Investment Highlights on SIVB crisis

Event

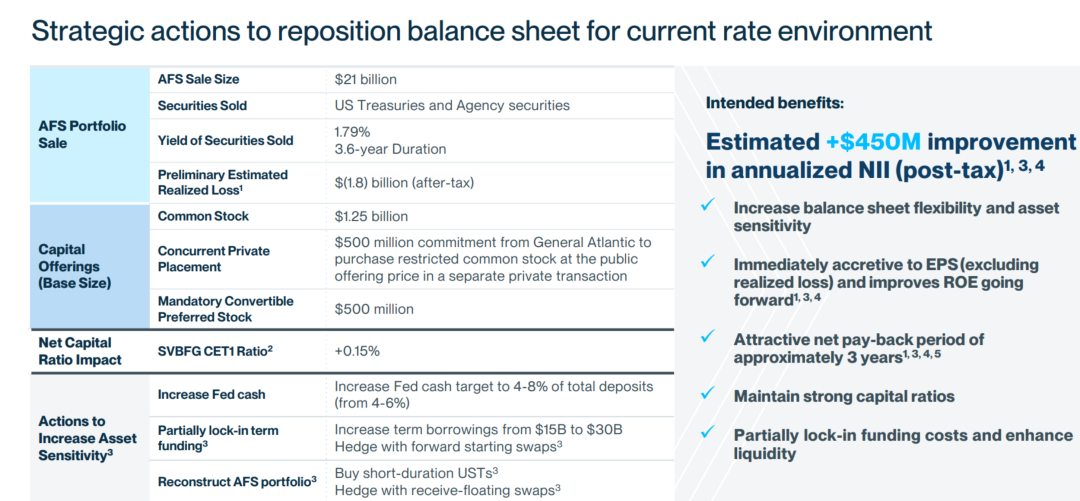

On March 9th, EST, Silicon Valley Bank $SVB Financial Group(SIVB)$ announced that it had sold all available-for-sale (AFS) assets for US $21 billion, with a loss of US $1.8 billion, and prepared to raise US $2.25 billion by offfering common shares and convertible preferred stocks.

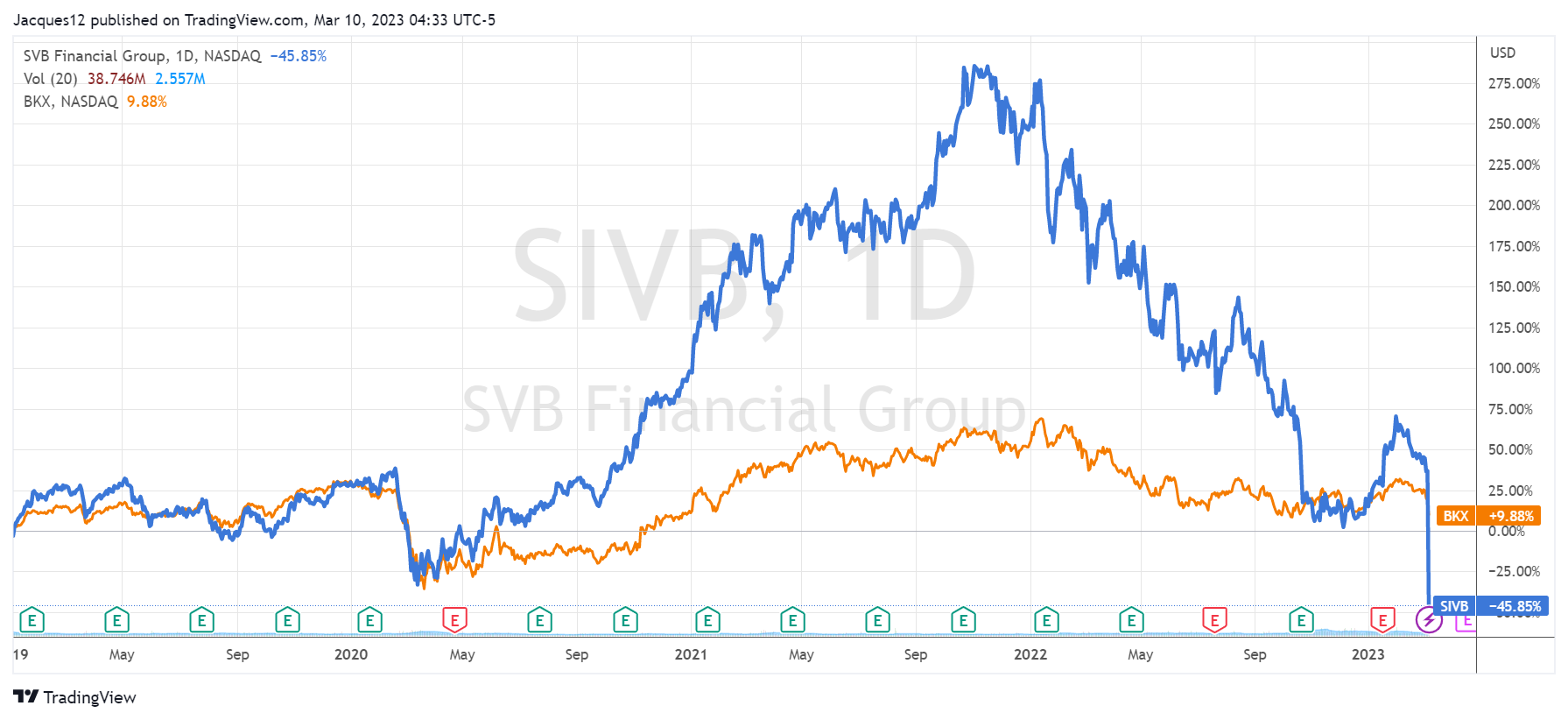

After the news,$SVB Financial Group(SIVB)$ plunged 60% in the trading day, the biggest since 1998, and continued down 22% in after hours. At the same time, the whole banking sector plummet, with the $KBW Regional Banking Index(KRX)$ plunging 7.7%.

Reasons

The collapse of Silicon Valley banks is the spread of panic among investors who are worried that bank deposits will be run-off, which will not cover the current capital demand. According to the provision ratio announced in the latest quarterly financial report of the company, as well as the adequacy of reserves, there is no bankruptcy crisis. It is essentially a liquidity problem.

The causes of this problem include:

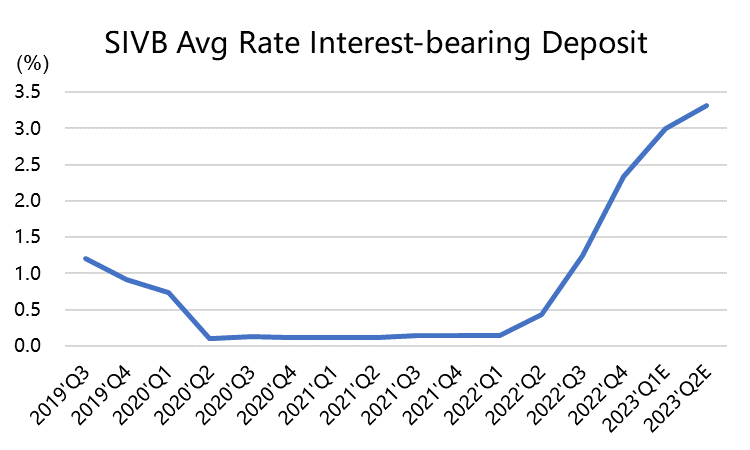

First, the Federal Reserve raises interest rates. After the pandemic, the Federal Reserve maintained zero interest rate and expanded its balance sheet for a long time. It was not until the end of 2021 that inflation heated up sharply that the process of raising interest rates and tightening began. Moreover, the pace of tightening is quite fast, raising the interest rate to 4.5-4.75% within one year. The large amount of interest-free or low-sucking deposits that banks absorbed during the previous quantitative easing period decreased, and instead became loans demanding higher return rates (the average interest-bearing loan interest rate of SIVB rose rapidly). The cost of banks' liabilities also increases with the Fed's interest rate hike, so that they have to sell available-for-sale assets with mismatched duration to replenish capital.

Second, the technology investment market cools down.Silicon Valley banks have a large number of primary market investors and start-up companies. In the past two years, the weakening of primary market investment activities has reduced bank inflows and increased the credit risk of corresponding loans (SIVB's non-performing loan ratio has also increased). In the interest rate hike cycle, technology companies are especially sensitive to interest rates. Even if companies cooperate with Silicon Valley banks for a long time, they have to save their funds to safer banks for risk control and investors' requirements.

Third, liquidity issues.Term mismatch between asset and liability is a common problem, especially in the cycle when interest rates change very fast. SIVB announced the sale of longer-term US bonds and MBS in its financial portfolio (CEO said that almost all AFS assets that can be sold have been sold). Although it suffered a loss ($1.8 billion), it ensured liquidity. At the same time, it also repositioned the balance sheet to improve the strategy of asset sensitivity, increase net interest income and push up the capital ratio.

Investment Highlights

Why Silicon Valley Bank?

First of all, it is the company with the closest connection with high-risk business in the whole industry. It is closely related to technology, medical startups and related venture capital firms, so it achieved a return rate much higher than the banking average during the boom period of the technology industry (+55.6% vs KBW-13.6% (2020); +75.6% vs KBW +35.1% (2021)), but it was also higher than the industry average when there was a retracement in 2022 (-66.6% vs KBW-27.7% (2022)). Because they are regional small and medium-sized banks, the volatility becomes greater.

At the same time, the activities related to the listing of startups (including IPO, DPO and SPAC) decreased, which further reduced its non-interest income. The proportion of its net interest income in the overall income increased from 47.2% in Q1 2021 to 68.5% in Q4 2022. Therefore, the importance of interest rate-related lending business in the company's operation has been further enhanced, and the company's growth has declined rapidly since 2022, and its performance has deteriorated.

Coincidentally, the one who declared bankruptcy the day before$Silvergate Capital(SI)$The news (code SI, two characters less than SIVB) is scrolling, and investors who don't know the truth may panic about "banking crisis" and cause a run on the bank. In addition, investors such as Peter till, Coatue, USV, Founder Collective and other institutions all suggested taking money out of SIVB from investors, resulting in "the more panic, the more run, the more panic".

Whether it's a malicious shorting or the liquidity problems that should have been exposed are just coming to the surface, it's enough for Fed officials to pay attention to the possible problems in the banking industry in the environment of raising interest rates.

Do other regional banks have similar problems?

After plunging 60%, the market value of Silicon Valley banks fell from the head of the entire regional banking sector to the middle waist, but its Tier 1 asset ratio was 15.44%, higher than the average of 12.14%; The ratio of Tier 1 assets of common stock is 12.09%, which is higher than the average of 11.29%, the ratio of tangible equity (TCE Ratio) is 5.61%, which is lower than the average of 7.25%, and the ratio of loans to deposits is 42.89%, which is lower than the average of 80.31%. Regional banks that have performed well across the industry show that their assets are not as good as SIVB's are everywhere.

Of course, other regional banks' main customers are not as concentrated in the technology industry as SIVB's. At the same time, except for assets,More importantly, it depends on the liquidity reserves of small and medium-sized banks.That is to say, we should pay attention to the liquidity of their assets. Even financial products that can be sold in the short term, such as AFS, have prices lower than the theoretical value due to a large number of sales. Liquidity discount can easily make more banks "floating losses" become "real losses".

At the same time, some wealth management companies with cash management business may also have such problems, such as$Charles Schwab(SCHW)$On the one hand, it is necessary to pay the "deposits" of investors who are rising, and on the other hand, it is necessary to find ways to allocate the money "at the same time" to products with higher returns. Wealth managers that buy financial products with higher interest rates will further consider the risk of default when banks have a liquidity crisis, so the risk premium of these products will be raised.

Who would be the beneficiaries in this crisis?

Generally speaking, raising interest rates will increase the net interest spread of banks, thus increasing the net interest income of traditional banks. However, raising interest rates too fast will expose the problem of term mismatch and highlight the liquidity crisis. At the same time, high interest rates are not conducive to corporate lending and change the balance sheets of banks.

It is a crisis for banks with insufficient liquidity. On the other hand, is it possible for banks with sufficient liquidity to profit from it?

Like Silicon Valley banks, they are forced to sell AFS financial products that have not yet expired at a discount, so some counterparties must have found this bargain. If its liquidity is good enough, there will be extra income when it is held to maturity. Big banks and asset managers with sufficient liquidity may play such a role.

At the same time, those investors who withdraw their funds because of the liquidity and debt ratio of small and medium-sized banks will definitely choose safer banks to deposit. By comparison, large banks with sufficient capital will have advantages.

Then it evolved into the game of big fish eat small fish.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- SureWinkiat·2023-03-10bye bye. money gone. recession liao4Report

- KickAss1337·2023-03-10Crash and burn is good!2Report

- hd87·2023-03-11Thanks for sharingLikeReport

- xiaobaii·2023-03-11like & comment please1Report

- reeve·2023-03-11NiceLikeReport

- Cheahkim·2023-03-11谢谢LikeReport

- WmochaW·2023-03-11Thanks1Report

- stkwok·2023-03-11Like1Report

- Hosay_hosay·2023-03-11[Cool][Cool]1Report

- Jialatsia·2023-03-11MeepLikeReport

- boonk·2023-03-11okkkkLikeReport

- DesmondLee·2023-03-11G1Report

- Yang Sheng·2023-03-11ok1Report

- maxcheng·2023-03-11👍1Report

- EdmondT·2023-03-11ok1Report

- EdmondT·2023-03-11okLikeReport

- SkyLim·2023-03-11ok1Report

- Paggie·2023-03-11阅LikeReport

- Derrick_1234·2023-03-11OkLikeReport

- KSR·2023-03-11👍LikeReport