As the COMEX gold futures price edges closer to the $3,000/oz threshold, the current gold market demonstrates a price rally driven by strengthened technical patterns and underlying spot arbitrage dynamics. This momentum is further characterized by two prominent features. With market-wide concerns that Trump’s tariff policies might impose duties on physical gold imported into the U.S., this speculation could push gold prices towards a short squeeze above 3,000 points. Thus, this issue warrants a closer examination.

Two Unusual Features in the Gold Futures Market

1. Expanding Cross-Market Price Spread

The price spread between London spot gold and COMEX futures has widened to exceed 2.5 times the historical standard deviation. At present, this arbitrage creates a risk-free profit margin of over $40/oz for spot traders (see price spread chart). This reflects a severe imbalance in physical gold liquidity between the New York and London markets:

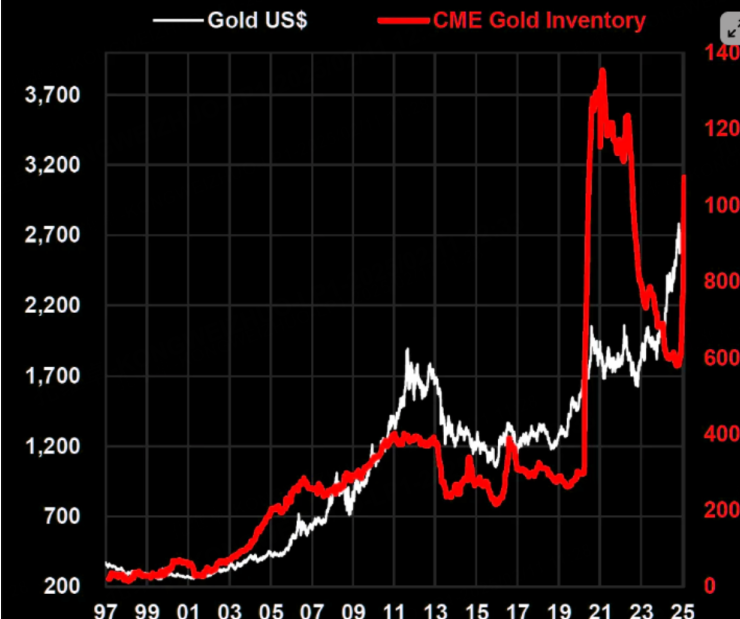

2. Inventory Disparities Between New York and London Amplify Arbitrage Activity

In the past month, COMEX gold warrant inventory in New York has grown by over 20%, while the proportion of “floating inventory” for deliverable gold bars in London has dropped to historic lows. This imbalance has led to a sharp rise in the cost of gold leasing in London, exacerbating the shortage of physical gold.

These features highlight how cross-market arbitrage mechanisms have become increasingly entrenched.

Cross-Market Arbitrage Mechanics Explained

Arbitrage Stages:

Spatial Arbitrage: Traders purchase 400-ounce standard gold bars (LBMA-certified) in London at the spot price and simultaneously sell equivalent COMEX futures contracts in New York. The gold is transported via sea freight to COMEX-designated warehouses for delivery.

Hedging for Price Risk:

To protect against price volatility during the shipping period (approximately 17 days), arbitrageurs establish short positions in futures equivalent to their spot holdings. According to CFTC data, hedge trades currently account for nearly 40% of COMEX’s open interest.

Profit Realization and Repetition: Upon completing physical delivery, arbitrage profits are calculated as:

(COMEXfuturesprice−Londonspotprice)−(shipping,insurance,andfinancingcosts).

This type of near-risk-free arbitrage opportunity is driving significant inflows of physical gold from London to COMEX delivery points each month.

This framework has contributed to a surge in the volume of gold delivered within the U.S.:

Structural Distortions in the Gold Market and the Potential Short Squeeze Above 3,000 Points。

This arbitrage mechanism is altering the fundamental dynamics of the gold market:

Bottlenecks in Refining and Delivery Chains:

The specification mismatch between London’s 400-ounce bars and COMEX’s 100-ounce requirement extends the logistics chain and inflates delivery demand. Refining capacity is further constrained, as the five largest global refiners currently have a backlog of 32 working days, creating a short-term supply bottleneck. This deepens the physical shortage.

Inventory Imbalances:

A significant portion of COMEX gold warrants has been locked in arbitrage strategies, while London’s “floating inventory” has shrunk to just 36 million ounces—sufficient for less than 10% of contracted delivery needs. According to the LBMA, delivery delays for 400-ounce bars have worsened, extending from the typical T+2 settlement to 4–8 weeks—a twelvefold decrease in efficiency.

Evidence of Forward Curve Distortions

COMEX gold futures are displaying widening premiums for near-term contracts (see Chart 1). For example, the April 2025 contract’s premium over the June 2025 contract has surged to $9.8/oz, marking the highest near-month premium since the 2008 financial crisis.

Speculation of a Gold Short Squeeze Triggered by Trump's Tariffs

The market is increasingly concerned about the prospect of Trump imposing tariffs on physical gold imports. This scenario would impact arbitrage activities in two possible ways:

Scenario 1: Tariffs Are Implemented

If the U.S. government imposes tariffs of 3.5%–5.2% on precious metal imports, the current arbitrage window would close permanently. Arbitrageurs would accelerate operations, triggering a “gold rush,” which exacerbates the short-term shortage of physical gold in both markets. Following the implementation of tariffs, COMEX short positions would face forced liquidation, likely resulting in a sharp price spike and a short squeeze.

However, after the short squeeze, the surplus of physical gold in COMEX warehouses would lead to inventory buildup, potentially causing a steep post-squeeze price decline.

Scenario 2: No Tariffs Are Implemented

If there are no tariffs, arbitrage activities would continue, but price spreads would likely contract to below $15/oz, returning to historical averages. Under this scenario, gold prices would maintain a gradual upward trend, with milder corrections compared to Scenario 1.

Historical Comparison of Gold Price Trends in Similar Situations:

The ongoing rally represents the gold market’s longest uninterrupted overbought stretch in history. Should Scenario 1 materialize, gold price volatility could surpass previous records. In the short term, however, the bullish momentum shows no signs of immediate reversal.

$E-mini Nasdaq 100 - main 2503(NQmain)$ $E-mini S&P 500 - main 2503(ESmain)$ $E-mini Dow Jones - main 2503(YMmain)$ $Gold - main 2504(GCmain)$ $WTI Crude Oil - main 2503(CLmain)$

Comments