Weekly: After a Best Week Since June, Usher a Super Earnings Week

The major U.S. stock indexes started the week and ended it with sizable daily rallies, rebounding from the previous week’s mostly negative results. The $S&P 500(.SPX)$, the $NASDAQ(.IXIC)$, and the $DJIA(DJIA)$ all finished with weekly gains of around 5% as investors focused on quarterly earnings and prospects for further interest-rate increases.

As of last Friday, the$Straits Times Index(STI.SI)$ lost 2.29% weekly with a -4.92% YTD; and $S&P/ASX 200(XJO.AU)$‘s YTD performance is -10.3%, with a lost of 1.21% last week.

The dollar index was broadly flat, while the pound rallied on the prospect of Rishi Sunak becoming Britain's next prime minister after Boris Johnson dropped out of the race. Investors were cheered by reports that the Federal Reserve's aggressive rate hike policy stance could soften slightly later this year.

According to FactSet: Nearly a third of S&P 500 companies, or 161 companies, will report earnings in the coming week, . Earnings data from these companies can give investors a better idea of how companies are doing as inflation weakens consumer spending, ongoing supply chain challenges and a stronger dollar.

Notable Earnings Calendar:

$Coca-Cola(KO)$ ,$General Motors(GM)$ ,$UBS Group AG(UBS)$ ,$3M(MMM)$ ,$Microsoft(MSFT)$ ,$Alphabet(GOOG)$ ,$Visa(V)$ ,$Spotify Technology S.A.(SPOT)$ ,$Texas Instruments(TXN)$ ,$Boeing(BA)$ ,$Meta Platforms, Inc.(META)$ ,$Ford(F)$ ,$Teladoc Health Inc.(TDOC)$ ,$McDonald's(MCD)$ ,$MasterCard(MA)$ ,$Apple(AAPL)$ ,$Amazon.com(AMZN)$ ,$Intel(INTC)$ ,$T-Mobile US(TMUS)$ ,$CVS Health(CVS)$ ,$Exxon Mobil(XOM)$ ,$AbbVie(ABBV)$ ,$BYD Co., Ltd.(BYDDY)$

Macro Factors to Watch

Earnings Outlook: The subdued expectations for earnings season improved slightly as a second week’s batch of quarterly results came in. As of Friday, Q3net income was expected to rise 1.5% compared with the same period a year earlier, based on S&P 500 companies that have already reported combined with projections for those still scheduled to report. In the previous week, analysts had forecast growth of 1.3%.

Labor Market Resilience: Despite concerns about rising interest rates and recessionary trends, a key labor market indicator continues to show signs of strength. The government reported that American workers submitted 214,000 initial claims for unemployment benefits during the latest weekly period. That figure is down from 226,000 the week before and is close to the historically low level that they’ve averaged year to date.

Housing Slowdown: U.S. home sales in September fell for the eighth month in a row. Rising mortgage rates are one reason for the slowdown; the firm Freddie Mac reported on Thursday that the average 30-year fixed-rate mortgage rose to a rate of 6.94%, up from 6.92% the previous week and more than double the 3.09% figure from a year earlier.

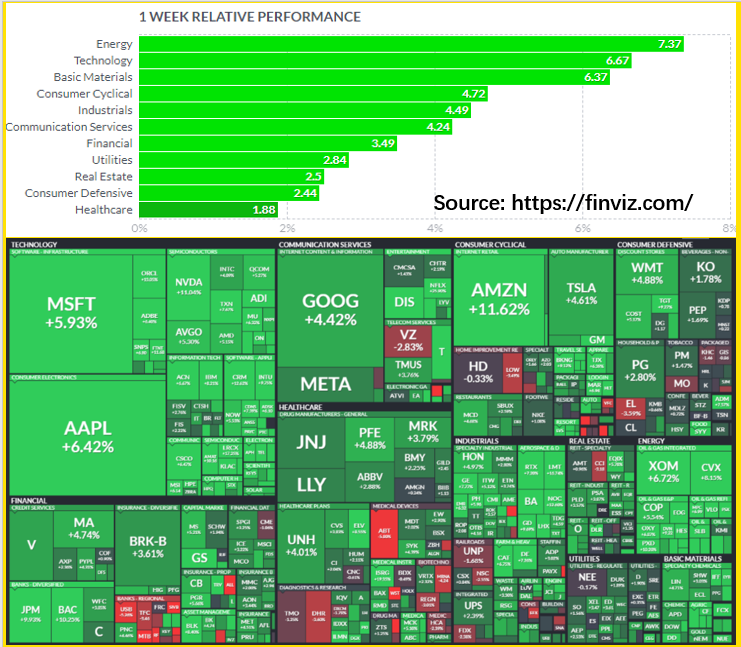

Sectors & Stocks Performances Review

Weekly Top Gainers of S&P 500

Data from Tiger Trade

Top 10 lists: $NFLX(NFLX)$ ,$Schlumberger(SLB)$ ,$Intuitive Surgical(ISRG)$ ,$Lam Research(LRCX)$ ,$Lockheed Martin(LMT)$ ,$Baker Hughes(BKR)$ ,$Freeport-McMoRan(FCX)$ ,$Halliburton(HAL)$ ,$Carnival(CCL)$ ,$Norwegian Cruise Line(NCLH)$

Other Markets:

Yield Fluctuations:The yield of the U.S. 10-year Treasury bond eclipsed 4.20% on Friday, a week after breaching the 4.00% level for the first time since October 2008. The yield of the 2-year Treasury was volatile, rising above 4.60% briefly on Thursday before slipping back to 4.51% on Friday—the highest since August 2007.

U.K. Leadership Transition:The financial market turmoil that followed Prime Minister Liz Truss’ release of a tax-cut plan triggered political fallout for the United Kingdom’s leader, who stepped down from her post after 45 days on the job. Before resigning on Thursday, Truss abandoned her proposals for large tax cuts paired with spending increases.

U.S. WTI crude oil futures rose 0.5% last week. Natural gas futures prices fell sharply last week, falling more than 20% for the week, hitting the lowest closing price since March 2022; gold futures rose about 0.5% last week.

The Week Ahead: October 24-28

Recession Watch: The scheduled release on Thursday of the government’s initial estimate of third-quarter GDP will show whether positive growth returned after two consecutive quarters of economic contraction—a result that met the technical definition of a recession. In the second quarter, GDP declined at an annual rate of 0.6%; in the first quarter, the decline was 1.6%.

Price check ahead: A report scheduled to be released on Friday will be closely watched for any signs that U.S. inflation might edge downward anytime soon. The government will update its Personal Consumption Expenditures Price Index, the Fed’s preferred gauge for tracking inflation. The most recent monthly report showed that PCE inflation excluding food and energy prices rose 4.9% in August from a year earlier, up from 4.7% the previous month.

Monday

- No major reports schedule

Tuesday

- S&P/Case-Shiller 20-City Composite Home Price Index

- Consumer Confidence Index, The Conference Board

Wednesday

- New home sales, U.S. Census Bureau

Thursday

- Third-quarter GDP, advance estimate, U.S. Bureau of Economic Analysis

- Durable goods orders, U.S. Census Bureau

- Weekly unemployment claims, U.S. Department of Labor

Friday

- Personal Consumption Expenditures Price Index, U.S. Bureau of Economic Analysis

- University of Michigan Index of Consumer Sentiment

- Pending home sales, National Association of Realtors

Do you believe Octorberwill be a better month for US stocks?

Welcome to Join daily Discussion about your Trade?

Share Trades to Win Coins! (OCT 24)

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

👍

Smarter!

@TigerObserver