Why I Believe The Coming Gold Surge Could Be Bigger Than You Imagine

The U.S. dollar has been unusually weak recently, and multiple signs suggest this choppy weakness may persist for a while longer. The real turning point is likely to fall somewhere between March and April this year.

First, China’s official USD/CNY fixing was set around 6.9 today—previously it had been in the 7-handle. This is the strongest official RMB fixing since 2023, and with the official rate now back below 7, it indicates the dollar has indeed remained weak lately. The central bank apparently does not see a problem with setting the fixing this strong。

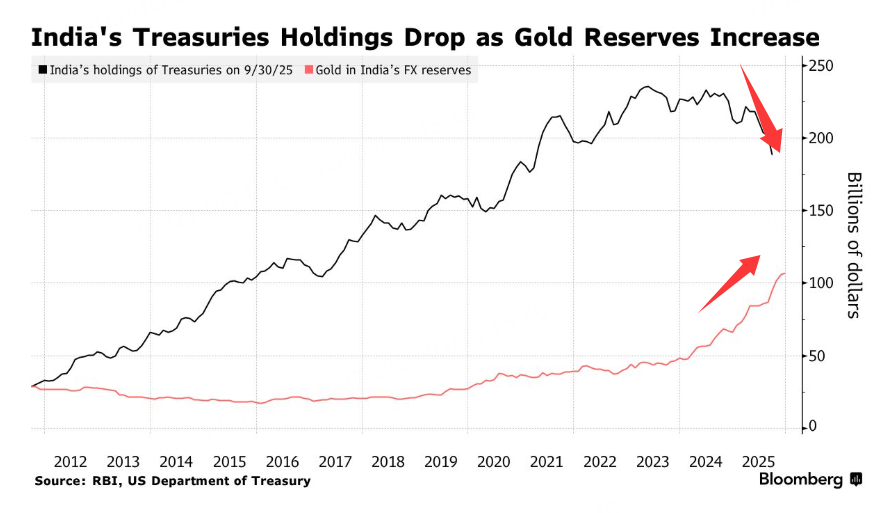

Second, Bloomberg reported that India again sold a large amount of U.S. Treasuries over the most recent month.

India’s U.S. Treasury holdings have now fallen to the lowest level in five years. Data released last week show India’s long-term U.S. debt holdings have dropped to USD 174 billion, down 26% from the 2023 peak. A year ago, U.S. Treasuries accounted for 40% of India’s FX reserves; now that share is only about one-third. India’s Treasury holdings are only about one-quarter of a certain country’s holdings. India’s selling looks even more aggressive than China’s and Japan’s. From a geopolitical standpoint, India does not appear to be engaged in a political confrontation with the U.S., so this selling may simply reflect a view that Treasuries are overpriced or risky.

$20+年以上美国国债ETF-iShares(TLT)$ $10年美债主连 2603(ZNmain)$ $美元指数(USDindex.FOREX)$ $做空美元指数-PowerShares(UDN)$ $MSCI 印度(美元)指数期货主连 2601(MNDmain)$

Look at the scale of the selling: the black line. Then compare it with the red line, which shows India’s increased gold holdings—rising continuously. That is why it is difficult for gold not to go up.

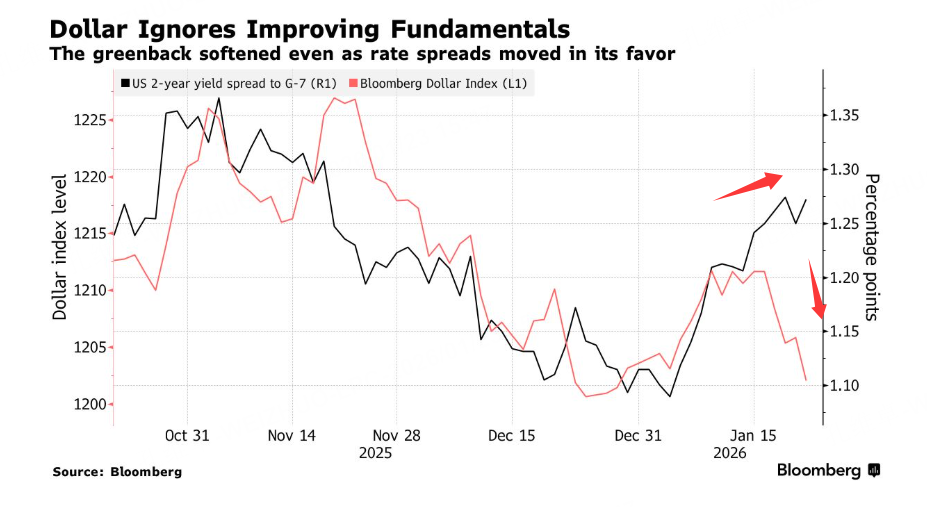

In addition, the relationship between the dollar index and the spread between U.S. 2-year yields and G7 yields has diverged. Even though U.S. yields have continued to rise relative to the G7, the dollar index has not risen as it typically would. This suggests investors remain cautious about the value of U.S. Treasury assets.

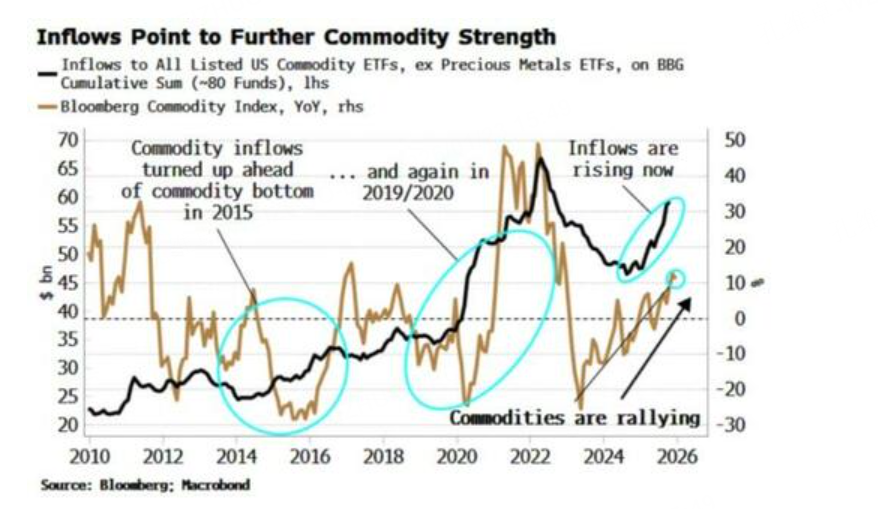

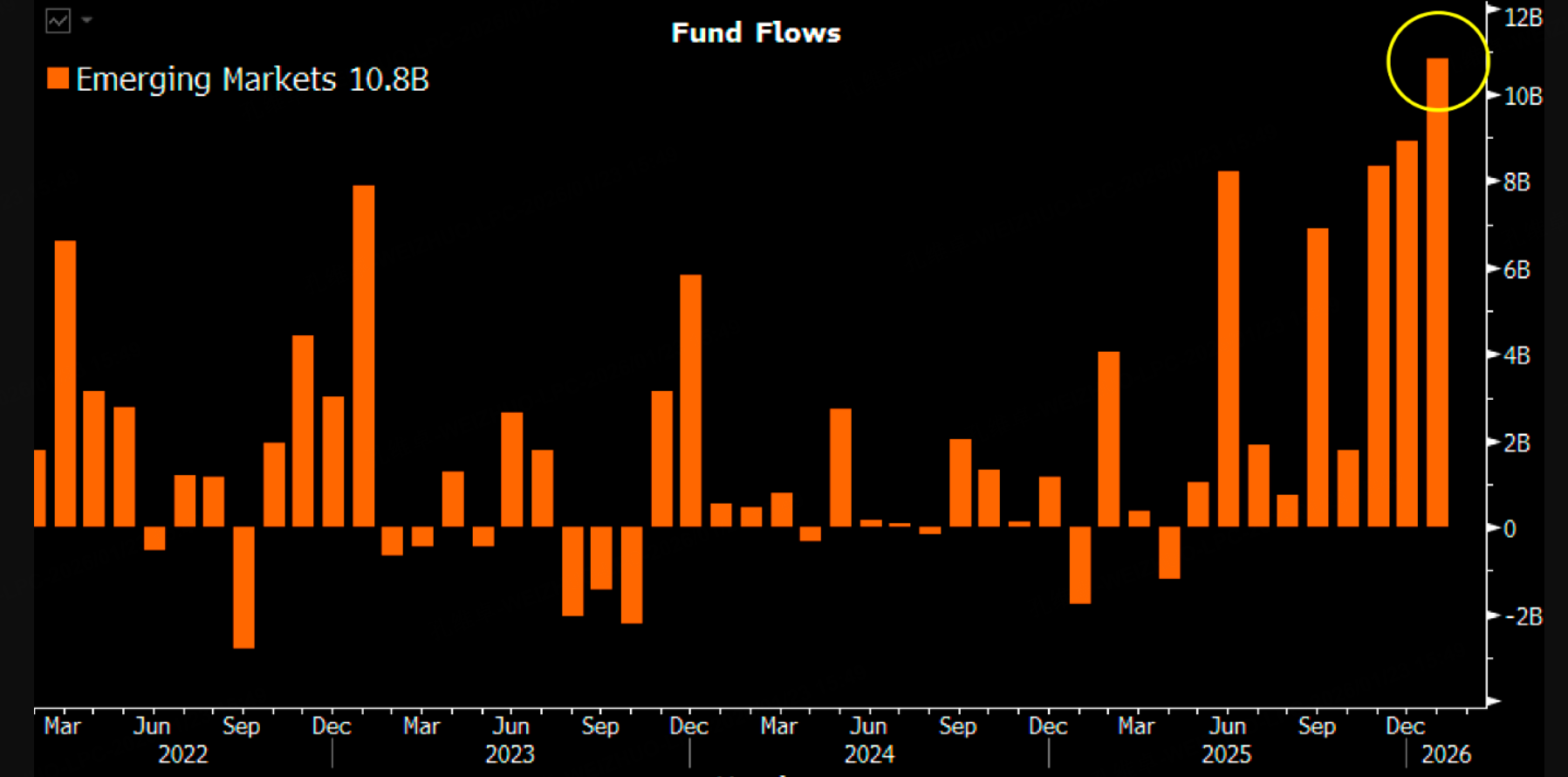

The dollar’s sudden weakness feels unusual. Over the past year, capital has been flowing into commodities and emerging markets.

commodities: $材料ETF(XLB)$ $ProShares做空大宗商品ETF(SBM)$ $SSE COMMODITY ETF(510170)$

Emerging markets

$iShares MSCI Emerging Markets ETF(EEM)$

How long can this process last, and how durable is it? The expectation is that it may continue throughout Q1. Based on historical patterns, the dollar index may only rebound around the start of Q2.

A separate point that aligns with this cycle: March silver delivery volume is too large and CME inventories are insufficient. That implies silver futures may still struggle to see a major drop in February trading. From a cyclical perspective, these factors line up.

In other words, this phase of choppy dollar weakness may last until March–April. During this window, emerging markets, Hong Kong/China A-shares, and gold and silver should be relatively strong—unless some major event abruptly lifts the dollar index. At the moment, the only clear scenario that could cause a sudden dollar surge would be the Fed unexpectedly turning much more hawkish. Otherwise, it may be difficult for the dollar to regain strength in the short term.

Now to the second topic: Silver and Gold

According to CME (the Chicago Mercantile Exchange), current open interest in silver is 150,200 contracts. Each contract represents 5,000 ounces of silver, so the total amount implied for delivery is 751 million ounces; however, CME-registered inventory in warehouses is only 410 million ounces.

Of course, not every open futures contract will require delivery, but the gap is still very large. This mismatch is a key reason many believe silver could continue to rise. Many participants want to take delivery as soon as possible in March to obtain physical silver, which could keep the spot market’s high premium from easing. As a result, from February into March, silver may remain volatile at elevated levels and be difficult to push lower.

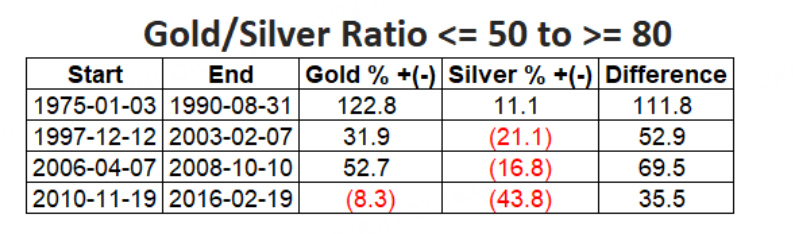

However, a key point to watch is that the gold–silver ratio has reached an extreme historical level: 50

At such times, history suggests leadership between gold and silver may switch—from “gold weak, silver strong” to “gold strong, silver weak.”

Looking at four historical instances where the gold–silver ratio fell below 50, gold rose more aggressively than silver.

Based on this, the current expectation is to place a provisional silver top above 130; during that process, gold may accelerate—similar to what Goldman Sachs has suggested, with gold potentially pressing toward 5,400. In current gold futures options, substantial capital has already been positioned for strikes above 5,000.

$Gold - main 2602(GCmain)$ $E-Micro Gold - main 2602(MGCmain)$ $1-Ounce Gold - main 2602(1OZmain)$ $VanEck Gold Miners ETF(GDX)$ $iShares Silver Trust(SLV)$

Therefore, within this Q1 cycle, if there is no sudden hawkish pivot by the Fed or some other black-swan event that drives a sharp dollar surge, it is important to be cautious: the upside in gold and silver could exceed expectations.

From a strategy perspective, for silver futures, the approach remains to use the 5-day moving average as the observation line: if price breaks below the 5-day line, exit and take profit; if it breaks below the 10-day line, switch bearish and prepare to view it from the short side.If it does not break the 5-day line, stay bullish.

For gold, use the 10-day moving average as the bull/bear dividing line: if it breaks below the 10-day line, stop out long positions. Alternatively, if the Fed suddenly turns hawkish and the dollar index spikes, immediately take profit and reassess the bullish view on gold and silver

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- ZhongRenChun·01-23TOPyuan should peg to silver, instead of dollar.2Report