Why Pinduoduo Win that much in Q2? Compare with BABA & JD

$Pinduoduo Inc.(PDD)$ released Q2 earnings before market open on August 29th. Unlike many investors' first impressions of a disaster Q2, Pinduoduo not only beats in revenue, but also recorded the highest profit in history, especially when e-commerce giants $Alibaba(BABA)$ and$JD.com(JD)$ were suffering. The market also unceremoniously gave an intraday increase of up to 20%, closing with a 14.7% surge. Since Pinduoduo in $NASDAQ 100(NDX)$ it help the index less affected by the sold off in the trading day.

Why can Q2 be the best single season?

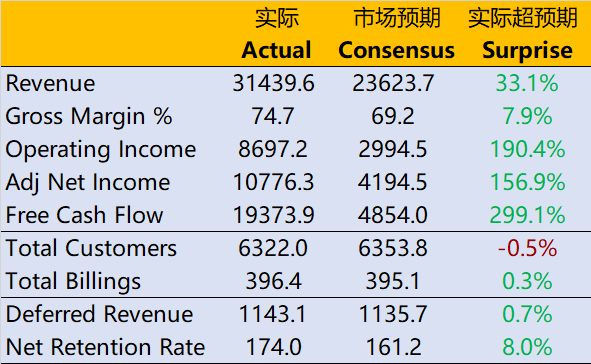

- The overall revenue was 31.44 billion yuan, a year-on-year increase of 36%, much higher than market consensus of 23.62 billion yuan;

- Online marketing service income was 25.17 billion yuan, a year-on-year growth rate of 39%, higher than the market expectation of 18.59 billion yuan, and transaction service income was 6.22 billion yuan, a year-on-year growth rate of 107%, higher than the market expectation of 5.23 billion yuan;

- Gross profit margin reached 75%, higher than the market expectation of 69%;

- The marketing expenses were 11.34 billion yuan, a year-on-year growth rate of 9.2%, higher than the expected 10.26 billion yuan; R&D expenses were 2.61 billion yuan, up 12% year-on-year, and 2.96 billion yuan was expected by the market.

- Operating profit is 8.7 billion yuan, much higher than the market expectation of 3 billion yuan.

It can be said that Pinduoduo's financial report has far exceeded market expectations since the first column above the income statement.

In terms of Revenue,

It is much higher than the market consensus, which means the market is not expected it enlarge its market share. On one hand, some areas of Q2 were affected by the pandemic, analysts' expectations are lower; On the other hand, the market believes that the pattern of e-commerce enterprises will not change greatly. Considering the growth rates of Ali (core e-commerce+1%) and JD.com (self-operated e-commerce +5%), Pinduoduo will not be predicted at a growth rate of 36%.What Pinduoduo did better was to make a major breakthrough during the 618 periodIn this festival that does not belong to it, "a presumptuous guest usurps the host's role.

In terms of Macro

It is precisely because of the epidemic situation in some areas,Consumers' consumption habits have also been changed, which gives the e-commerce industry a chance to reshuffle.Pinduoduo's "factory direct sales" mode and community group buying of "buy more food" played an important role during the epidemic. As for some investors who think that consumers prefer Pinduoduo, it is a "consumption downgrade". In fact, on the other hand, Pinduoduo itself is also "upgrading consumption", and its advantage is not "cheapness", but improving shopping efficiency.

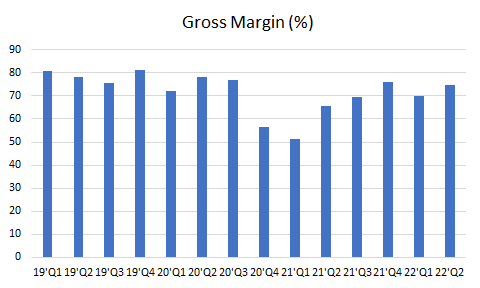

In terms of gross profit,

Pinduoduo's gross profit margin gradually recovered to the level before 2019, when there were no large-scale self-operated goods. Since the scale of self-operated goods sales is reduced, the profit rate can be aligned with the previous high level.

In terms of expenses,

R&D expenses are the only one lower than expected, which is also due to Q2 special reasons. Although management expenses and marketing expenses are higher than expected, they generally show a downward trend in growth rate, which shows that users' purchasing habits are gradually developed, and there is no need for continuous high marketing expenses to maintain them. This is helpful to maintain the long-term profit margin.

Of course, the executives specifically stated in the telephone conference,The profit margin of the current quarter may not be the normal state in the future. This may also be to actively reduce the market's profit expectations, so as not to be "killed".

After all, Pinduoduo did not release the data of active users and sellers this quarter, and this activity data has peaked in the past few quarters, which is why the company began to exert its "retention rate" and "profit rate".

We believe that with the change of consumer habits would further change the market structure, there is still much room for Pinduoduo's future growth, and cost decline will help its profit margin continue beating market expectations.

What changes will happen to the secondary market when we compare the Top 3?

Through the performance in these quarters, the performance of the three major home appliance companies after the epidemic is also slightly different. It is more intuitive to compare them together.$Alibaba(BABA)$$JD.com(JD)$$JD-SW(09618)$$Alibaba(09988)$

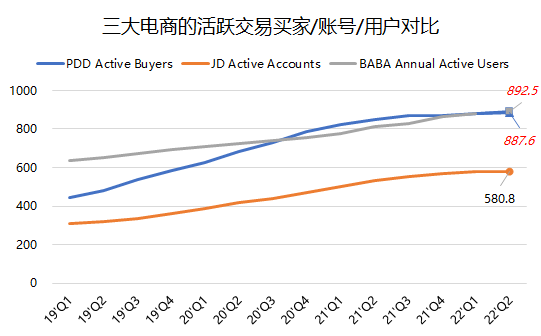

From user activity, AliBABA and Pinduoduo's (domestic) e-commerce active buyers almost hit the ceiling.

Because the statistical caliber of each family is different, for example, Ali is the annual active buyer, Pinduoduo is the number of active buyers, and JD.COM is the active account, so the comparison will definitely be different. However, we can understand the general trend through the year-on-year data, that is, the current peak is about 900 million buyer accounts. Q2 did not publish active buyer accounts except JD.COM, so it took the market expectation consensus (average) instead. JD.COM's statistical caliber is slightly different.

From revenue ,The growth rates of Ali (domestic retail) and JD.COM both declined in the first two quarters of this year, and fell to single digits in Q2. Because Pinduoduo has never participated in the shopping season, the growth rate of Q4 in 21 years is slightly slower, but it has picked up again in the first two quarters of this year.

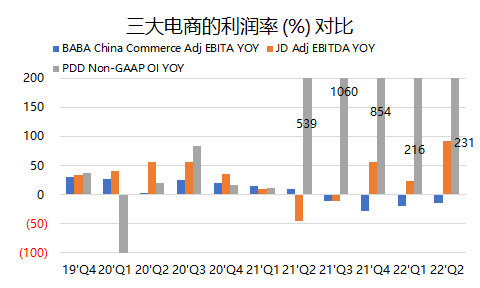

From the perspective of profit,Pinduoduo's growth is in the dust, because it is in the growth stage of realizing profits.

Pinduoduo does not have EBITDA, so we use Non-GAAP operating profit; JD.COM adopts the adjusted EBITDA (profit before interest, tax and amortization); Ali adopted the adjusted EBITA (earnings before interest, tax and amortization), and changed the business classification caliber in 21Q4, but we can also see the trend.

Obviously, Ali's Chinese e-commerce company's profit has declined year-on-year for four consecutive quarters, JD.COM has shown certain resilience in the past three quarters, while Pinduoduo's profit has increased rapidly and accumulated cash flow continuously.

Judging from the changing trend, it is obvious that Pinduoduo has the most potential for upward growth. If we look at the valuation, whether it is income multiple or profit multiple, Pinduoduo has a large upside.

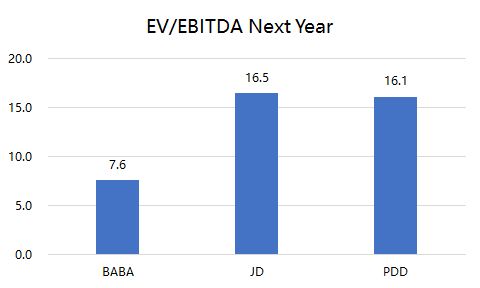

At present, the market expects Alibaba's EV/EBITDA multiple to be 7.6 times in 2023. Of course, Ali's cash reserves and profit base are also high. While JD.COM is 16.5 times and Pinduoduo is 16.1 times, which are basically the same.However, due to the high profit growth expectation of Pinduoduo, the subsequent performance may be even better.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Good