Why We Still Should Count on $Disney$

For the whole entertainment industry, disney is the best.

A mixed Q2 earnings, should be another chance for all of us.

$Walt Disney(DIS)$ released the second quarter earnings of 2022 ended April 2. The Top1 entertainment company in North America, has become the indicator of industry. What does its mixed performance tell?

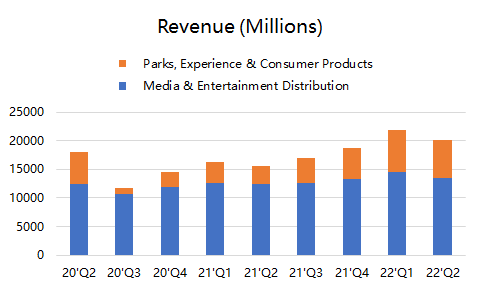

- Revenue increased by 23.3% year-on-year to US $19.25 billion, which was less than the US $20.11 billion expected by the market;

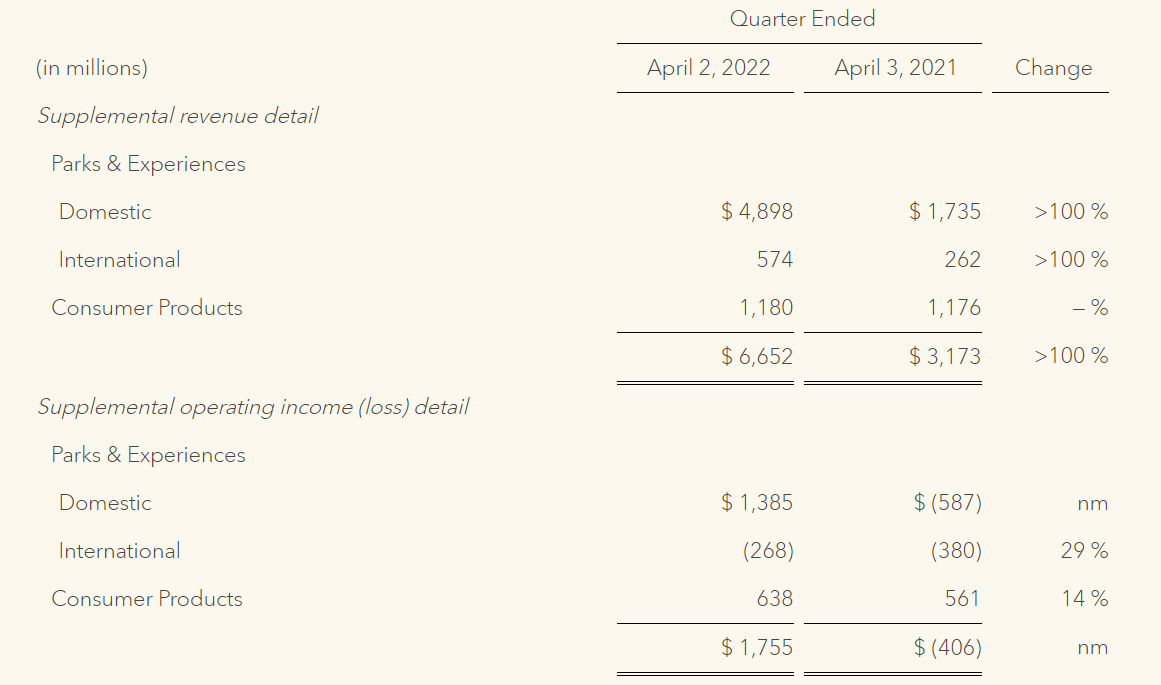

- Revenue of the media and entertainment was US $13.89 billion, while revenue of theme parks and experience was 6.65 billion US dollars, compared with the same period of last year.Higher than expected $6.12 billion;

- Operating profit of the media and entertainment was 1.94 billion US dollars, down 32% year-on-year, due to the loss of DTC business (streaming media); operating profit of theme parks and experience was 1.75 billion US dollars, better than the market consensus of 1.61 billion US dollars. In the same period last year, it lost 410 million US dollars;

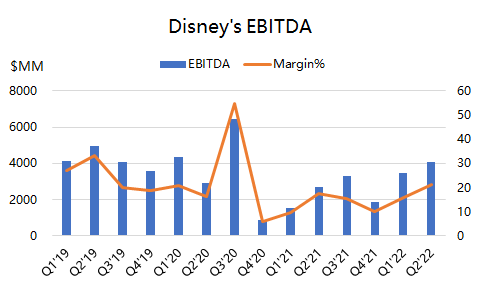

- After non-GAAP adjustment and dilution, the earnings of US stocks were US $1.08, up 37% from US $0.79/share in the same period last year, slightly worse than the expected US $1.17.

On the whole, although some financial indicators are not as good as market expectations, there are also surprises. Disney has wild business, it is difficult for analysts to accurately predict it, so the market consensus doesn't mean much.

Investors pay more attention to Disney for nothing more than two points: One Streaming Media, as Disney+ etc., the other is recovery of offline entertainment.

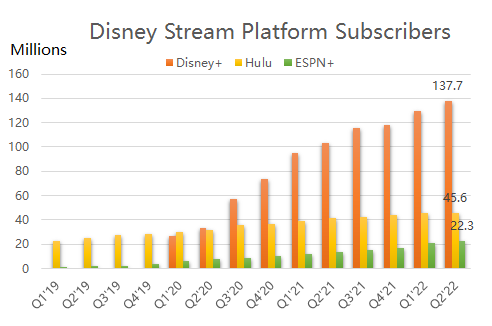

Looking at streaming media first, the total number of Disney + subscribers increased to 137.7 million this quarter, an increase of 33% year-on-year, which was higher than the market expected consensus of 134.4 million. The increase in a single quarter was 7.9 million, which was much higher than the expected consensus of 4.47 million.

It might not be the best in last few years, but much excellent than $Netflix(NFLX)$ in the same period.

Disney's latest mini TV series "Moon Knight" (finished) of lanched on March 30th, winning huge reputation, has greatly promoted the fiscal quarter ending on April 2nd.

Marvel Studio can always be count on.

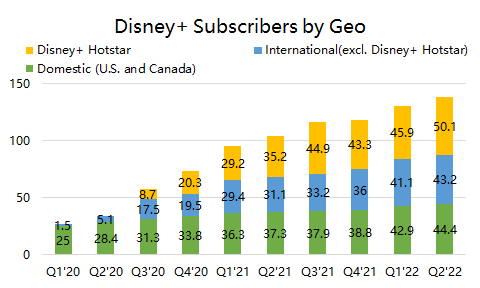

The growth rate of Disney+ in North America this quarter was 19%, which was obviously lower than the overall level, while the growth overseas was even worse, targeting Southeast Asia and other places Disney+ Hotstar subscribers increased from 35.2 million to 50.1 million, a 42% increase YOY, while the rest of the world grew by 39%.

In addition, the company expects Disney+ in the second half of the year,

The net growth will be stronger than the first half, but the growth rate "may not be as large as previously expected."

This also brings hope in the current situation of the whole streaming media decline.

Obviously, Disney+ has started its rapid overseas growth ahead of schedule, which is a mixed signal. Netflix expanded North America first, then overseas. With the same pace, Disney choose a safer way.

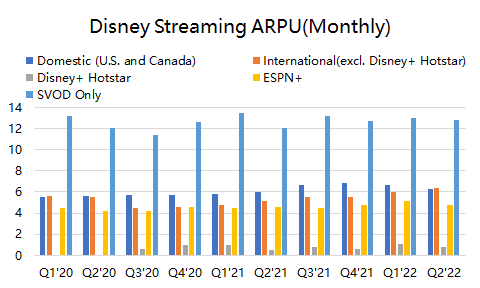

At the same time, we should also see that the losses of DTC business (Disney +, ESPN +, Hulu) are larger than expected, indicating that the market launch and cost expenditure are not restrained. Disney+ Hotstar brings major growth, but it can't bring more revenue. Compared with ARPU of $6.32 in North America, Disney+ Hotstar is only $0.76. And even if the $6.32 in North America, with a year-on-year increase of only 5%,Nor is it comparable to the inflation of more than 8% in the United States.

Therefore, Disney will inevitably encounter the bottleneck of users' purchase intention in Netflix Hospital,I t can only be seen whether there is a continuous "excellent" sequel.

Another unexpected business is offline entertainment, which is unexpected but reasonable. Theme parks took the lead in turning losses into profits in North America, and their strength exceeded market expectations, which was also the recovery of offline entertainment after the pandemic.

While overseas theme parks have not yet achieved profitability and their growth is not as strong as that of North America, they are obviously influenced by parks in Hong Kong and Shanghai. We believe when Hong Kong and Shanghai back normal operations, they will probably back to crowded.

Therefore, the offline entertainment business will have better opportunities in the following summer and autumn.

On the whole, Disney's business is not as desperate as Netflix's. On the contrary, its business is more resilient, and it is possible to get better opportunities in the next quarter or two. Investors' pessimism before is more questioning the streaming media industry. This long-term problem may need more easy methods, which cannot be solved overnight. However, in terms of stock price, it is unlikely to encounter Netflix's predicament.

Entertainment, needs Disney.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

All time favorite entertainment