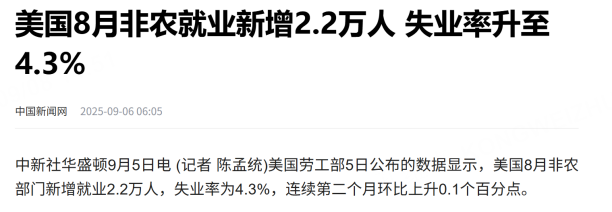

The latest nonfarm payroll report, released last Friday ahead of the Federal Reserve’s September meeting, mirrored the prior month’s disappointing data, significantly missing market expectations and accompanied by downward revisions of previous figures. This reinforced market anticipation that the Fed would begin cutting rates in September, with CME and Bloomberg markets pricing in three 25bps rate cuts this year. Historically, the Fed has refrained from easing because of a robust U.S. economy, implying no urgent need for rate adjustments. However, the sharp downward revision in nonfarm employment raises the probability of rate cuts while simultaneously reviving fears of an economic recession in the U.S. that had been looming for two years. This dual effect led to a bifurcated market response: gold rallied while U.S. stock indices corrected. Clearly, recession concerns weigh more heavily on the stock market than the prospect of rate cuts.

Early Attention to U.S. Stock Market Recession Expectations

Economic weakness usually prompts Fed rate cuts to stimulate growth, a standard cycle. Although no direct signals currently indicate a U.S. recession, the historical pattern of an inverted yield curve (where long-term bond yields fall below short-term yields) generally precedes recessions within three years. This pattern appeared a year ago but the expected recession has yet to materialize. The critical question remains whether this economic rule will break or if a recession is simply delayed. This uncertainty calls for vigilance. If a recession is indeed beginning, U.S. stock indices would likely experience more volatility, not necessarily crashing immediately but shaking for some time until the market reaches a consensus.

From a technical perspective, the S&P 500 still trades near its 20-day moving average, while the Russell 2000 index outperforms the other three major indices. Such divergence increases the risk of a market correction. Therefore, consistent with the prior week’s analysis, the recommended strategy is to buy the VIX, purchase put options for protection, and wait patiently for clearer market direction.

Watch for a Turning Point in Gold Prices

Based on the cyclical timing of gold prices, a turning point is anticipated around the release of the nonfarm payroll data. Since no turning point appeared before the data release, this week demands close attention. Under normal circumstances and barring significant negative news, gold’s cyclical adjustment magnitude typically ranges from 150 to 200 points. Considering last week’s high near 3650 (October COMEX Gold futures), the key support area would likely be near the 3450-3500 range, close to the breakout zone. If unexpected negative news emerges, the adjustment could be larger but currently, nothing significant has surfaced. Hence, the market should initially observe the normal adjustment range.

From a long-term perspective, the 20-week moving average remains a reliable indicator to distinguish bullish or bearish phases. Therefore, this expected cyclical turn should be viewed as a temporary adjustment, and after a sufficient decline, gold could present a reasonable minor entry opportunity.

$NQ100指数主连 2509(NQmain)$ $SP500指数主连 2509(ESmain)$ $道琼斯指数主连 2509(YMmain)$ $黄金主连 2512(GCmain)$ $WTI原油主连 2510(CLmain)$

Comments