On Friday, U.S. President Donald Trump and Ukrainian President Volodymyr Zelensky engaged in a heated debate in the Oval Office, with Trump even warning that Ukraine was “gambling on World War III.”

Despite the dramatic confrontation broadcast live for the world to witness, the U.S. stock market displayed relatively little reaction. Instead, traders and investors appeared to focus on the possibility of progress in Russo-Ukrainian peace negotiations.

While the markets initially dipped following the news, volatility quickly subsided, and stocks began to recover. The "fear index" on Wall Street briefly spiked but stabilized shortly after.

Keith Lerner, Co-Chief Investment Officer at Truist Advisory Services, commented that investors seemed to interpret Trump’s remarks as political theatrics rather than a shift in fundamental prospects for peace talks between Russia and Ukraine. “Whether this assessment is accurate or not, the performance of both U.S. and European stock markets suggests that the consensus view remains optimistic about a potential agreement,” Lerner added.

1. Is the Russo-Ukrainian Conflict a Core Driver of U.S. Stock Indices?

Not exactly. From the perspective of the United States, the success of peace talks largely determines whether it can extract benefits – such as access to minerals – or not. For Trump’s administration, however, the priority lies in withdrawing U.S. support for Ukraine and reducing America’s fiscal burdens.

Thus, regardless of how the peace process unfolds, the U.S.'s eventual disengagement from the conflict seems inevitable. For U.S. stock indices, this implies that the impact of the conflict itself remains modest, with market sentiment playing a more significant role than actual fundamentals.

The key influences on U.S. stock index trends remain the tug-of-war between Trump’s tariff policies and the Federal Reserve’s stance on interest rate cuts. In March, 25% tariffs on goods from Canada and Mexico will take effect, and similar measures for European Union imports are forthcoming. There is also the possibility of increased tariffs on China. Against this backdrop, inflation expectations are likely to rise, leaving the Fed constrained in its ability to implement significant rate cuts.

If economic data weakens and investors fail to see the Fed step in with rate cuts to support the market, stock indices could face significant challenges. In such a scenario, investors are advised to temper expectations for a strong rebound in the indices.

2. Technical Analysis of U.S. Stock Indices

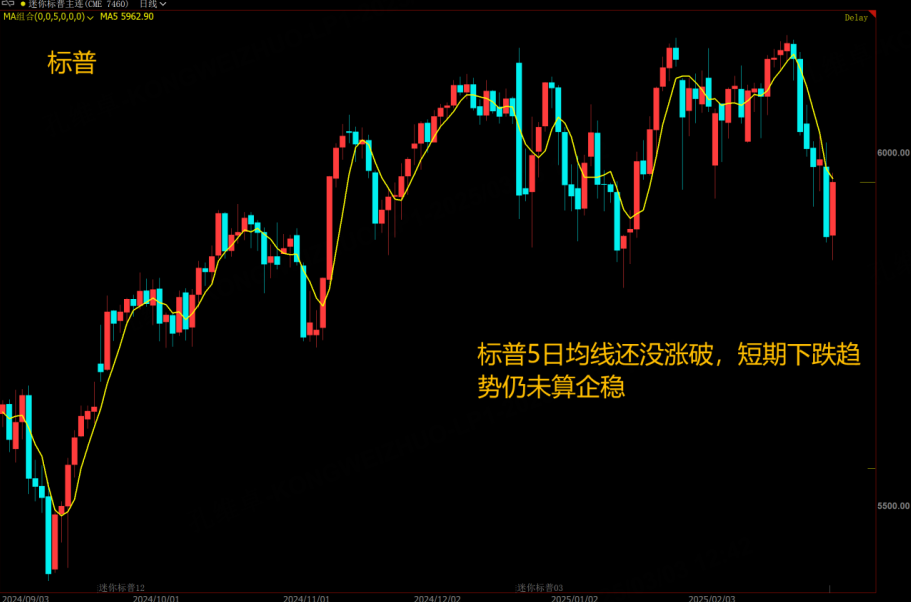

From a technical perspective, U.S. stock indices have already fallen below their 20-week moving averages, suggesting a period of heightened volatility ahead. Investors should closely monitor resistance at the 20-day moving average, which corresponds to the S&P 500 level of 6,050. If the index fails to break through this resistance, it could enter another downward cycle.

During a live-streamed session on Thursday, historical data indicated that the minimum correction for U.S. stock indices in similar phases has been approximately 10%, which would place the S&P 500 level around 5,500. Therefore, investors should remain cautious and prepared for potential risks. After a phase of risk release, better opportunities for capturing rebound momentum may arise. For now, patience and a wait-and-see approach appear to be the prudent strategy.

3. Has Gold Adjusted Enough?

After eight consecutive weeks of gains, gold prices finally experienced a pullback last week. While the decline was not significant, the prices remain far from their long-term moving average and cannot yet be considered at a relatively safe level.

Currently, gold’s 20-week moving average sits near the 2,750 level, which is over 100 points below its current price. It is possible that gold will need to touch this level next week before staging an effective rebound. As such, investors looking to buy on dips may want to wait for further adjustments.

Though the heated exchange between the U.S. and Ukraine might provide a short-term boost to gold prices next week, it is unwise to rely on this too heavily. Speculations that the U.S. is restocking its gold reserves or conducting inventory audits to drive gold prices higher remain unsubstantiated and appear to be driven by emotions rather than facts. A cautious approach is recommended in this regard.

$E-mini Nasdaq 100 - main 2503(NQmain)$ $E-mini S&P 500 - main 2503(ESmain)$ $Gold - main 2504(GCmain)$ $E-mini S&P 500 - main 2503(ESmain)$

Comments