring, and Air Pure) by mid-November. As of Feb. 28, Lucid's reservations exceeded 25,000 units, worth more than $2.4 billion in potential sales.

Deliveries: Lucid started deliveries of the Dream Edition in late October. As of Feb. 28, it had delivered more than 300 units, including 125 units in 2021. Investors had bigger expectations given that Lucid had earlier said it plans to start deliveries of other models only after delivering 520 Dream Editions.

Production: This, by far, is the most important number investors are focused on, because the ability of an EV manufacturer to produce at scale and its pace of production are two of the biggest advantages to have in such a highly competitive industry. Until November, Lucid was confident of producing 20,000 vehicles in 2022 as it ramped up production at its Arizona factory. It now expects to produce only 12,000 to 14,000 units this year as it navigates supply and logistics challenges.

To be fair, Lucid isn't the only EV start-up to fall short of its production estimates.Rivian Automotive(NASDAQ:RIVN), whose debut electric truck has also won accolades, like Lucid's debut electric car, is just one of the other companies to have missed its goals. Also, Lucid isn't the only automaker facing supply constraints.

Importantly, its reservation numbers are strong. Also, during its fourth-quarter earnings conference call, Lucid said that reservations for its second-most expensive model after the Air Dream Edition, the Grand Touring, were higher than its two lowest-priced trim packages. Lucid also confirmed plans to set up a factory in Saudi Arabia,a nation it has strong connections with.

I'd want to believe Lucid is prioritizing quality over quantity when it comes to production right now, and its revenue could grow steadily once the dust settles on the supply chain. As that happens, Lucid's stock could be back in the limelight again.

Besides, I also want to talk about the company's valuation by the way.

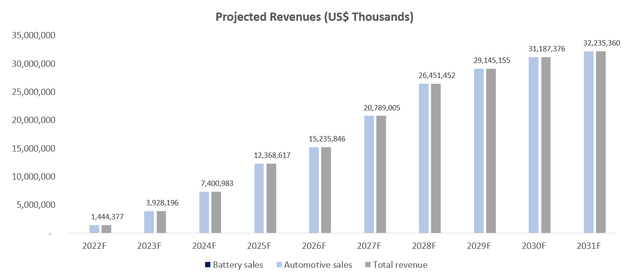

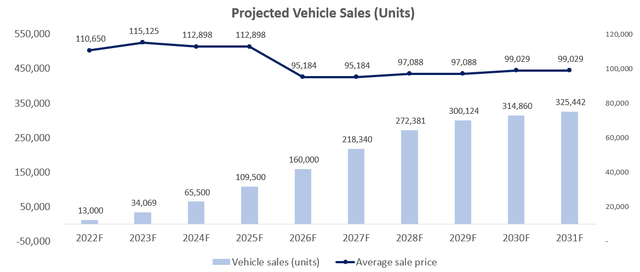

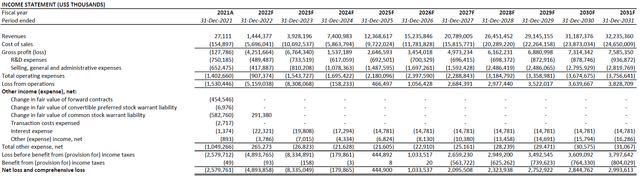

Much of the Lucid's top-line growth will be driven by its core vehicle sales business, which is expected to grow from $1.438 billion (13,000 vehicles) in the current year towards $32.228 billion (325,442 vehicles) by 2031. The growth assumption applied is consistent with market forecasts onglobal EV uptakeover the next ten years as discussed in detail in one of ourearlier coverageson the stock, and also takes into consideration Lucid's refined growth strategy which now prioritizes expansion of its global sales and manufacturing footprint, and product roadmap to acquire additional market share.

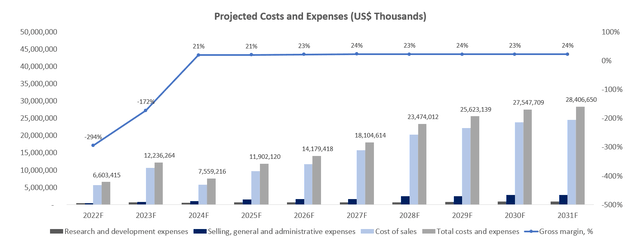

Meanwhile, Lucid's cost of sales and operating expenses are expected to remain elevated until at least 2025 to support the ongoing build-out and production ramp-up of its overseas sales and manufacturing capabilities, respectively. Specifically, current year cost of sales is expected to remain largely consistent with trends observed in 2021, as Lucid Air sedan productions continue to ramp at its Casa Grande manufacturing facility in Arizona, while logistic costs remain elevated in the near-term due to supply chain disruptions. Our base case forecast expects gross margins to expand towards 24% consistent with more mature industry peers over the longer-term once new manufacturing facilities start to come online and production continues to ramp up with scale. Operating expenses which include research and development, and selling, general and administrative spending are also expected to remain elevated until at least 2025 to support ongoing improvements to battery and powertrain technology development, introduction of new vehicle models, and expansion of its overseas sales and manufacturing capacities.

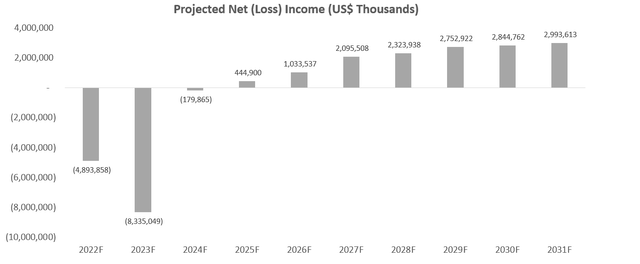

Combined with other nominal non-operating income and expenses, Lucid is expected to incur narrowing losses from $4.893 billion in the current year towards $179.9 million by 2024. The EV maker is expected to remain on track for profit realization beginning 2025, albeit at a lower figure due to near-term top-line growth and cost pressures driven by supply chain constraints. Net income is expected to expand from $444.9 million in 2025 towards $2.994 billion by 2031.

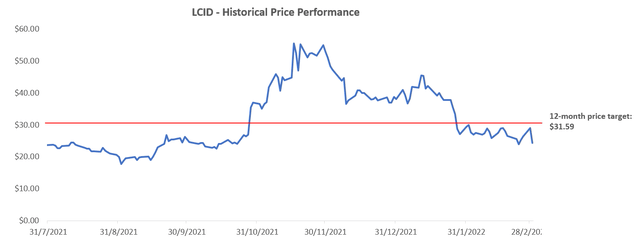

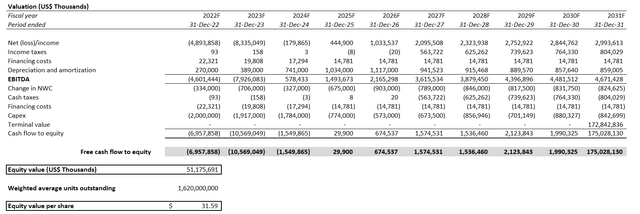

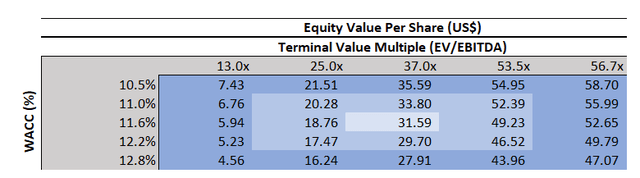

Drawing on the above analysis, our 12-month price target for Lucid remains at about $30. This represents upside potential of close to 25% based on Lucid's last traded share price of $25.52 at the time of writing (March 1st).

Key valuation assumptions applied in our valuation analysis remains largely consistent with our previous coverage as Lucid's operating environment and growth strategy has not materially changed. Despite a downward adjustment to near-term revenue cash flows due to temporary supply chain constraints, Lucid's terminal growth outlook remains intact based on the foregoing analysis. Specifically, the ongoing build-out of Lucid's global footprint, paired with the continued expansion of its product and technology roadmap is poised to advance its market share within the fast-growing luxury EV market in coming years, which further bolsters the stock's valuation prospects ahead.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- Vandaluus·2022-03-03LCID needs to show results (real PnL) and not just hide behind the EV fad to justify its inflated stock price.11Report

- KYHBKO·2022-03-04may consider buying after it breaks even. with elevated costs, it looks likely to make losses till 2025 or later. with losses, there is more downward pressure on the prices.6Report

- LohYK·2022-03-04the current market value real numbers rather than projected. expect lucid to get more hits8Report

- Jason_LSE·2022-03-04Will be great if industry experts can share a comparison table ( pro & con) of the key EV OEMs.5Report

- Shawn287·2022-03-03Is EV likely to dominate the motor vehicles industry in 2-3 years? Or are we into over-valuation of prices for now…4Report

- Nase·2022-03-04Depends on how long we can hold3Report

- kimC·2022-03-03Lucid needs to put up a great performance to justify it's market cap4Report

- JC888·2022-03-12It took Tesla 13 years to be profitable. How lo g do you think it will take Lucid to hit the millionth car? By then would it be in the green already?2Report

- JeremyKok·2022-03-05is it making a profit already in this highly competitive industry? do your own due diligence before you invest.2Report

- All in Tesla·2022-03-04Overvalued for sure no ability to scale production to reduce cost 🤔3Report

- Kraken 1·2022-03-02stats say one thing but market sentiment say another.2Report

- luckyone·2022-03-04A good EV company to look into?2Report

- Huatge68·2022-03-03So hot this car 🥰2Report

- Sigit waloyo·2022-03-08good morning1Report

- Coyotero·2022-03-07No cars so no opportunitty1Report

- MaShao·2022-03-05thanks for sharing this good article...1Report

- sk5735·2022-03-04Only time will tell1Report

- Asphen·2022-03-04LCID going 17.10?1Report

- InvisibleP·2022-03-04Still have potential?1Report

- SatieTIG·2022-03-04Can we bet Lucid over Nio?1Report