The macro news was another relatively calm day, but enough to scare some traders.

-The US stock market rose, the S&P 500 index broke five consecutive losses and rose by 0.8%, the Dow Jones index rose by 0.5%, and the Nasdaq index rose by 1.1%;

-While stocks rose Thursday, the recent rally in U.S. Treasuries lost momentum. The yield on the benchmark 10-year U.S. debt rose to 3.492% on Thursday from 3.407% on Wednesday. The difference between the yields of 2-10-year government bonds rose by about 1.4 basis points to-82.91 basis points;

-The US dollar index fell and risk sentiment returned. In addition, the seasonal trend in December is usually unfavorable to the US dollar;

-The price of gold was small last week, and it is possible to test $1,800 again;

-Oil prices have fallen for five consecutive trading days, and a major crude oil pipeline is expected to resume operation, which will lead to a large amount of crude oil returning to the market;

-The offshore RMB is basically flat at 6.9626, and the high of 6.93 set on Monday is still an important short-term resistance level (it is reported that an important economic conference in China will be held next week)

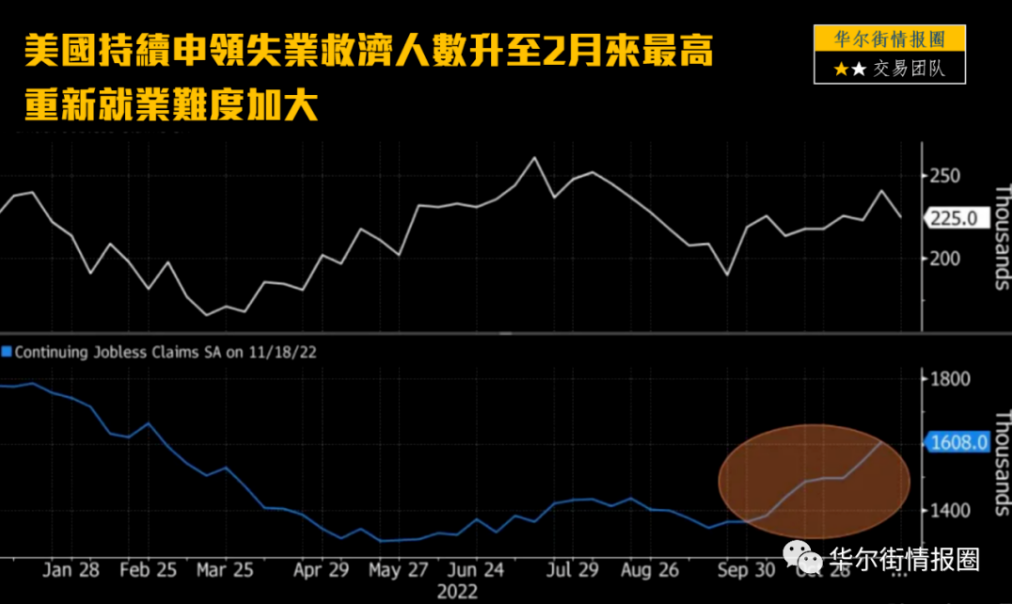

From the market performance, "the dollar fell and other rising patterns" were roughly restored, and traders acted cautiously. Yesterday's low-profile economic data-the number of initial jobless claims in the United States increased slightly last week, while the number of renewed jobless claims hit a 10-month high-"bad news has become good news again" for the market. Originally, this is a data that has not received much attention (because it is published every week and released frequently), but in the absence of news, a small data can reverse the market trend.

However, from this data itself, we can also see a major problem:

-The number of unemployed people in the United States increased by 4,000 at the beginning of last week (little change, no problem);

-In the week ending November 19, the number of people claiming unemployment benefits in the United States increased by 57,000 to 1.6 million, the largest increase in a year (this is the problem).

More recently, analysts are concerned about "sustained jobless claims," an indicator of how easy it is for people to find jobs after losing their jobs, and an early warning indicator of the impending economic recession. Next Thursday evening, we will still focus on this breakdown.

The day before the market was worried about a recession (Wall Street executives warned of an imminent recession), the day after a tiny data triggered a market turnaround, how uncertain our current environment is.

Be careful, today's market volatility may be amplified:

First, today is Friday, which is usually a day with large volatility in a week;

Second, the November PPI data of the United States and the inflation data of the University of Michigan Consumer Confidence Index will be released tonight, which are the two most important economic data this week.

21:30 US November PPI (previous value: 8.00%; Market expectation: 7.1%)

23:00 US one-year inflation forecast for December (previous value: 4.9%)

Third, next week's key events are approaching, which will make some traders leave the market early tonight. CPI data will be released in the United States next Tuesday, and the latest interest rate resolution will be released by the Federal Reserve on Thursday.

$E-mini Nasdaq 100 - main 2212(NQmain)$ $E-mini S&P 500 - main 2212(ESmain)$ $E-mini Dow Jones - main 2212(YMmain)$ $Gold - main 2302(GCmain)$ $Light Crude Oil - main 2301(CLmain)$

Comments