Last Friday’s US-Russia talks failed to produce any “decisive” outcomes. The United States still requires coordination with the European Union and Ukraine for further discussions. Therefore, the Russia-Ukraine conflict is unlikely to end in the short term. However, the secondary sanctions on purchasing Russian crude oil are expected to ease somewhat. This outcome was largely anticipated by the market, so it did not cause significant surprise. Looking ahead to next week, the key focus will be whether there are confirmed plans for trilateral talks involving the US, Russia, and Ukraine.

Additionally, starting next Wednesday, the World Central Banks Annual Meeting will be held over three days. Market attention will center on the Federal Reserve Chairman’s speech at this event. Given Jerome Powell’s usual approach, it is widely expected that he will “douse” any aggressive easing expectations. Currently, the market assigns a 66% probability that the Fed will begin rate cuts in September, with 22% even expecting a 50 basis point cut. Hence, if Chairman Powell adopts a dovish tone, the market rally may continue.

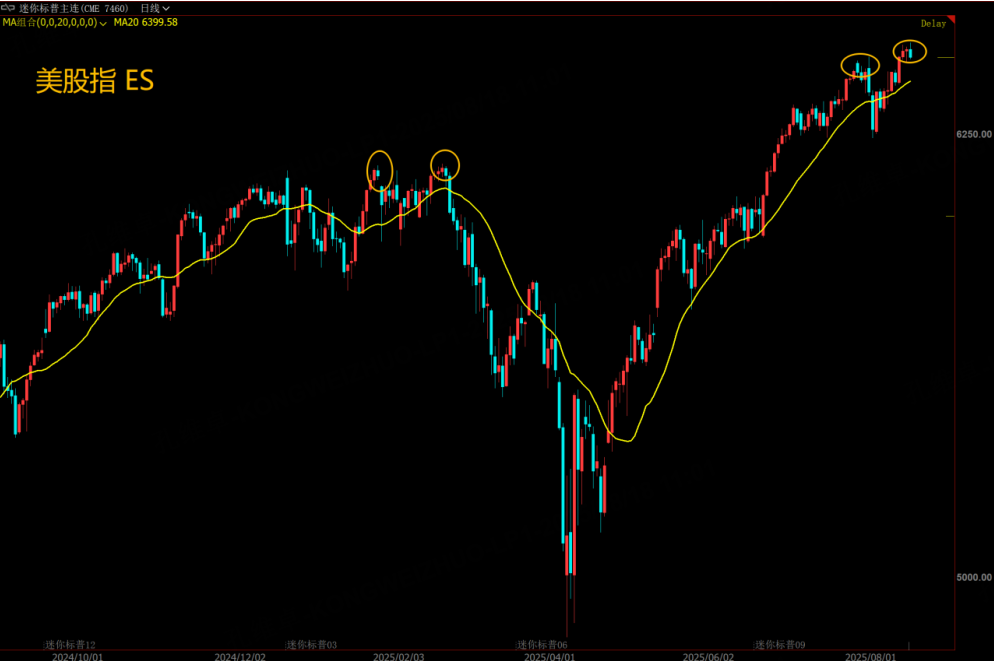

1. Will US stock indexes be affected?

If Powell delivers hawkish remarks, US stock indexes will definitely be impacted, especially based on his assessment of inflation, which directly affects market expectations for rate cuts. Should the major US indexes adjust, observe closely the speed of their correction, since US indexes often form double-top patterns. The 20-day moving average remains a key short-term risk management level for the indexes, which suggests caution is still required. The risk window for US stocks in August has not yet closed.

From a technical perspective, if the major US stock indexes do not fall below the 20-day moving average and instead continue to make new highs, the double-top pattern would fail. In that case, there is nothing extraordinary to note going forward, and the 20-day moving average can continue to serve as a tracking indicator for the indexes.

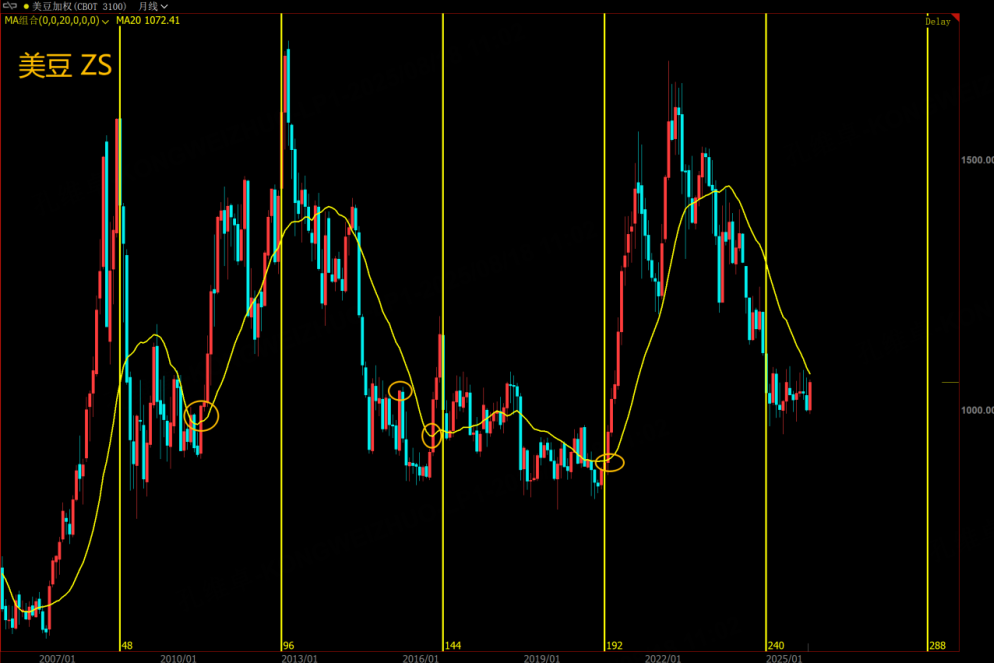

2. Significant drop in US soybean inventory—watch if it breaks out

Last week, the agricultural sector saw an important monthly supply and demand report, with soybeans standing out as the most favorable crop. The USDA lowered the global soybean production forecast. Compared to the July report, the August update reduced soybean output primarily due to decreased harvested area in the US and lower yields in the EU and Serbia. Specifically, global soybean production for the 2025/2026 marketing year is revised down by 1.29 million tons to 426 million tons. Correspondingly, global soybean ending stocks were cut by 1.17 million tons to 125 million tons.

On the surface, these figures are not dramatically surprising. However, because production data in previous months had been overly optimistic and soybean prices hovered near the cost level of 950 cents per bushel, this output reduction delivers a long-awaited positive signal for the market. Yet, since this production decline is not caused by weather issues and its sustainability is questionable, we cannot yet conclude that soybean prices have entered a significant new uptrend. The key observation is whether soybean prices can break through the 1100 cent mark. Failure to do so would mean continued volatility.

Technically, the 20-month moving average remains a ceiling constraining soybean prices. A breakthrough above that level would open the door to a promising market, while failure might result in range-bound price action or even slightly lower prices. From a subjective standpoint, I lean towards soybean prices not hitting new lows; although new lows cannot be completely ruled out, the prospect of renewed, large-scale soybean purchases by China following a potential Sino-US trade agreement represents a major bullish fundamental factor. Hence, do not dismiss the potential for a soybean market rally simply due to short-term volatility. Patience is warranted.

$E-mini Nasdaq 100 - main 2509(NQmain)$ $E-mini S&P 500 - main 2509(ESmain)$ $E-mini Dow Jones - main 2509(YMmain)$ $Gold - main 2512(GCmain)$ $WTI Crude Oil - main 2510(CLmain)$

Comments