Many people may not yet have noticed that the current market is showing a very intriguing and seemingly contradictory pattern.

On one hand, bond market pricing suggests that investors do not believe the Federal Reserve, even after its leadership change, can smoothly and quickly transition into a clearly dovish policy environment. On the other hand, silver prices have hit fresh highs even without any visible squeeze caused by tightness in the physical inventory. The gold–silver ratio has undergone a technical collapse, which implies that market bets on future inflation remain elevated, and silver is very likely front-running a new upcycle in broader commodities.

In Chinese physical silver market, the basis has continued to weaken, yet U.S. silver prices are still being relentlessly squeezed higher.

This contradictory development gives the upcoming speech by Jerome Powell an even wider range of potential market volatility scenarios. Counting carefully, Powell still has three FOMC meetings to chair before stepping down, and the tone he adopts in those three meetings will determine the trend for major assets such as equity indices and gold and silver.

The Fed Is Unlikely to Turn Fully Dovish, and the Bond Market Does Not Believe

Judging from current market positioning and existing macro data, it will be very difficult for the Federal Reserve to pivot abruptly from a cautious, hawkish stance toward the deeper, more aggressive rate-cutting path advocated by the “shadow Fed chairman,” Kevin Hassett.

First, there are no clear signs of an imminent macroeconomic recession. The U.S. Department of Labor’s October Job Openings and Labor Turnover Survey (JOLTS) showed that job openings were unexpectedly strong, with vacancies surging by 431,000 positions month on month, indicating that labor demand remains robust.

As of October, job openings exceeded the number of unemployed persons by 55,000. This means that the long-standing situation in which job openings were fewer than the unemployed has once again been reversed. It is worth noting that the U.S. economy has never fallen into recession when job openings have exceeded the number of unemployed workers.

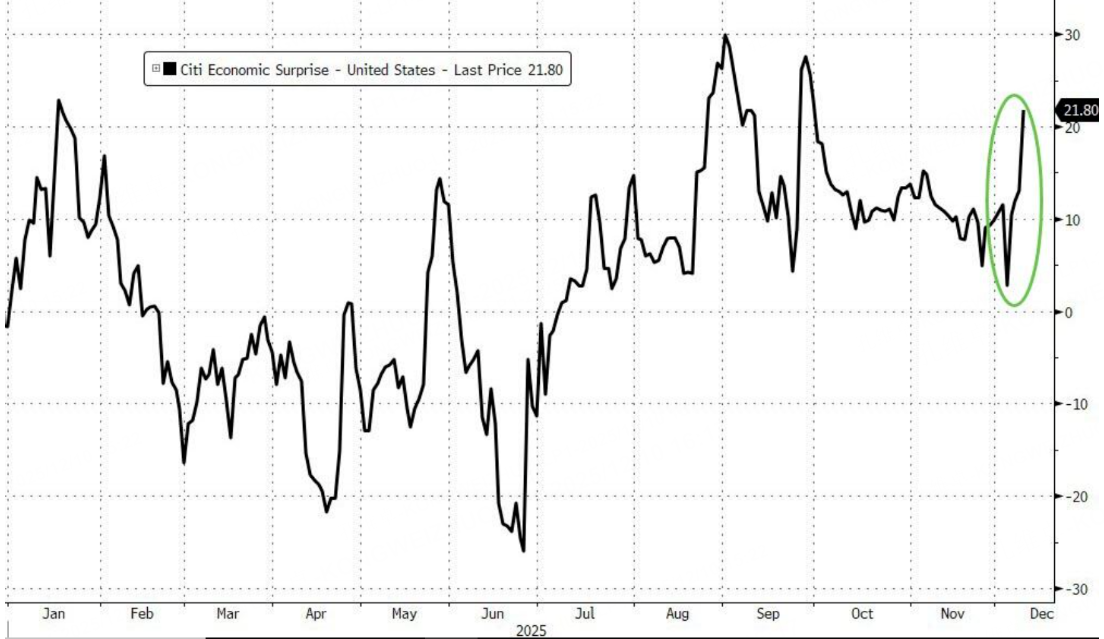

Therefore, there is not enough data-based justification for the Fed to embark on an aggressive, deep rate-cutting path. In addition, Citigroup’s Economic Surprise Index has continued to climb, reaching 21.80, underscoring the ongoing strength of the economy

From within the Federal Reserve itself, the internal personnel landscape also constrains the possibility of a comprehensive shift to an easy policy stance.

At present, the most hawkish Fed officials are Powell, Cook, and Barr. Even in the most dovish scenario in which these three hawks all depart alongside Powell, it will still be very difficult for the incoming chair, Hassett, to coordinate the remaining officials into a fully dovish consensus.

At the moment, officials such as Williams, Jefferson, Bowman, Waller, Milan, Hammack, and Logan all have strong credibility and a high degree of independence, making them unlikely to change their positions purely because of political pressure.

Even after excluding a few officials who have previously voiced dovish views, Bowman and Waller still do not exhibit an obvious dovish inclination, and the probability that they would shift in that direction is close to zero. For these remaining officials, it is also very unlikely that they would lower the projected rate-cut path for 2026 in the upcoming dot plot. If Cook and Barr were to remain at the Fed, the new chair would have even fewer resources with which to implement a dovish rate-cutting agenda.

The first two FOMC meetings in 2026 will still be chaired by the distinctly hawkish Powell, and Hassett may only begin to exert real influence on the meeting outcomes from May onward. In the near term, this makes the December FOMC meeting highly likely to deliver what can be described as a “hawkish rate cut.”

A hawkish rate cut means that while the policy rate is indeed cut by another 25 basis points, Powell will deliver hawkish messaging in the subsequent press conference.

He may not even mention the market’s anticipated RMPs plan, which is a Treasury bill purchase program of 4.5 billion dollars per month as currently discussed. If the meeting results in such a hawkish rate cut, markets will inevitably be jolted in the short term, forcing a reversal of pricing that has become overly dovish. In that scenario, gold, silver, and equity indices may all face a period of correction.

Finally, it is important to recognize that next year the pressure of global liquidity tightening is likely to re-emerge, and, judging from the bond market, investors have not priced in much of an extended, dovish, low-interest-rate environment driven by rate cuts.

At present, what appears relatively certain is that the European Central Bank, the Reserve Bank of Australia, the Riksbank, the Reserve Bank of New Zealand, the Bank of Canada, and the Swiss National Bank have probably already ended their easing cycles. Among major central banks, only the Federal Reserve, the Bank of England, and Norges Bank are likely to continue cutting rates into 2026.

Next week, the Bank of Japan is also very likely to raise rates, thereby tightening one of the key channels for exporting cheap capital and making global excess liquidity even more scarce. Even if the Fed delivers a dovish rate cut this time, long-dated U.S. Treasury yields may not decline over the long run. That is because rate cuts can trigger a retaliatory rebound in inflation, which weakens the attractiveness of U.S. Treasuries and further reduces the supply of buyers.

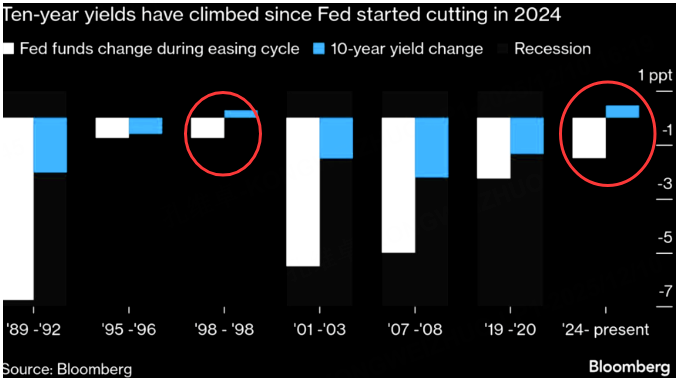

It is crucial to note that among past Fed easing cycles, the one that has played out since 2024 is highly unusual over the last 30 years. Even though the Fed has continued to cut rates, on an annual basis U.S. Treasury yields have actually risen.

Consider what is happening now: despite the Fed continuing to cut rates and even preparing to change chairs in order to pursue an even more dovish rate-cutting policy, prices of 10-year Treasuries have fallen instead of rising, and yields have broken to new highs. This is exactly the underlying logic just described.

Powell’s Remarks Will Determine Short-Term Market Direction

Looking ahead to the meeting early Thursday morning, Powell’s remarks and the subsequent dot plot will be the central focus for markets. His comments will set the basic tone for the next two FOMC meetings. If his message leans dovish, inflation expectations will intensify, and in the short term, equity indices and gold and silver prices are likely to continue moving higher.

If, instead, Powell’s remarks lean hawkish, that would align more closely with current bond market expectations, and market reactions would likely be less extreme. In that scenario, there could be modest pullbacks in equity indices and in gold and silver, but such pullbacks should be viewed as opportunities to build long positions.

In addition, there is another curious development in the market that deserves caution:

the collapse of the gold–silver ratio has already sent an important signal.

At present, after a brief pullback, silver has once again broken above its prior highs, creating a technical inflection point that is well worth watching. This is the market challenging and reminding us to reconsider the logic underlying our traditional understanding.

Previously, an internal report from JPMorgan suggested that the appropriate level for the gold–silver ratio should be around 75, which is near its lows over the past decade. That level has now been decisively broken, meaning that silver’s recent performance has been far stronger than most people expected.

If the gold–silver ratio continues to collapse, silver may find itself in a persistent short-squeeze environment. Based on estimates from the monthly chart, there could still be more than 30 percentage points of upside, and a price level of 70 dollars per ounce is not out of reach.

However, if in the short term the gold–silver ratio rebounds and returns to a state where 75 again acts as its central anchor, silver could experience a major correction. In the near term, it is enough to use silver’s 5-day moving average as the key reference level. As long as silver does not break below the 5-day moving average, the strong, short-squeeze-like uptrend is unlikely to be over.

The collapse of the gold–silver ratio seems to indicate that capital is already moving in advance to bet on a scenario of stagflation or at least a rebound in inflation. In such a scenario, yields remain at high levels while commodity prices broadly move higher, which is a classic stagflationary pattern.

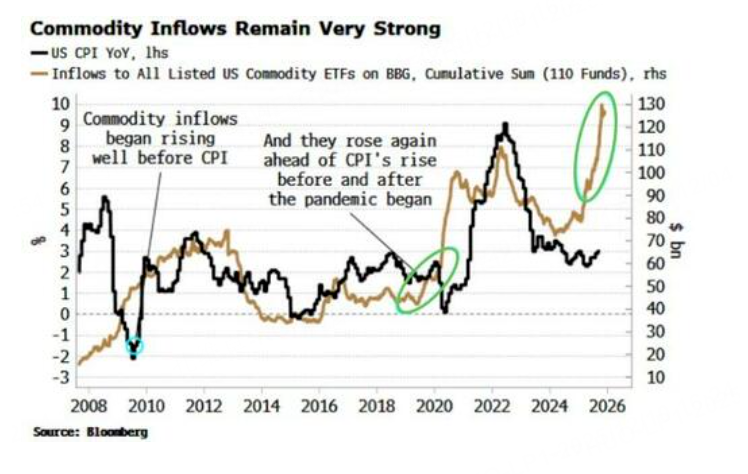

From the perspective of institutional flows into commodity-related ETFs, there has been a visible increase in capital inflows into these products over the past several months. A new wave of reflation may therefore be only a matter of time.

The anchor that could trigger this wave lies in whether, tomorrow night, Powell uses a dovish tone that effectively fires the starting gun for a repricing of commodity markets.

How to Position for Market Opportunities Before the FOMC Meeting

Because silver is so volatile, the previous strategy of going long the gold–silver ratio with a 5-day moving-average take-profit level, although very precise in the short term, was still extremely risky. Silver has already accelerated higher three times from its recent lows, and without a suitably strong positive catalyst, the short-term risks are very significant. For this reason, it makes sense here to use gold as the underlying asset when constructing a straddle-style options strategy.

One can simultaneously buy gold put and call options with the same strike price and the same expiration date, choosing at-the-money options. The goal is to bet on an increase in short-term volatility for gold. After Powell’s remarks are released, depending on whether his tone turns out to be dovish or hawkish, the losing leg of the options position can be closed, and the position can then be fully exited for a short-term profit within this week.

Because this is a buy-side strategy, both the potential loss and the risk exposure are fixed and clearly limited. The trade is simply a bet that Powell will deliver comments that surprise the market, thereby triggering a rise in short-term market volatility.

$E-mini S&P 500 - main 2512(ESmain)$ $E-mini Dow Jones - main 2512(YMmain)$ $Gold - main 2602(GCmain)$ $WTI Crude Oil - main 2601(CLmain)$ $E-mini Nasdaq 100 - main 2512(NQmain)$

Comments