Sectors Recap: Indexes fell nearly 2%, Consumer Defensive Won

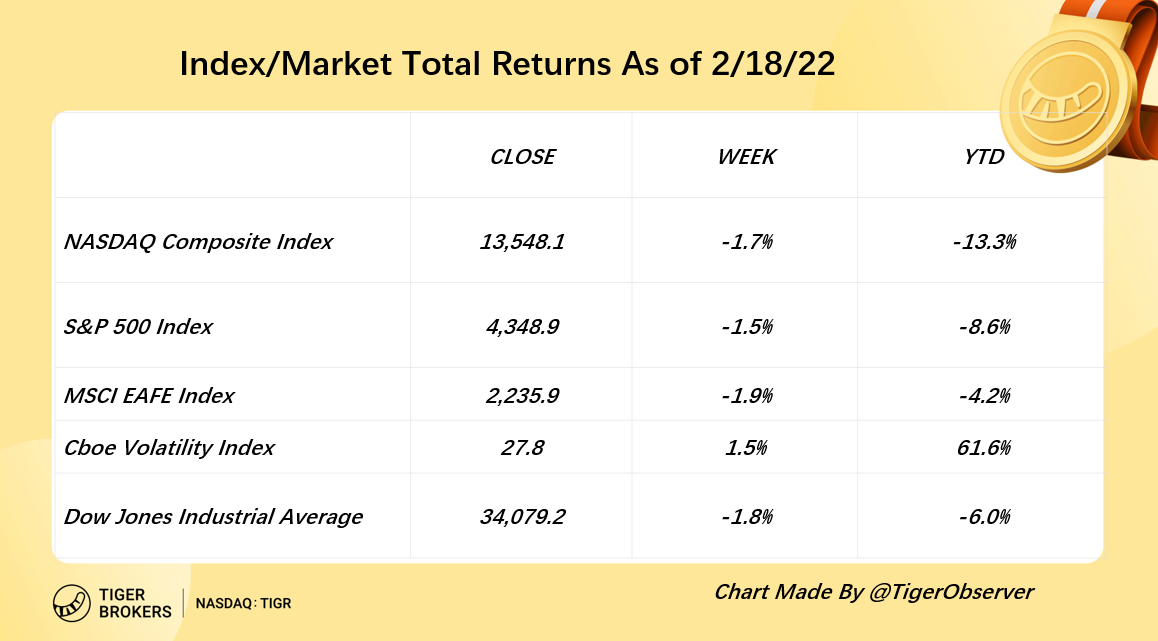

The major U.S. stock indexes appeared to be on the verge of an overall gain at midweek, only to end up negative after declining on Thursday and Friday. Indexes fell nearly 2%, and military tensions on the Russia-Ukraine border appeared to drive the markets.

Weekly Index Returns from Last Week

Other Markets:

- Amid inflation concerns and rising geopolitical conflict, the price of gold futures briefly eclipsed $1900, climbed to its highest level in about eight months, marking a 6% increase from a recent low in late January.

- U.S. crude oil prices were as high as $95 but retreated to around $92 on Friday, last week, an eight-week rally that pushed. The potential for additional oil exports from Iran helped to offset concerns related to supply disruptions stemming from the continuing Russia-Ukraine conflict.

- The yield of the 10-year U.S. Treasury climbed as high as 2.06% on Wednesday—the highest since July 2019—before slipping down to around 1.93% on Friday.

Macro Factors:

- Retail Comeback: U.S. retail sales rebounded by 3.8% from a decline of 2.5% in December, as a surge in online purchases and increased sales of furniture helped to fuel better-than-expected growth in January. High inflation also helped to boost the latest monthly retail sales total.

- Unemployment Rose:Two economic releases indicated potential weakness in the U.S. economy. The latest weekly tally of new claims for unemployment benefits rose to 248,000, marking the first increase in four weeks.

- Earnings Streak: With 86% of S&P 500 companies having reported fourth-quarter results as of Friday, earnings season was on track to record year-over-year profit growth exceeding 30.0% for the fourth quarter in a row.

- Small-cap Outperformed: The small-cap benchmark, Russell 2000 Index, has risen about 0.3% over the past two weeks, while its large-cap counterpart has fallen nearly 4%. Showing U.S. small-cap stocks have outperformed large caps for the past two weeks.

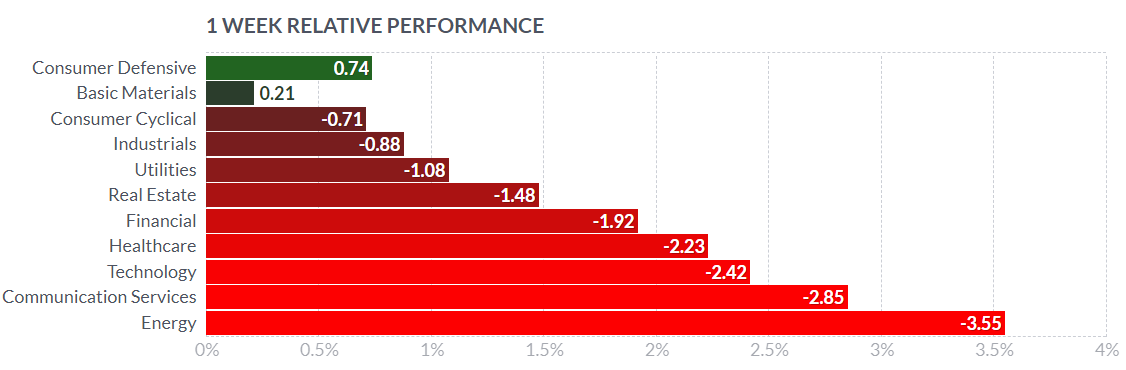

S&P 500 11 Sectors Performances:

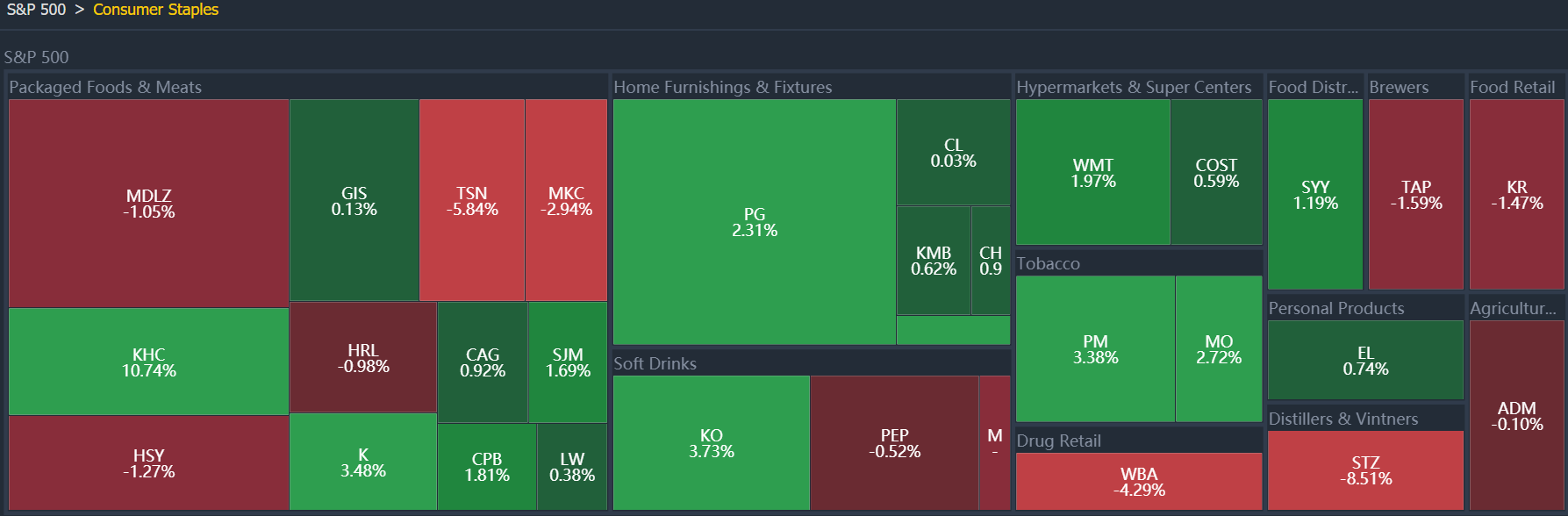

Last week, Consumer Defensive & Basic Materials Sectors got less 1% increase. Engergy Sector leading the retreatment, then, Communications Services.

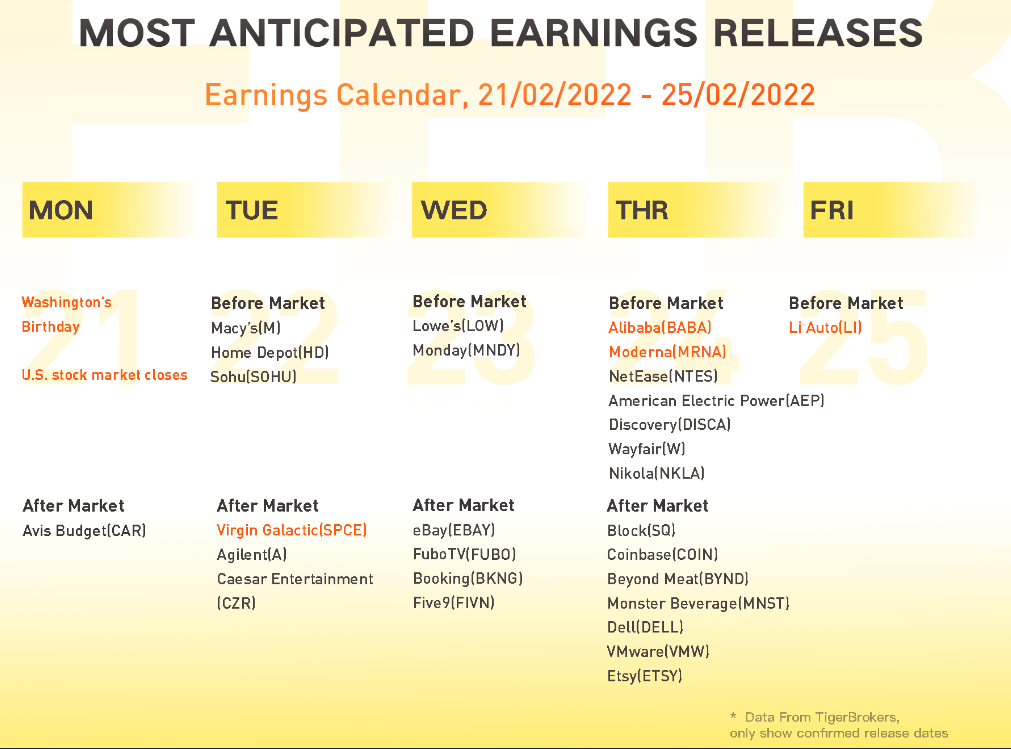

Most Anticipated Earnings Releases: February 21-24

The Week Ahead: February 21-24

Related Reading:

Recap: Positive Q4 Earnings Season But Biggest Moves of Stocks

Cash Flow is King: Factors Driving Returns Over The Next Decade

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Good