How to trade after a hawkish rate cut?

Last week, assets entered a new wave of correction after the December FOMC meeting.

First, on the rate cut front, the Fed cut 25bp as planned, bringing the benchmark rate back to 4.25%-4.5%, just as the market thought it would be, as November data on nonfarm payrolls, service prices, and rents, as well as data on GDP and the unemployment rate, all supported the cut.

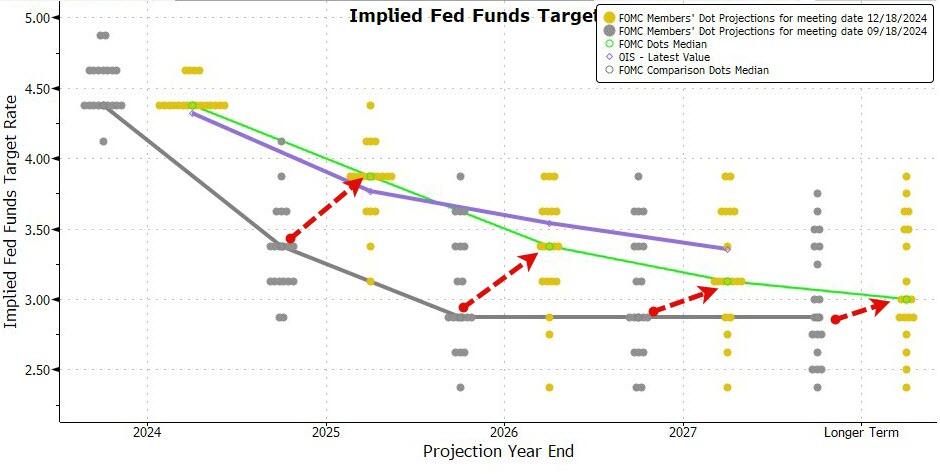

Second, at the meeting the Fed indicated that rate cuts would slow down in the future, with the "dot plot" showing only two cuts in 2025, less than the market expected.The meeting statement also added to consider the "magnitude and timing" of the words, Powell also said to be more cautious, move more slowly, but also have to keep an eye on the trend of inflation.

In addition, the Fed has adjusted its economic data forecasts for 2025, raising real GDP growth from 2.0% to 2.1%, PCE inflation from 2.4% to 2.5%, and the unemployment rate from 4.4% to 4.3%, which matches the economic outlook at the time of the soft landing, which was for employment to stabilize, and inflation to bottom out in the middle of the year before rebounding.

Neutral interest rate was also raised, before the Cleveland Fed President said interest rates close to neutral will have to slow down, this meeting of the Federal Reserve neutral interest rate from 0.9% in September to 1%, and the real interest rate difference shrunk to 1.3 percentage points.

The future policy path will have to balance a number of factors, and it remains to be seen for a while.

Now in the case of a soft landing, the Fed has to balance the fundamentals and the inflationary pressures brought about by Trump's policies.

On the one hand, interest rate constraints are not great, the gap between financing costs and investment returns is small, and there is a risk of cutting rates too fast or too slow, and after the recent cuts you may have to see what happens before setting the pace;

On the other hand, after Trump's election, the Fed has to assess the impact of his policies, although Powell did not explicitly say, but implied that we have to look at the impact of tariffs or something, and some members of the relevant assumptions have been counted into the policy considerations.

When to cut interest rates in the future, how much, depending on the natural course of the economy and the impact of Trump's policies.

Economically, the credit cycle projects inflation and core inflation could bottom out in mid-2025;

Policy-wise, inflationary policies are likely to come out of Trump's presidency faster because of process, but perhaps limited, and growth policies like tax reform are likely to advance faster.

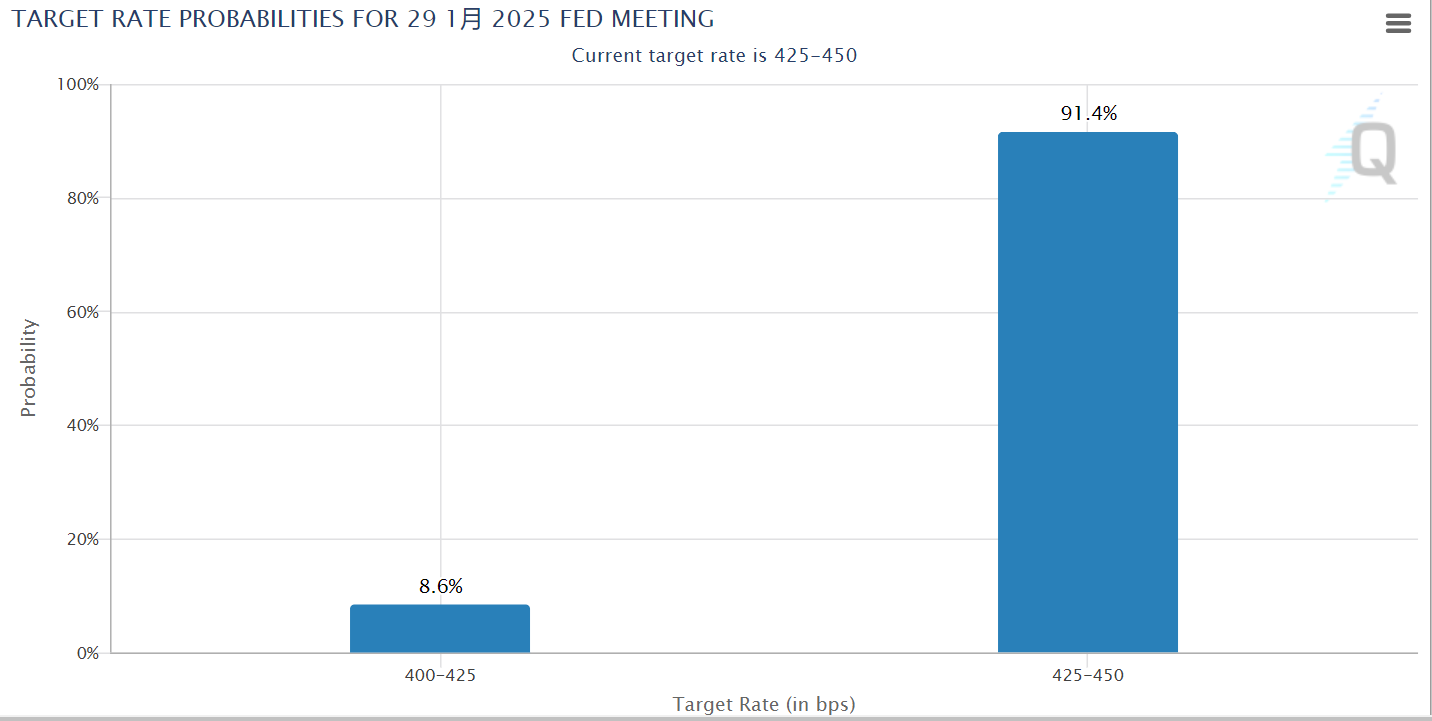

Therefore, the Fed's January meeting is critical, Trump's inauguration may be fierce signing of executive orders, so the January 29 FOMC rate cut is unlikely, if his inflation policy is moderate, the first half of the year there is still a chance to cut interest rates, otherwise it may be pushed back.But now the policy still has room for rate cuts, unless inflation rises sharply.

Back end of rate cuts, asset trading logic

The interest rate cut space is calculated with the goal of restarting the private credit cycle and bringing down the cost of financing below the ROI.By the analytical framework, it is appropriate to reduce the base case to around 3.5%, which is another 50-75bps.

In terms of returning monetary policy to neutrality, referring to the Fed's model and dot plot to calculate the natural rate, combined with the PCE level, a cut of 2-3 to 3.5%-3.8% is reasonable; from the Taylor Rule assumptions, taking into account the Fed's weighting of the inflation and employment targets, the long-run target, and the economic data estimates at the end of 2025, the appropriate federal funds rate is 3.2%, but factors such as inflation tailing may make the rate cutsmaller.

In terms of the impact on assets, before the market is expected to be too fierce, this time the interest rate cut is expected to drop, the assets will pull back, the short term can wait for new opportunities, the medium term to strengthen the pro-cyclical direction.

U.S. bonds: interest rate lows over, the bottom will rise, combined with the neutral rate calculation, the long end of the U.S. bond reasonable pivot is 3.9-4.1%, the current level of 4.7% is obviously limited high, there may be trading opportunities.The rise in the long end is mainly due to supply and growth expectations, with a large contribution from the term premium and a small impact from rate hikes and inflation expectations. $iShares 20+ Year Treasury Bond ETF(TLT)$

U.S. stocks: short-term valuations are high, expectations are high, be on the lookout for changes in sentiment when data and policy are not as expected, after the pullback mid-January policy and performance period is a key node to intervene, the index is now at a key support level. $iShares Russell 2000 ETF(IWM)$ $.SPX(.SPX)$ $.IXIC(.IXIC)$ $.DJI(.DJI)$ $SPDR S&P 500 ETF Trust(SPY)$

US Dollar: natural economic fixes and post-election policies have supported it, short-term expectations have dropped the dollar has risen instead, and while too much short-term rise may not be good, it's still strong overall unless there's policy intervention. $Invesco DB US Dollar Index Bullish Fund(UUP)$

Gold has already exceeded the support level calculated by fundamental models, even with risk premium compensation, and is able to deal with uncertainty in the long term, with a neutral recommendation in the short term. $Barrick Gold Corp(GOLD)$ $SPDR Gold Shares(GLD)$

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

In terms of the impact on assets, before the market is expected to be too fierce, this time the interest rate cut is expected to drop, the assets will pull back, the short term can wait for new opportunities, the medium term to strengthen the pro-cyclical direction.

U.S. bonds: interest rate lows over, the bottom will rise, combined with the neutral rate calculation, the long end of the U.S. bond reasonable pivot is 3.9-4.1%, the current level of 4.7% is obviously limited high, there may be trading opportunities.The rise in the long end is mainly due to supply and growth expectations, with a large contribution from the term premium and a small impact from rate hikes and inflation expectations. $iShares 20+ Year Treasury Bond ETF(TLT)$

U.S. stocks: short-term valuations are high, expectations are high, be on the lookout for changes in sentiment when data and policy are not as expected, after the pullback mid-January policy and performance period is a key node to intervene, the index is now at a key support level. $iShares Russell 2000 ETF(IWM)$ $.SPX(.SPX)$ $.IXIC(.IXIC)$ $.DJI(.DJI)$ $SPDR S&P 500 ETF Trust(SPY)$

US Dollar: natural economic fixes and post-election policies have supported it, short-term expectations have dropped the dollar has risen instead, and while too much short-term rise may not be good, it's still strong overall unless there's policy intervention. $Invesco DB US Dollar Index Bullish Fund(UUP)$

Gold has already exceeded the support level c