Why this time, US Treasuries decides all assets?

Starting from early September, long-term government bonds represented by 10-year U.S. Treasuries have rapidly increased. On October 3rd, the yield on the 10-year government bond surpassed 4.81%, and the 10-year TIPS yield exceeded 2.45%, marking new highs since 2007 and 2008, respectively.

This has had a global impact, with pressure on U.S. stocks and other emerging markets, and a significant drop in the price of gold. As October began, U.S. bond yields started to retreat, and the U.S. stock market saw some degree of rebound.

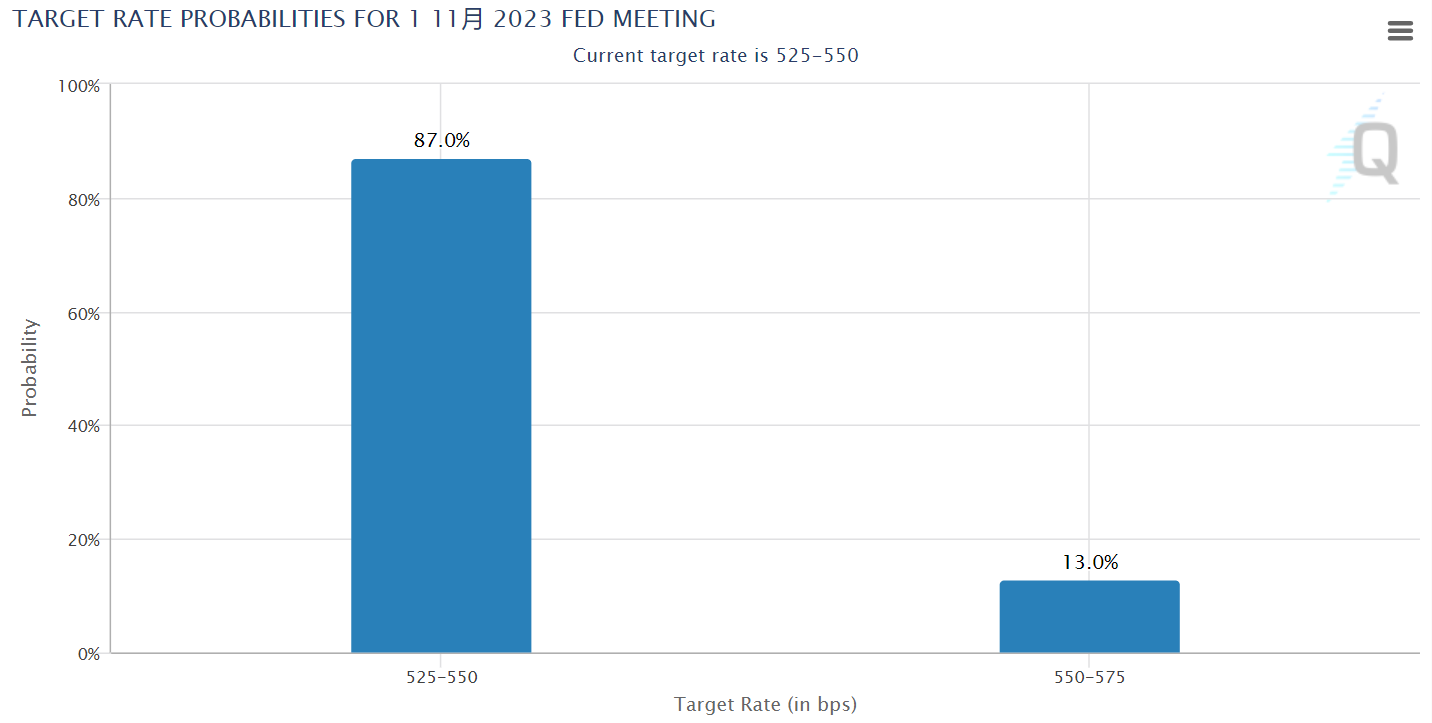

With the recent surge of the "anchor of global asset pricing," an increasing number of senior Federal Reserve officials believe that the sharp rise in U.S. Treasury yields, tightening financial conditions, can substitute for further increases in the benchmark interest rate. Yesterday, the hawkish Dallas Fed President Logan and Federal Reserve Vice Chairman Jefferson both mentioned this.

Characteristics 10Y T-bond yield surge

1. Real interest rates, not inflation expectations, are the main contributors, indicating that strong growth, not high inflation, is the primary driver.

The rise in nominal interest rates on the 10-year U.S. Treasuries is almost entirely driven by real interest rates, which increased from 1.82% to 2.58%, contributing 77 basis points to the 83 basis points increase in nominal rates, while inflation expectations only rose by 6 basis points and continued to fall after entering October. Therefore, the recent rise in long-term U.S. bond rates reflects more the resilience of the U.S. economic growth rather than the risk of a significant increase in inflation. This also explains why U.S. stocks, especially the Nasdaq, have not been heavily impacted by this round of rising interest rates. If it were driven by inflation expectations, it might have put significant pressure on growth stocks, causing greater stress on the Nasdaq. $NASDAQ(.IXIC)$

2. Driven by the term premium: In fact, since the second quarter of this year, the rapid increase in 10-year U.S. bond rates has been mainly driven by the term premium.

Since September, the term premium on 10-year U.S. bonds has increased from -0.5% to 0.3%, while rate expectations have risen and then fallen, with an overall small decline. The divergence in term premium and rate expectations indicates that investors have not changed their pricing of the current rate hike path; rather, it reflects an increased need for risk compensation when holding long-term government bonds.

The need for more risk compensation is due to the uncertainty of the delayed rate hike path and the increase in bond supply caused by the surge in U.S. Treasury issuance.

This is largely consistent with the information conveyed by the Federal Reserve's September FOMC, which indicated a commitment to maintaining rates at high levels for a longer duration. The implied rate hike path in recent CME interest rate futures has not seen significant changes. However, term premiums show distinct mean-reverting characteristics, leading to stronger pullback pressure once they reach a certain height.

However, changes in supply and demand in the secondary market could also impact U.S. bond yields in the opposite direction.

T-Bond’s Supply and Demand

From the demand side, major investors have a lower appetite for holding bonds. International investors such as the Bank of Japan and $iShares MSCI Japan ETF(EWJ)$ the People's Bank of China $China A50 Index - main 2310(CNmain)$ are reducing their holdings overall (the possibility of normalizing monetary policy has increased gradually following an upward adjustment in the Japanese YCC ceiling). Even the Federal Reserve is steadily reducing its holdings of U.S. bonds through quantitative tightening, and the willingness of domestic U.S. investors to purchase bonds is currently not strong.

The primary sources of incremental demand are currently pension funds with requirements for long-term yields and liquidity, as well as hedge fund investors.

On the supply side, the U.S. government's debt issuance has reached record highs, and a new fiscal budget bill has been passed, with expectations of further increases in the coming year. However, the expansion of the U.S. fiscal deficit continues to cast a shadow over the financial markets.

The ongoing Israeli-Palestinian conflict may increase defense spending in the 2024 fiscal year.

with the removal of House Speaker McCarthy, an increase in conservative Republican influence, intra-party disputes, and factors related to the 2024 elections. As a result, Congress may still be unable to approve the fiscal year budget by the end of January 2024, causing further anxiety.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Japanese bond crisis could send shockwaves into Western markets. If the BoJ can’t get bond yields under control they will begin force selling US treasuries before power buying the Yen to avoid a currency collapse.

Search for haven assets feeds rally in US Treasuries. Investors scale back rate rise expectations as bond markets respond to Hamas attack on Israel.

Public consensus is that a short squeeze in US Treasuries is imminent.

Treasuries need liquidity … check… where will we get the liquidity?

Great ariticle, would you like to share it?