From the domestic macro point of view, it is still unsatisfactory at present, but the price decline has already priced in some negative factors in stages. Considering that the overall decline of other industrial metals has been very considerable, and many of them have fallen near the cost or reduced production, so the weak recovery may start to price towards the end of recovery, and the price will rebound.

1. Review of COMEX copper market last week

COMEX copper price fluctuated and rebounded last week, and the operating center of gravity moved up. The resolution of the debt ceiling problem has given the market some room to risk on, and risky assets have generally rebounded. The weaker economic data in Europe was priced in the previous price decline, while the economic data in the United States continued to perform well last week, and the recession feared by the market seems to be a long time away. This also gives the market the determination to rebound. On Friday, the number of non-farm payrolls in the United States exceeded expectations again, which made the market's expectations for the follow-up monetary policy change again. However, corresponding to the copper price, it is also worried that the follow-up maintenance of high interest rates and even further rate hike may make the aggregate demand still face a greater test and may cause some risk events again. Therefore, the copper price may rebound, but the height should not be too high.

In-depth analysis of macro, supply and demand and positions, and influencing factors of copper market

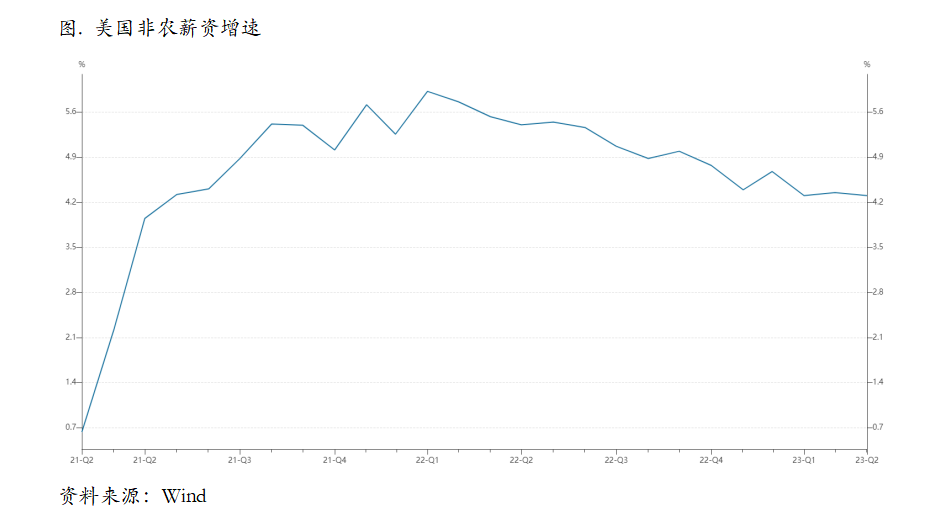

Macroscopically, the United States released the latest employment data for May. Among them, 339,000 new non-agricultural jobs were added, exceeding the market expectation of 195,000; The labor participation rate was 62.6%, and the average hourly wage increased by 4.3% year-on-year, slightly lower than the market expectation.

In May, 339,000 new non-agricultural jobs were created, which rose again compared with April, and exceeded market expectations. The new job market performed strongly. Structurally, service industry is still the main component of new employment at present. Generally speaking, the current Fed rate hike does not seem to have a significant negative impact on the service industry. However, with the high interest rate level getting longer and longer, the downward trend of related employment continues, but it is still far from the desirable level of the Fed.

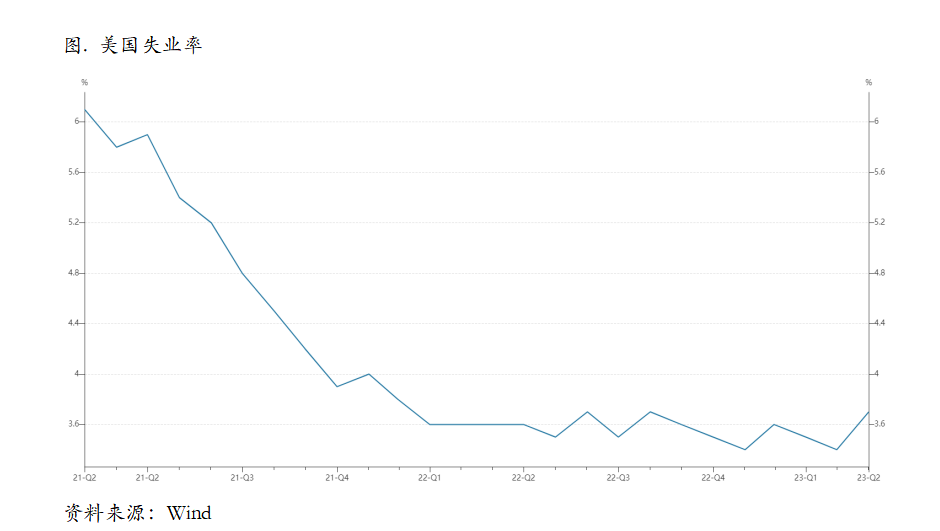

In terms of unemployment rate, the unemployment rate recorded 3.7% in May, up 0.3 percentage points from April, indicating that the current US labor market has cooled down. Specifically, the surveyed population increased by 175,000 in May, the labor force population increased by 130,000, and the labor participation rate recorded 62.6%, which was basically the same as that in April. However, the total employed population decreased by 310,000, and the unemployed population increased by 440,000, thus driving the unemployment rate to rise. We believe that under the background that the labor participation rate is difficult to increase again, the unemployment rate is rising, which may reflect that the current US labor market is already changing, and the subsequent cooling of the labor market may continue.

Judging from the current situation, the increase in unemployment rate in May reflects that the overall job market is still cooling down (the increase in the number of unemployed and the decrease in the total number of employed people), and the decline in the turnover rate is also a side evidence. If the unemployment rate continues to rise or remains high for a period of time, the inflection point of the American labor market may be coming soon. For the Federal Reserve, the employment data in May can be described as "mixed". From the current employment data alone, the probability of the Federal Reserve suspending the rate hike in June is high.

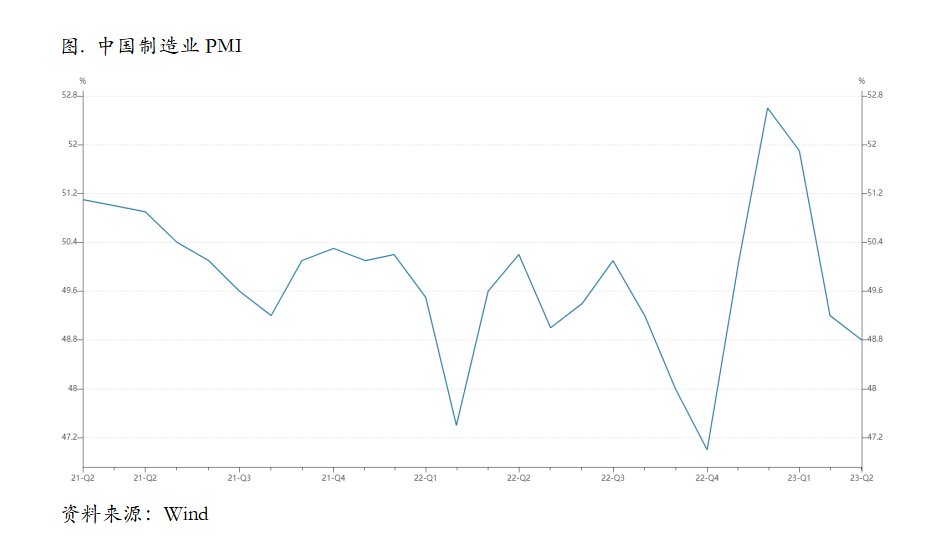

In terms of domestic macro, the official manufacturing PMI in May was 48.8%, the previous value was 49.2%, and it is expected to be 49.5%; In May, the official non-manufacturing PMI was 54.5%, the previous value was 56.4%, and the expected PMI was 56.4%. The Business Condition Index (BCI) of Chinese Enterprises is 55.0%, and the previous value is 58.8%.

Manufacturing PMI continued to weaken, and all items declined. The endogenous kinetic energy of the economy is still weak, and the PMI sub-items declined across the board in May. Structurally, both supply and demand are declining, while internal and external demand is weak, but domestic demand is declining even more. The manufacturing industry continued to go to the warehouse, and the price level dropped sharply. It is estimated that the PPI will drop to-4. 4% year-on-year in May. Weak domestic demand dragged down the prices of industrial products. In May, the purchase price and ex-factory price of PMI raw materials fell sharply, and the cost pressure in the middle and lower reaches was further eased. According to the high-frequency index, we expect that the PPI in May may be around-0. 8% month-on-month and around-4. 4% year-on-year.

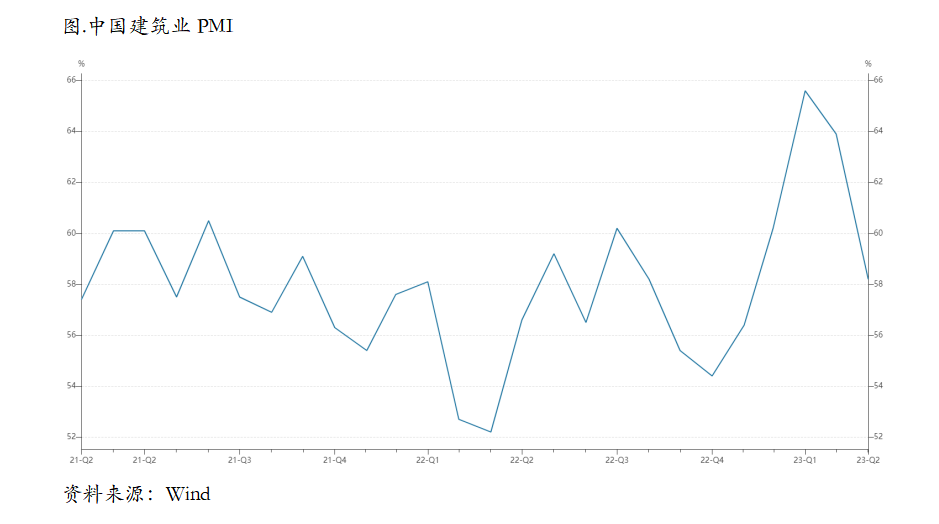

In May, the PMI of construction industry dropped sharply by 5.7 percentage points to 58.2%, and the new order index was lower than threshold for the first time in the year. On the capital side, the issuance scale of new local special bonds declined in April and May, which caused a certain drag on the growth rate of infrastructure construction. It is expected that a new batch of quotas will be issued as soon as the middle and late June. In addition, attention should be paid to the possibility of overweight policy financial instruments in subsequent national regular meetings. According to the comprehensive high-frequency construction, the growth rate of infrastructure construction will continue to decline in May, or fall to 9.0%.

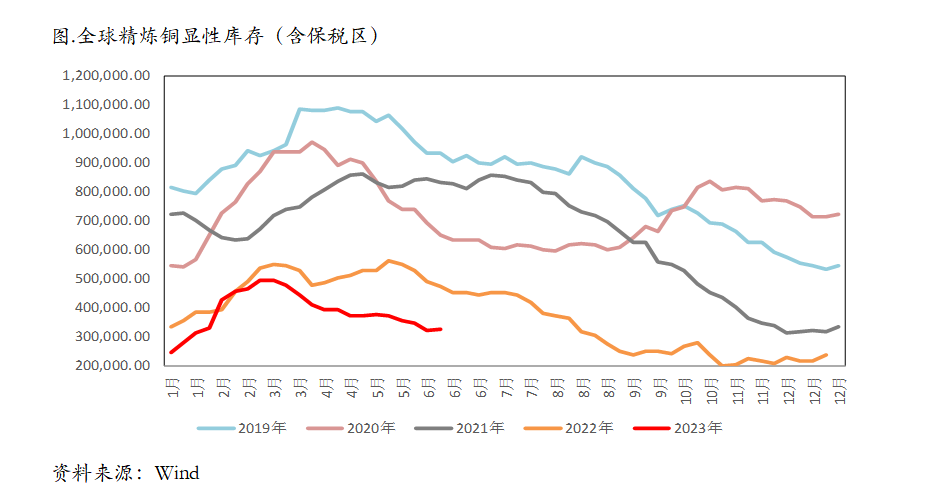

In terms of inventory, the spot inventory of electrolytic copper in the domestic market was 118,000 tons, down 5,300 tons from the 25th and up 2,900 tons from the 29th. This week, the spot inventory of electrolytic copper in Shanghai market stopped falling and rebounded, mainly because the week coincided with the end of the month, the pressure of some enterprises appeared, the downstream consumption performance was weak, and the inflow of imported goods supplemented the market. The spot inventory of electrolytic copper in Guangdong market continues to decline, and the main reason is that some refineries have less arrival. Although the downstream replenishment is not active, the inventory is lower due to less warehousing. This week, the spot inventory of electrolytic copper in the bonded areas of Shanghai and Guangdong totaled 112,500 tons, down 10,000 tons from the 25th and 5,000 tons from the 29th. The import window was still open during the week, and some imported goods were cleared and flowed in, and the inventory in the bonded areas also continued to decline.

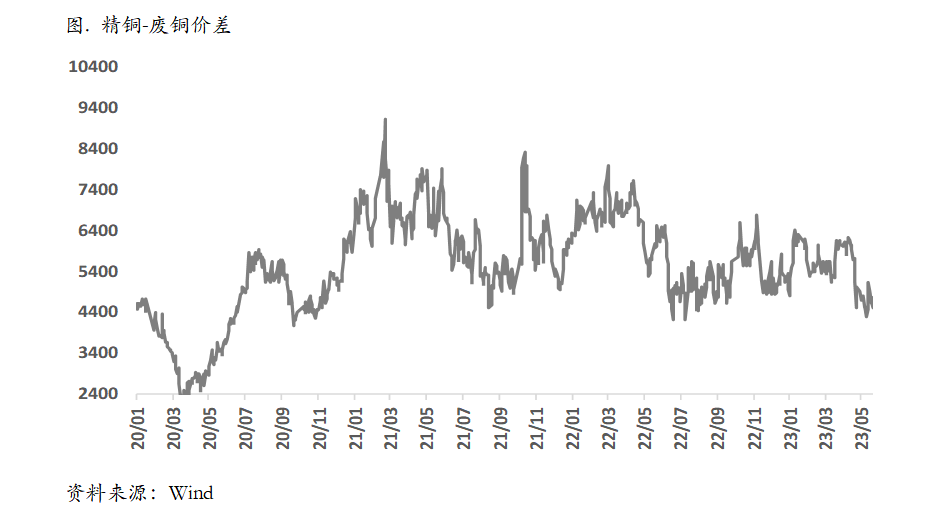

On the demand side, the processing fee of 8mm refined copper rod in domestic mainstream markets is generally raised due to the influence of high premium in the market, and the performance in East China is still the most obvious; The processing fee of refined copper rod market generally rises, and the transaction heat cools obviously; The price difference of refined waste rods has obviously expanded, and speculative transactions in the recycled copper rod market are hot; The price difference of refined scrap copper rods returned to the reasonable price difference level, and the trading activity of recycled copper rods increased significantly; In the market outlook, due to the insufficient orders and slow destocking speed of refined copper rod enterprises, under the background of high copper prices, it is expected that the finished product inventory of refined copper rod enterprises will still accumulate in the later period; However, due to the timely replenishment of raw materials in the market, the phenomenon of reducing production and stopping production last week did not spread widely. Although the overall supply of raw materials in the market is still tight, the speculative trading of short-term recycled copper rods is hot.

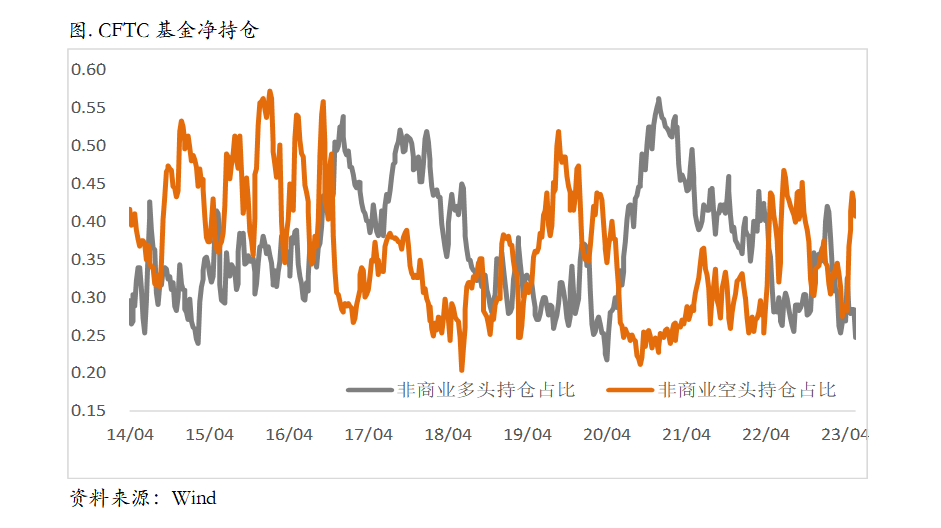

From the perspective of CFTC positions, the proportion of non-commercial long positions continued to decline last week, while the proportion of short positions increased more obviously. As far as we know, there are indeed some overseas funds that are closing their long positions, and the proportion of long positions may further decline.

Generally speaking, the price decline has already priced some negative factors in stages. Considering that the overall decline of other industrial metals has been very considerable, and many of them have fallen near the cost or reduced production, the weak recovery may start to price towards the end of recovery, and the price will rebound.

$E-mini Nasdaq 100 - main 2306(NQmain)$ $E-mini S&P 500 - main 2306(ESmain)$ $E-mini Dow Jones - main 2306(YMmain)$ $Gold - main 2308(GCmain)$ $Copper - main 2307(HGmain)$

Comments

Great ariticle, would you like to share it?