Economic and Market Review February

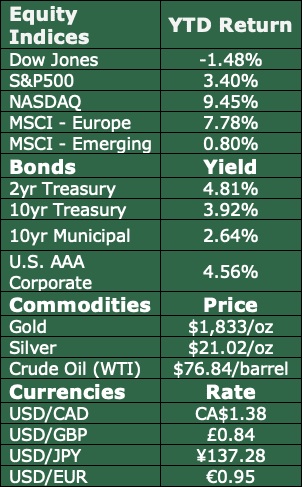

Monthly Summary

Monthly Summary

Inflation worries persisted in February as government data revealed stubbornly elevated prices for food and energy. As a result, the Federal Reserve’s policy on additional rate increases continues to bombard the equity and bond markets. The Fed’s concern is that it might relent too soon in combating inflation, so it is expected to continue on its rate increase trajectory until economic data proves otherwise.

Recent economic terms highlighted in the media include soft landing and hard landing. A soft landing indicates a non-recessionary outcome after the Fed stops raising rates, while a hard landing denotes a recessionary environment. Many economists believe that it is too soon to determine which may occur yet believe that an extended period of rate hikes likens the possibility of an eventual hard landing.

Stronger-than-expected employment data along with surprisingly resilient consumer demand drove the Federal Reserve to raise short-term rates, resulting in rates rising this past month. Mortgage and consumer loan rates rose in February, adversely affecting housing and consumer durables, where interest rates pose a significant factor.

Many analysts believe that the Fed’s current policy of ongoing rate increases might be hinged on stale economic data, including employment and consumer data. Economists view some of these data as lagging indicators, meaning that current economic conditions are not being properly represented.

Recently released data from the Bureau of Labor Statistics reveals that consumers are pulling back on cyclical goods such as clothes and electronics while focusing on food and essential products like toilet paper and toothpaste. Larger ticket items, which are more expensive products such as appliances and autos, are seeing a drop in sales as consumers redirect funds.

Internationally, the European Union continues to see inflation at 10% alongside a 6.1% unemployment rate, translating into economic stagnation per the most recent data releases. As in the U.S., stubbornly high food and energy prices continue to divert consumers from buying what they want versus buying what they need. The Russian invasion of Ukraine continues to pose a challenge to global supply chains and inflationary pressures. Reduced trade with Russia has led numerous countries to replace inexpensive Russian imports with other pricier sources.

A renewed concentration on consumer incomes and inflation is materializing, as average income growth continues to fall behind inflation, meaning that consumers are struggling to maintain regular spending habits without an immediate pay raise. A Federal Reserve Bank of New York survey showed that households expect income growth to drop, creating additional uncertainty for consumers as well as creating a detrimental impact on consumer confidence.

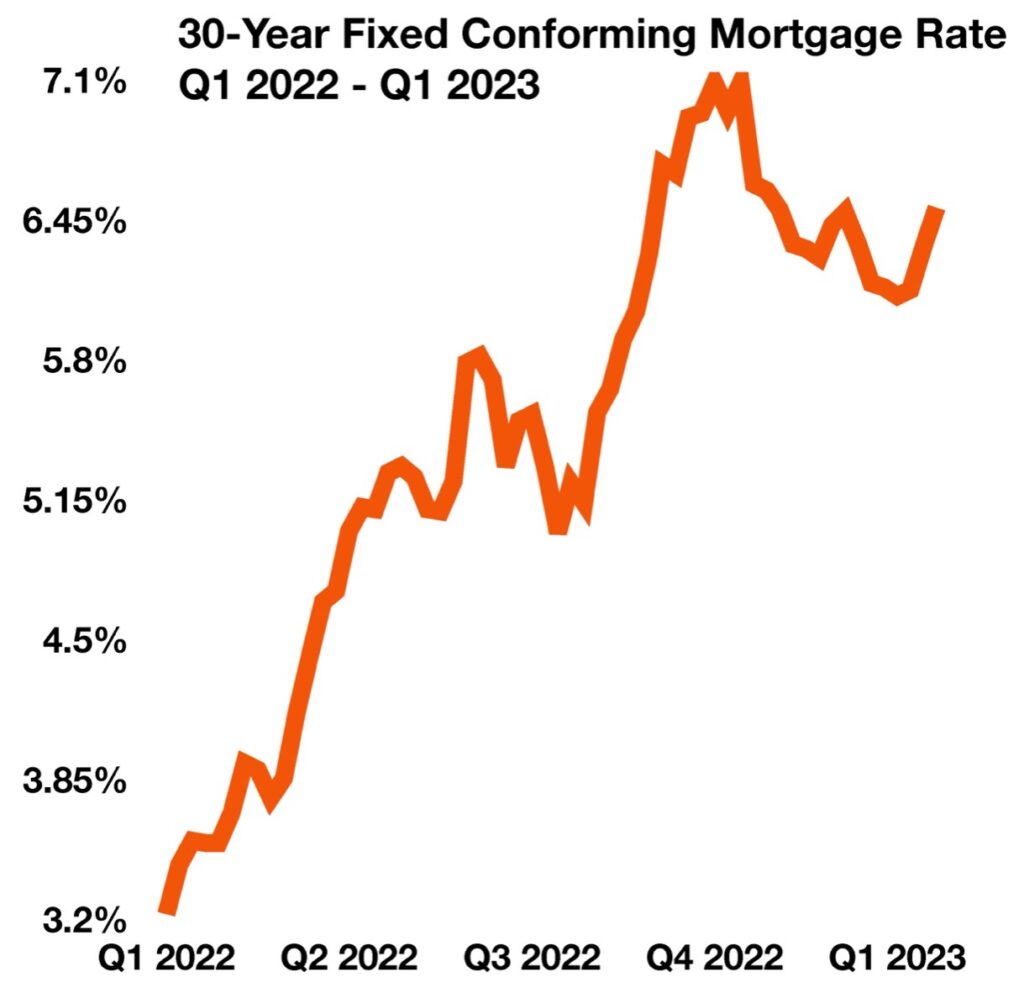

Higher Mortgage Rates Deter Buyers

With interest rates breaching higher levels, mortgages are becoming less affordable for millions of Americans. As a result, demand for new mortgages continues to reach decades-long lows, influencing homebuyers to either wait for rates to fall or for home prices to drop significantly.

Economists believe that a unique dynamic has evolved from the current housing environment. Existing homeowners with low mortgage rates are hesitant to sell and move into a higher-rate mortgage, enticing homeowners to stay put. This in effect minimizes the inventory of homes available for sale and possibly acts as a price buffer for available homes.

The 30-year fixed mortgage rate reached 6.65% in early March, its highest point since November of last year. This comes amidst continuously higher mortgage loan rates that reached as high as 7.08% in October and November of 2022, a 20-year high that the housing market last saw in 2002.

Loan and Credit Delinquency on the Rise

Loan and Credit Delinquency on the Rise

Following the 2008 financial crisis, consumers began defaulting on loans across the board. Since then, loan delinquencies have fallen steadily, with some dropping lower than half of their crisis peaks. However, recent data show that this trend has been reversing, with loan delinquencies on the rise throughout 2022. Economists closely follow delinquency rates as an indicator of possible faltering consumer finances.

The two most significant increases in delinquencies have been with credit cards and auto loans. Auto loans headed into the end of 2021 with 9 consecutive quarterly decreases, reaching as low as just 4.9%. However, they have since increased steadily up to 6.64% as of the fourth quarter of 2022. The current delinquency rate is nearly at a 3-year high. Credit card loans have also reached a 2.5-year high following 2 years of decreases in loan delinquencies, with current credit card delinquency rates at 5.87% of outstanding balances.

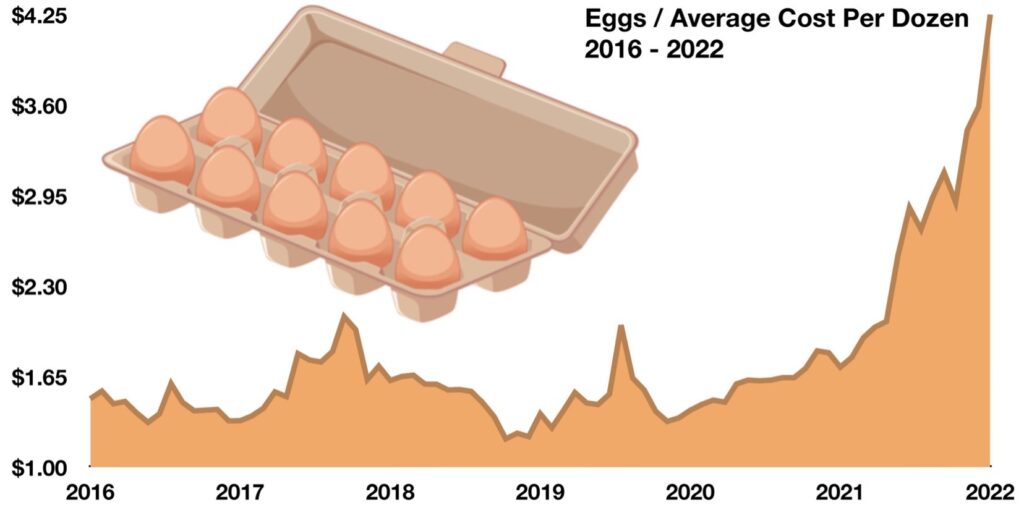

Eggs Continue To Get More Expensive

Amidst high food inflation throughout 2022, eggs have emerged as particularly costly goods at the grocery store in recent months. Egg consumption has been rising in recent years as compared to other protein sources, yet production has recently fallen due to an ongoing bird flu epidemic.

This bird, or “avian” flu, has infected 58 million birds, making it the largest outbreak of the flu in U.S. history. These birds must immediately be slaughtered once infected, which has caused the price of eggs to spike 60% in the past year alone. As of December 2022, the average price for a dozen of eggs was $4.25, up from just $1.32 in late 2020. Higher prices might remain for an extended period until the number of hens returns to its pre-flu norms.

Rising Car Payments Become Less Affordable for Many

Rising Car Payments Become Less Affordable for Many

Since the pandemic ushered in a widespread global shortage of semiconductor chips that are vital to new vehicles, car prices have risen to historic highs. Three years later, the supply issue has dissipated somewhat, yet prices for new vehicles remain abnormally high.

The average monthly loan payments on new cars rose past $700 in 2022, while used vehicles surpassed $500 on average. Despite years of fairly constant prices, the costs of new vehicles have skyrocketed following chip shortages and a reinvigorated demand for cars following the pandemic. While new car prices never surpassed yearly price growth of over 2% for 9 years, they increased over 10% during 10 consecutive months in 2022.

Used vehicles saw much more dramatic price changes, with prices increasing as high as 45% in late 2021 and throughout 2022. Used car prices have historically fluctuated more than new car prices, yet 2022 saw historic price jumps. In trend with used vehicles’ volatility, their prices have been falling rapidly in recent months, dropping nearly 12% in January of 2023 alone. So, while used car prices are still higher than pre-pandemic levels, their prices have finally begun trending toward normalcy. Albeit, the same cannot be said for new car prices, which have steadily increased for 30 consecutive months.

$S&P 500(.SPX)$ $NASDAQ(.IXIC)$ $DJIA(.DJI)$ $E-Micro Gold - main 2304(MGCmain)$ $Micro WTI Crude Oil - main 2304(MCLmain)$

https://buildingbenjamins.com/market-and-economy/economic-and-market-review-february/

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- ramondk·2023-03-09Good information1Report

- xiaobaii·2023-03-10like & comment please1Report

- Sirlatesalot·2023-03-09Thanks for sharingLikeReport

- SmallYang·2023-03-09Thanks for sharingLikeReport

- Alvis89·2023-03-10Go odLikeReport

- Chichiw76·2023-03-09okieLikeReport

- STLoke·2023-03-09hmmm....LikeReport

- Potatoclown·2023-03-09Yep thanksLikeReport

- Oldhead·2023-03-09ThanksLikeReport

- j up p·2023-03-09okLikeReport

- MalayaKG·2023-03-09lolLikeReport

- Yolofomo101·2023-03-09GdLikeReport

- HandsomeBoy·2023-03-09[Miser]LikeReport

- Jjsh·2023-03-09OkLikeReport

- K20·2023-03-09okkLikeReport

- Ruixiang·2023-03-09HLikeReport

- CExecutive·2023-03-09OoLikeReport

- Ccchia·2023-03-09kLikeReport

- jjsh2·2023-03-09OhLikeReport

- aozora·2023-03-09OkLikeReport