25bps or 50bps Rate Cut? Employment Data is Crucial

In his Jackson Hole speech, Powell made it clear the Fed intends to cut rates, but stated "the timing and pace of rate cuts will depend on incoming data, the evolving outlook, and the balance of risks."

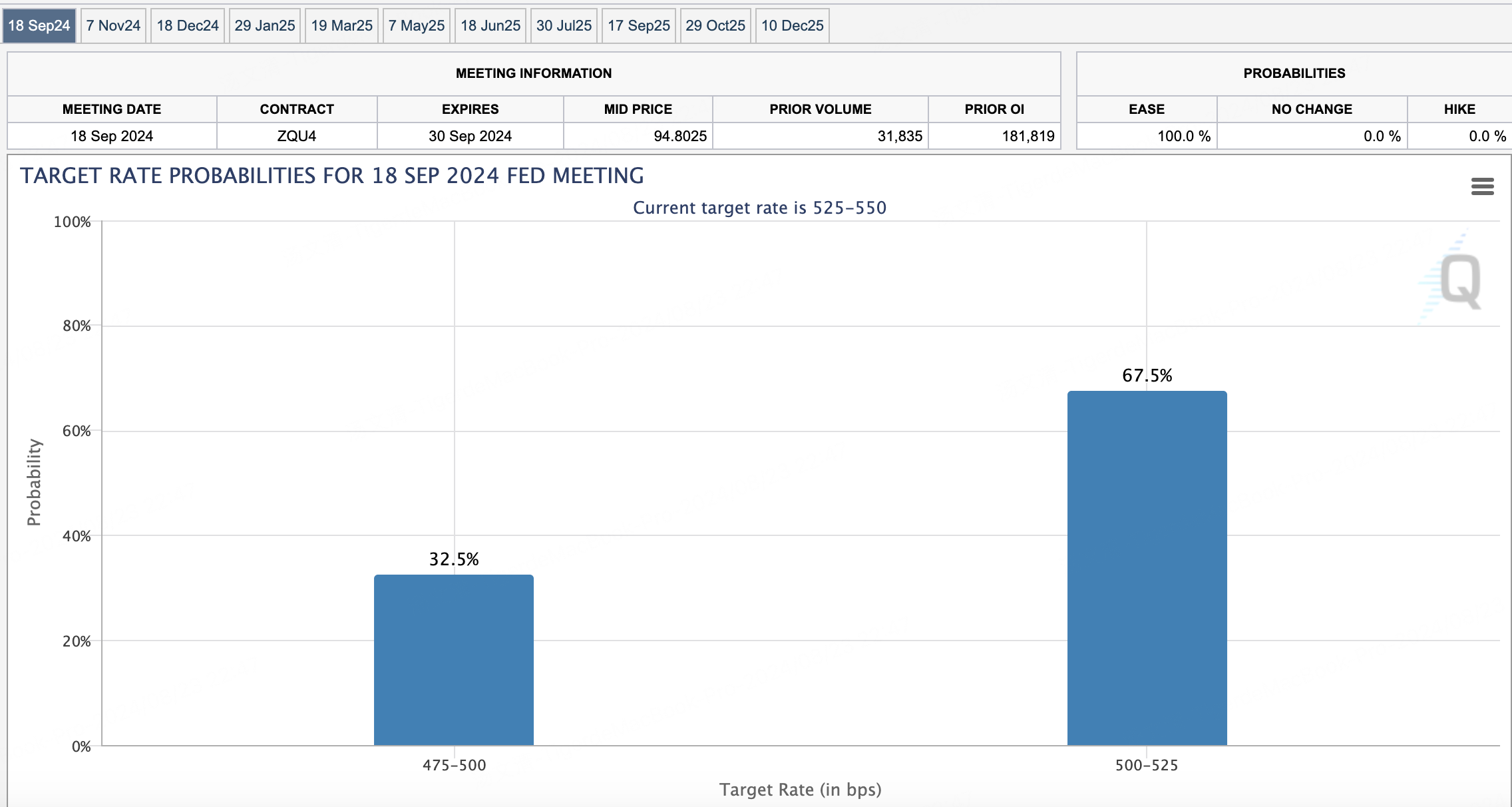

Market pricing currently shows a 67.5% probability of a 25bps cut in September and a 32.5% chance of a 50bps cut.

This suggests expectations for softer, but not drastically weak, economic data (including non-farm payrolls and CPI) between now and the September 20th FOMC meeting, warranting a 25bps ease. A 50bps cut is the lower probability scenario if data disappoints significantly.

An even lower probability event would be resilient data that convinces Powell to stand pat in September and wait until November.

In his policy outlook, Powell emphasized labor market performance:

Today, the labor market has cooled considerably from its formerly overheated state. The unemployment rate began to rise over a year ago and is now at 4.3 percent—still low by historical standards, but almost a full percentage point above its level in early 2023 (figure 2). Most of that increase has come over the past six months. So far, rising unemployment has not been the result of elevated layoffs, as is typically the case in an economic downturn. Rather, the increase mainly reflects a substantial increase in the supply of workers and a slowdown from the previously frantic pace of hiring. Even so, the cooling in labor market conditions is unmistakable. Job gains remain solid but have slowed this year.4 Job vacancies have fallen, and the ratio of vacancies to unemployment has returned to its pre-pandemic range. The hiring and quits rates are now below the levels that prevailed in 2018 and 2019. Nominal wage gains have moderated. All told, labor market conditions are now less tight than just before the pandemic in 2019—a year when inflation ran below 2 percent. It seems unlikely that the labor market will be a source of elevated inflationary pressures anytime soon. We do not seek or welcome further cooling in labor market conditions.

Note his final line - the Fed do not seek or welcome further cooling in labor market conditions.

With the focus shifting to averting recession risks, employment data may become more market-sensitive than inflation readings.

Unsurprisingly, Powell's comments spurred hedging flows like this $SPY$ put spread:

Buy $SPY 20241018 535.0 PUT$

Sell $SPY 20241018 529.0 PUT$

Essentially, traders are re-pricing downside risks based on prior lows.

However, I don't expect an aggressive consensus shift until after next week's $NVDA$ earnings, as both bulls and bears fear being wrong-footed by the print.

NVDA has also seen defensive positioning, albeit in a very cost-efficient manner:

Buy $NVDA 20250321 94.0 PUT$

Sell 10x $NVDA 20251219 19.0 PUT$

This trade buys the March 2025 94 puts but funds over 90% of the premium by selling 10x the Dec 2025 19 puts, a strike so deeply out-of-the-money it represents virtually free upside.

It perfectly captures the market's post-Powell sentiment - unsure when the jobs picture could crack, but wanting very inexpensive lottery ticket downside ahead of a potential 50bps surprise.

No major new $NVDA$ call overwriting was initiated this week, as institutions have already rolled their exposure out to the August 30th 130 calls - either setting the expected earnings ceiling, or leaving room to re-strike if needed.

While put open interest points to a 120 near-term floor, earnings weeks often distort typical ranges, so respecting previous lows is prudent.

TSLA has seen institutions roll their covered call exposure to next week, selling the $TSLA 20240830 225.0 CALL$ .

Notably, this roll happened on Thursday, suggesting they expect TSLA to simply tread water in the lead up to the Jackson Hole event risk.

I continue to overwrite at $TSLA 20240830 230.0 CALL$ and $TSLA 20240830 190.0 PUT$ for a near-neutral stance.

$Coinbase (COIN)$ has also seen two waves of covered call rolls, at the 215 and 217.5 strikes:

Sell $COIN 20240830 215.0 CALL$

Sell $COIN 20240830 217.5 CALL$

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- phongy 45·08-24could we trust Powell?LikeReport

- NicknameTiger·08-25August 25bps cut?LikeReport

- KSR·08-25👍LikeReport

- eo1668·08-25okokLikeReport

- Basics101·08-24Nice write up!LikeReport