Four Reasons Make META The Impressive Guidance

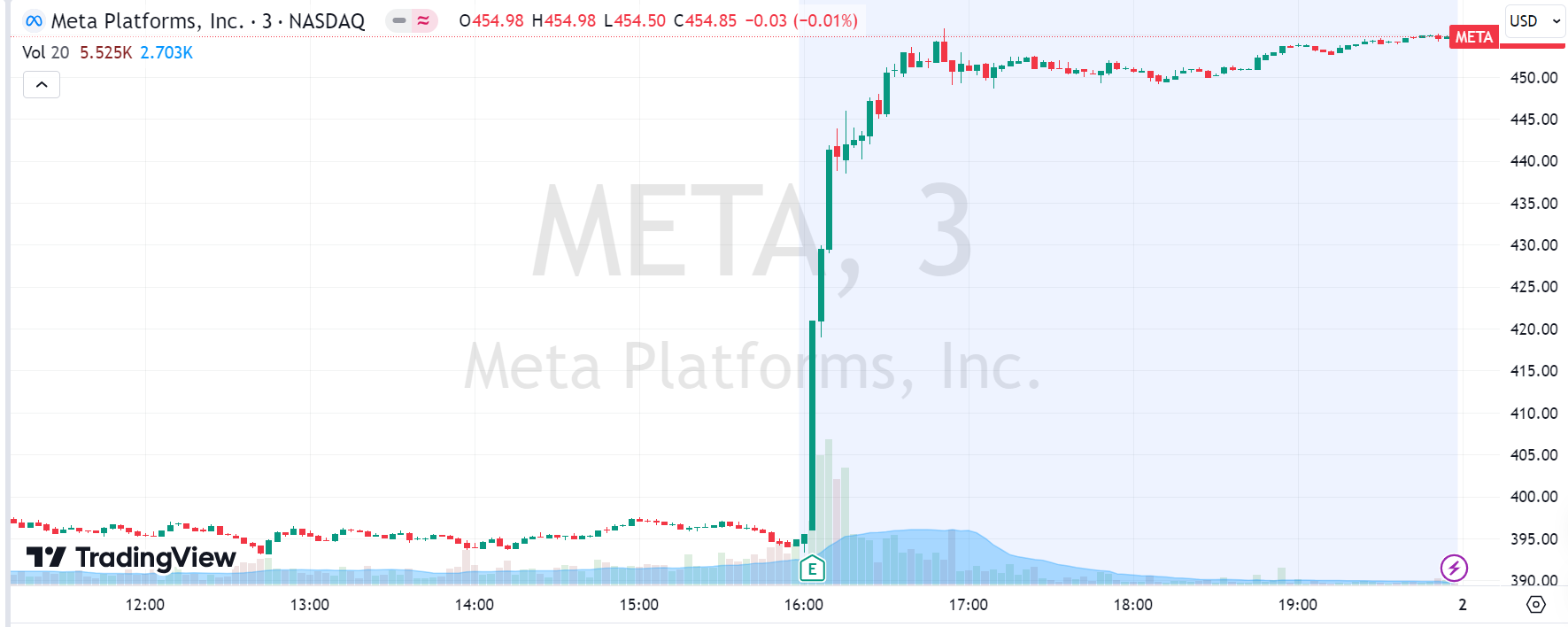

Excellent 23Q4 earnings with significantly guidance raising, while initiating first-ever $50 billion share buyback and a $0.5 per share dividend, $Meta Platforms, Inc.(META)$ delivered a super pleasing news to its investors with historical 16%+ surge in post-trading.

$Alphabet(GOOG)$ ‘s slightly miss in advertising (browsers advertising) the day before lowers some investors’ expectations for META.

Truth is, META proved that social media and short-video advertising, with their broader audience and more efficient conversion, along with AI assistance, are more favored.

Investment highlights

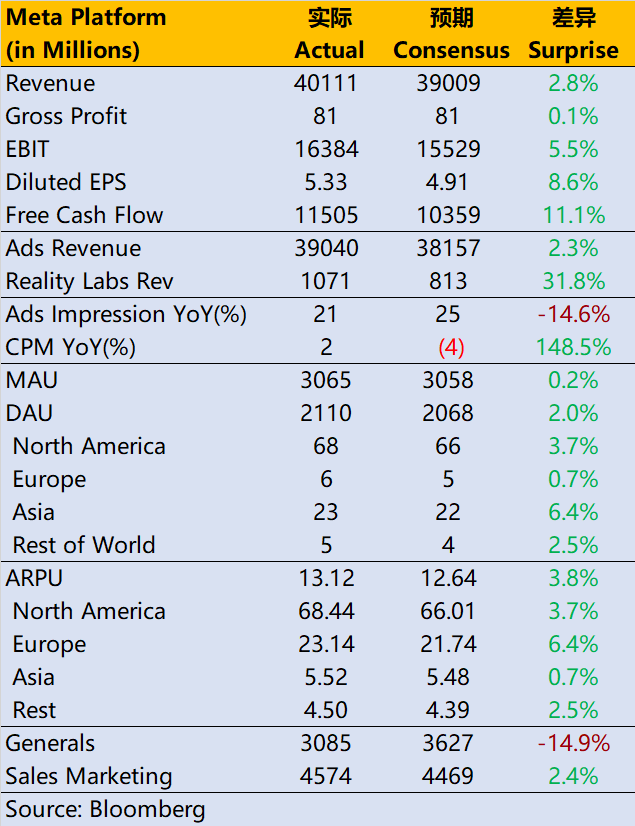

1. User base continues to expand even with a hyper base, supporting the simultaneous increase in advertising revenue. In Q4, Meta's social matrix saw a 6.4% increase in monthly active users, which is very impressive considering the base of 3 billion.

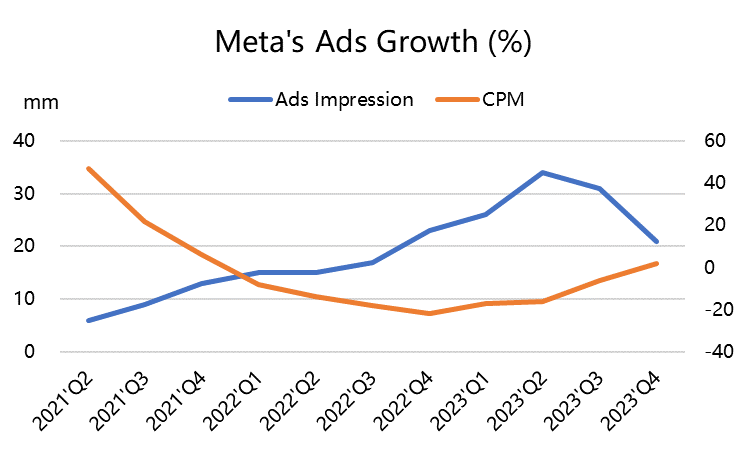

Advertising revenue reached $39 billion, a year-on-year increase, higher than the market's expected $38.2 billion. Meanwhile, the cost per thousand impressions (CPM) increased by 2%, while the market expected a 4% decrease; impressions increased by 21% year-on-year, compared to the market's expectation of 24%.

Overall, both volume and price increased simultaneously. This also indicates that Reels' commercialization is progressing smoothly, as it is not only a major incremental factor but also because it was previously part of the promotion cycle that lowered overall pricing, which has now increased back.

On one hand, this indicates strong economic growth in the United States, especially in the consumer industry. On the other hand, it also indicates intense competition among advertisers, especially in the consumer brand industry.

2. VR products are still in a waiting period, and losses are within expectations. Due to their low share, the entire VR industry still needs more mature products to develop the developer ecosystem. Apple's Vision Pro may bring some stimulation, but it is too early to become a phenomenal product. Therefore, the short-term goal of the VR business is to reduce losses.

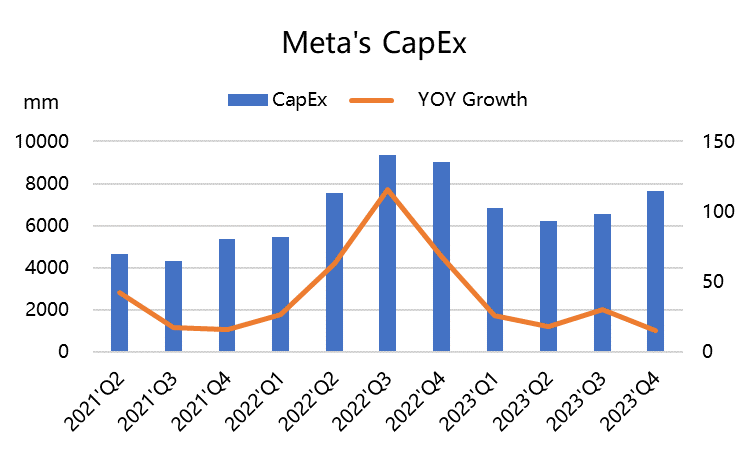

3. Extreme cost-efficiency improvement, META is more like a "profit maker" with AI. Capital expenditure remained at $7.9 billion, a decrease from $9.2 billion in 22Q4 (before the GPT explosion).

After open-sourcing Llama 2 models, Meta focuses more on cultivating the overall ecosystem. Under the AI business, advertising may be the easiest to monetize or improve monetization efficiency, thus further benefiting Meta as a "profit maker."

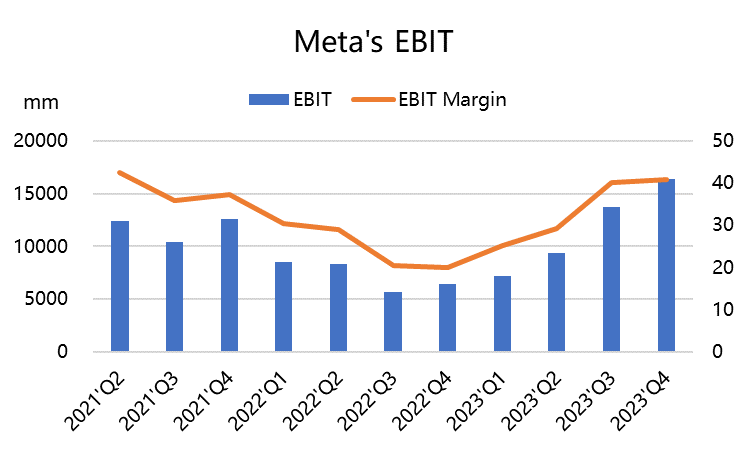

4. Margins continues and will continue to increase. The increase in advertising prices also led to a 7-percentage-point year-on-year increase in gross profit margin (from 74% to 81%), exceeding the previous high before the iOS privacy policy changes. Net profit also reached $14 billion, further strengthening an already very strong cash flow and assets.

As dollar-denominated assets retain value in a high-interest-rate environment, they provide strong support for the company's valuation. Q4 is still downsizing, and the costs including restructuring have increased compared to the previous period. It is expected that there is still room for improvement in profit margins in the later period.

Four Reasons make the Impressive Guidance

1. Stable and positive operating data support. This includes short video Reels and Threads, which are attempting to challenge X (formerly Twitter). The MAU of the Facebook Family increased by 6.7% year-on-year, and DAU increased by 5%. The Asia-Pacific region is the main driver of new active users, which is quite interesting.

2. Chinese companies’ overseas presents.. Not only major players like Temu and Shein are going global, but also more cross-border e-commerce and gaming companies are becoming the main force in expanding overseas. Due to the "Deinflection" market environment in China, the overseas market has become more important, leading to intense competition. As these companies have good cash flow, their long-term advertising investment sustainability is strong.

3. Advantage of election year political spending. Many countries have election demands this year, and not only traditional social media platforms like Facebook are important battlegrounds, but Threads also carry a lot of "political overflow demand" from X, which is expected to bring in revenue.

4. Benefits from AI. The capital expenditure for 24 is expected to be 30-37 billion, with AI being the main direction. Not only can the open source of Llama 2 improve the overall developer environment, but it can also promote the monetization of more mature AI products through social media platforms.

Is Meta still on the way of all time high?(Single choice)

Is Meta still on the way of all time high?(Single choice)Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- skippix·02-02Agree! META's impressive growth potential. $META $GOOG.LikeReport

- 不死鸟.·02-05👌🙏LikeReport

- MIe·02-03Meta wowLikeReport

- linrui·02-02impressed!LikeReport

- Tom Chow·02-02goodLikeReport

- YueShan·02-02Good⭐️⭐️⭐️LikeReport