I. Review of weekly Market

With the landing of Jackson Hole Annual Meeting, Powell's speech was neutral and hawkish, and the economic data fell short of expectations, which eased hawkish concerns. The market generally expected that the probability of suspending the rate hike in September was high, and the yield of 10-year US bonds peaked and fell back.

Although it was difficult to change the Fed's policy of maintaining high interest rates in the short term, the Fed's rate hike cycle entered the middle and late stage, and the yield of 10-year US bonds fell back after the short-term risk factors landed, which led to the repair of risk appetite in the equity market.

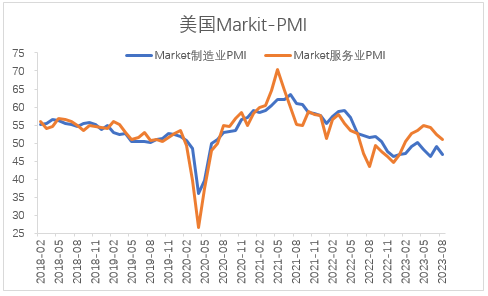

However, the recent Markit manufacturing PMI and service PMI in August fell short of expectations, and the economic growth gradually slowed down. The data released on August 23 showed that the initial value of Markit manufacturing PMI in the United States in August recorded 47, the previous value was 49, and it is expected to be 49.3; In August, the initial value of Markit service PMI in the United States recorded 51, the previous value was 52.3, and the expected value was 52.2. In August, the PMI of Markit manufacturing and service industry in the United States fell less than expected, and the PMI of service industry remained above threshold.

The growth rate of service industry slowed down but generally maintained an expansion trend, which formed a certain support for consumption and employment. The manufacturing industry continued to shrink, and the bottom was repeated, or gradually entered the middle and late stage of active destocking.

The market expects ISM manufacturing and service industries to continue to decline, but the PMI of service industries may maintain certain resilience. Although the economic data is mixed and the economic growth rate is gradually slowing down, the resilience of service industries makes the primary goal considered by the Federal Reserve at present still the inflation level.

Figure 1: PMI of Markit Manufacturing and Services in the United States

Source: Wind International Derivatives Think Tank

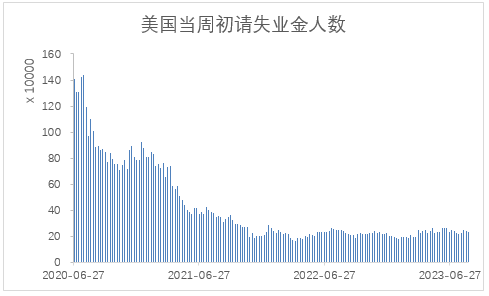

The number of jobless claims in the United States exceeded expectations at the beginning of the week, and the job market remained resilient. According to the data released on August 24th, the number of jobless claims in the United States recorded 230,000 in the week ending August 19th, with the previous value of 240,000 and the expected number of 240,000. The number of jobless claims in the United States exceeded market expectations at the beginning of the week.

The non-agricultural employment data in June showed that the job market was still strong, and there was still a gap in the US labor market. However, the impact of rate hike and economic downturn gradually transmitted downward, and the number of jobless claims briefly bottomed out at the beginning of the week

Figure 3: Number of jobless claims in the United States at the beginning of the week

With the landing of Jack Holson's annual meeting, the market's worries about the hawkish operation of the Federal Reserve slowed down, while economic data showed that the service industry and job market in the United States still maintained certain resilience.

Powell also said in his speech that he was mainly concerned about the performance of inflation data. The expectation of suspending the rate hike in September warmed up, and the rate hike might be restarted in November. The short-term rate hike disturbance marginal weakened, and the yield of 10-year US bonds fell, which benefited the performance of US stocks to a certain extent.

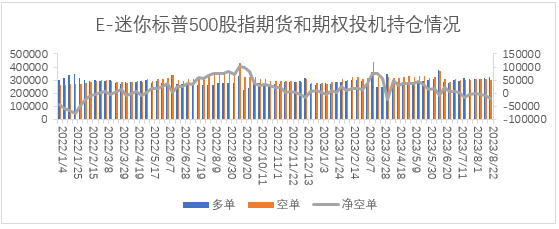

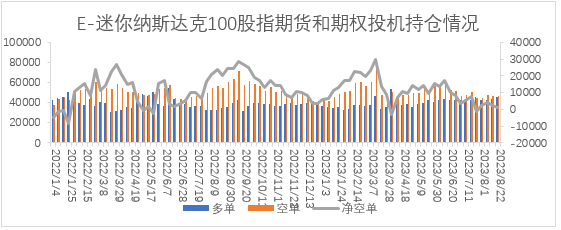

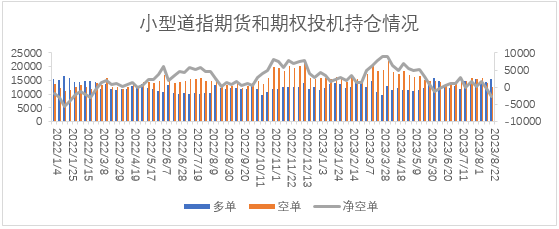

Position analysis

According to data released by the US Commodity Futures Trading Commission (CFTC), as of the week of August 22, Position situation shows that the net short power of the big mini index futures contract weakened obviously and the long power increased last Wednesday.

Figure 4: Changes in speculative positions of mini S&P 500 futures options

Source: CFTC official website International Derivatives Think Tank

Figure 5: Changes in speculative positions of E-mini Nasdaq 100 futures options

Source: CFTC official website International Derivatives Think Tank

Figure 6: Changes in speculative positions of Dow Jones ($5) futures options

Source: CFTC official website International Derivatives Intelligence

Market Outlook

From a fundamental point of view, the U.S. economy remains resilient. Although the downward pressure on the economy appears, the service industry is relatively strong.

At the same time, the inflation level in Europe and the United States remains high. Under the background of repeated crude oil prices, inflation may be repeated. At the Jack Holson annual meeting, the attitudes of European and American central banks remained neutral and hawkish, and the US Treasury yields was difficult to go down in the short and medium term.

However, the Fed's worries about the rate hike in September weakened, the short-term ten-year U.S. debt yield fell, and the interest rate and risk appetite in the U.S. stock market were repaired.

On the whole, with the landing of Jack Holson's annual meeting, the worries of market hawks are gradually digested, the yield of 10-year US bonds may gradually stabilize, and it is more likely that US stocks will continue to fluctuate and rebound.

However, it should be noted that the economic data such as non-agricultural employment in July of the United States will be released this week, which will interfere with the economic and rate hike expectations to some extent. It is expected that there is a high probability that US stocks will continue to fluctuate in the range of top and bottom.

$E-mini Nasdaq 100 - main 2309(NQmain)$ $E-mini S&P 500 - main 2309(ESmain)$ $E-mini Dow Jones - main 2309(YMmain)$ $Gold - main 2312(GCmain)$ $WTI Crude Oil - main 2310(CLmain)$

Comments