The global market may face the baptism of a perfect storm.

In the US financial market, the headwind of interest rate is blowing stronger, and the major economies in Europe and Asia have also raised their future interest rate expectations.

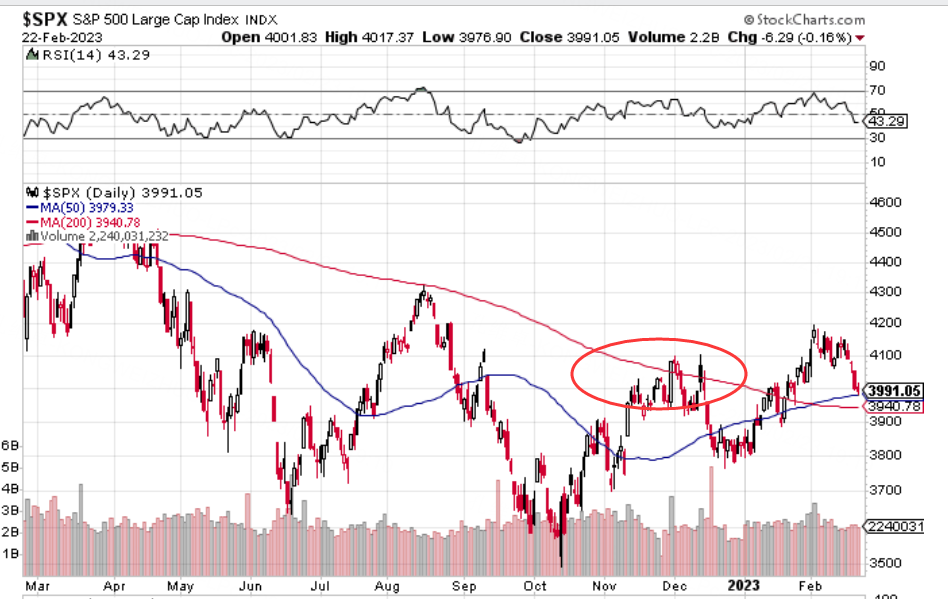

The global bond market is falling, the yield is rising, the revaluation of US stocks will be on the verge, and the S&P index has already shown signs of head shape.Breaking all this deadlock may be the completly falling below the 200-day moving average.

Big risks mean big opportunities. Under the expectation that foreign capital will start to return to the US dollar again, there will be a low buying opportunity in global stock markets. For example, Chinese real estate stocks that have been suppressed for a long time may be more turbulent,

It's time for trading in spring. The last rise of the US dollar and the last fall of the market before the recession may appear at any time:

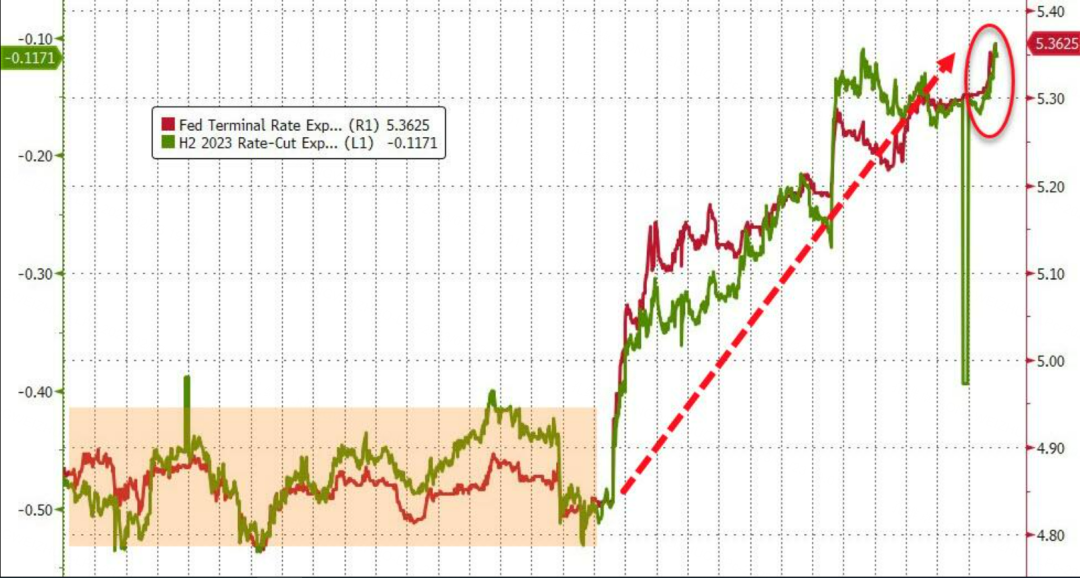

The minutes of the latest interest rate meeting of the Federal Reserve were released, and there was no accident. The hawkish atmosphere in line with expectations pushed the interest rate peak of the Federal Reserve's future interest rate hike slightly higher again:

At present, the expectation of the peak of interest rate increase in derivatives market has pushed up to more than 5.3%, and the possibility of interest rate cut this year is almost zero.

It is worth noting that the current financial environment index is inconsistent with the trend of the Fed interest rate curve:

In the week before and after the minutes were issued, the index rose slightly. According to the Fed's point of view, the tightening trend of the financial environment index may continue until it is consistent with the interest rate corridor, which may mean that there will be more hawkish actions in the future and the market liquidity will be further tightened.

We should pay attention to the fact that the hawkish headwinds in the interest rate market have become stronger and stronger, and the biggest problem caused by this is the high rise of US bond yields, which will soon exceed the important point of 4% in 10 years.

The 10-year US bond yield is usually used as the pricing reference value of the risk-free yield, Its rise, It means that the market puts forward higher requirements for the risk compensation of the stock market,

It directly lowers the overall valuation of US stocks, and the indirect market performance is that a large amount of funds will return to the bond market, which will suppress the stock price. We should know that the increase in yield has depressed the bond price, and the current US bond price is quite attractive under the background of approaching recession and imminent stock market correction.

The same situation happened in October last year. After the 10-year US bond yield exceeded 4% in a short time {above}, S&P started the fluctuation at the top for nearly three months, and vomited back a lot of gains in December.

However, unlike last time, now the 10-year yield broke 4%, which is not the end, but the beginning. The rise may even last for half a year, so the correction faced by US stocks is likely to be more violent

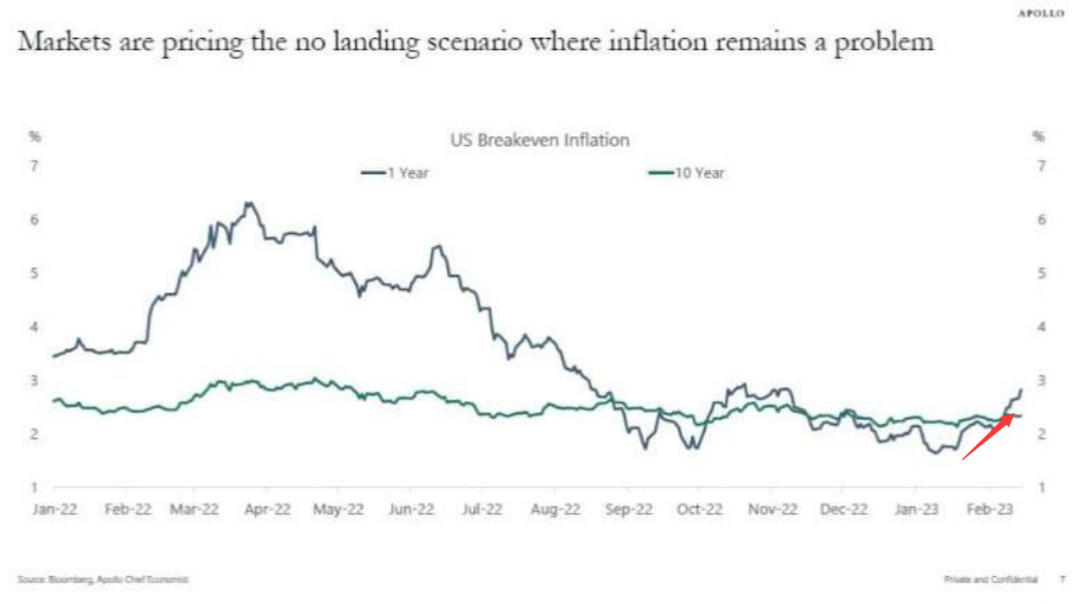

Inflation expectations are rising again

As we all know, the frequency of recent macroeconomic data exceeding expectations in the United States is very high, which led to a sharp rise in the economic accident index after the Federal Reserve meeting in January, but it also raised inflation expectations

The US Breakeven Inflation rate also reacted, and the 2-year Breakeven inflation rate began to bottom out and rise

These are very ominous omens, which mean that the Fed's interest rate hike work is not in place, and also indicate that a more violent interest rate hike storm will appear in the future.

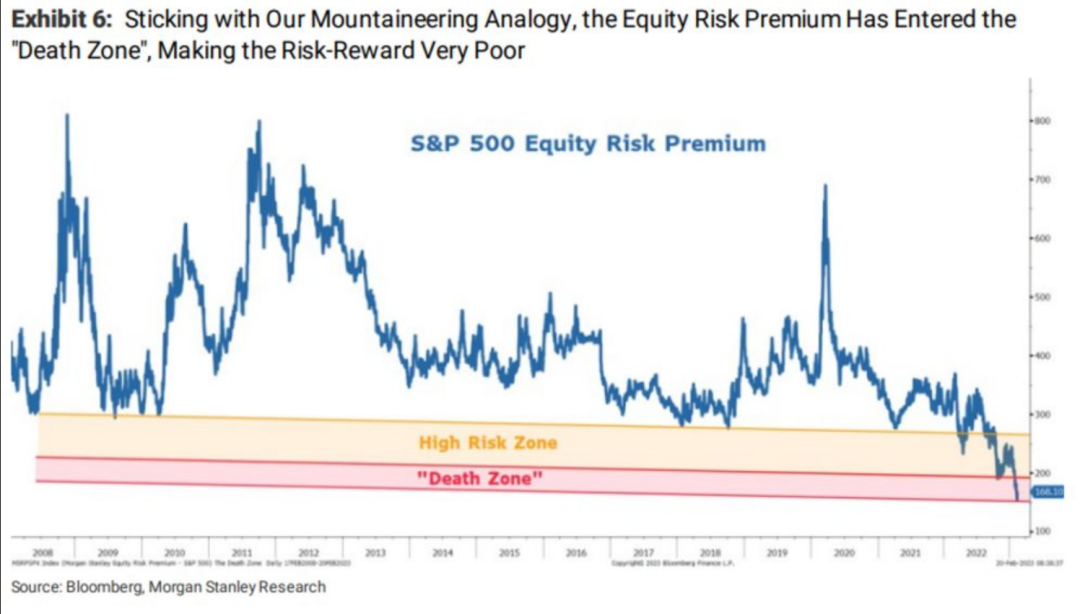

And how many times can the stock market afford to raise interest rates?

Let's look at this statistic:

According to Morgan Stanley's statistics, the trend of S&P's risk premium index since 2008, as we talked about above, because the risk-free interest rate rises and the risk premium squeezing the stock market falls, the risk premium of S&P has now come to the dead zone.

U.S. stocks have a high probability, so it is difficult to keep rising. That is to say, if you sell the call option of S&P on a weekly basis at this time, it may be a good choice.

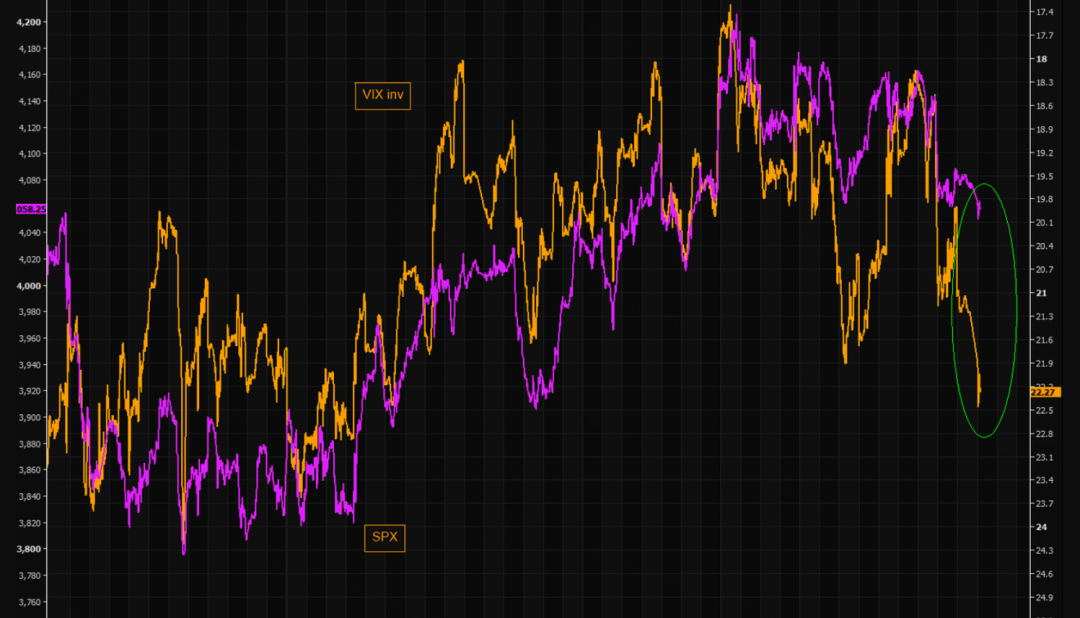

You should be careful of the gap as following

One is the gap between the market volatility index and the S&P's continued high volatility

The way to close the gap is likely to be a shock caused by the sharp drop of S&P, which makes the red (SPX) and yellow (VIx) intersect again

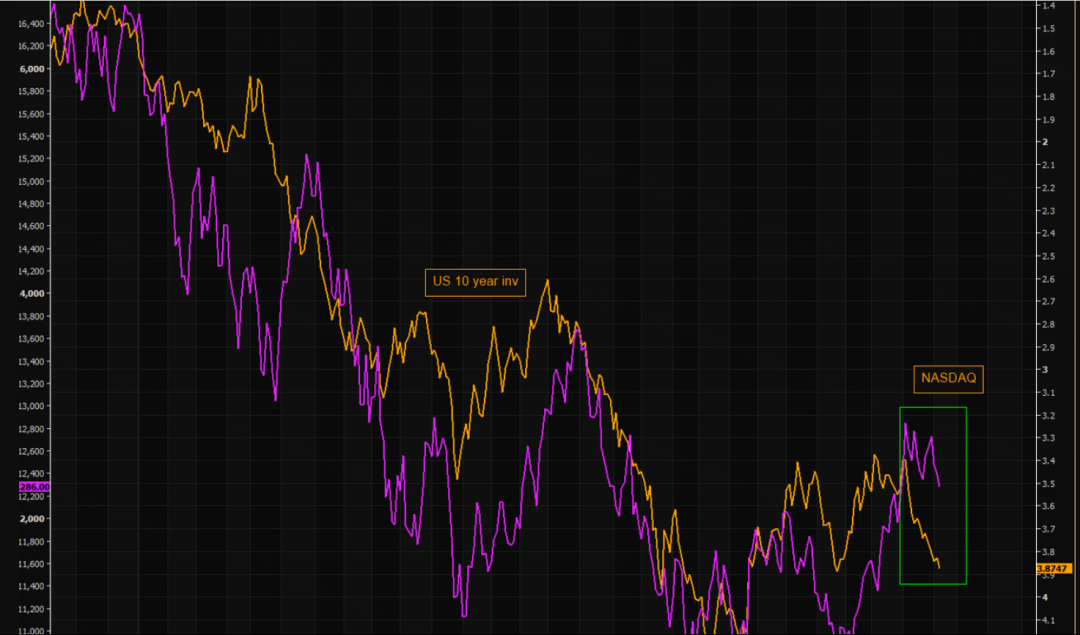

The other is the gap between Nasdaq and 10-year US bond yields.

This gap has widened, and the squeeze on high-valued stocks brought about by the rise in yields will bear the brunt of the Nasdaq, so if you choose to short, the Nasdaq is of course the first choice

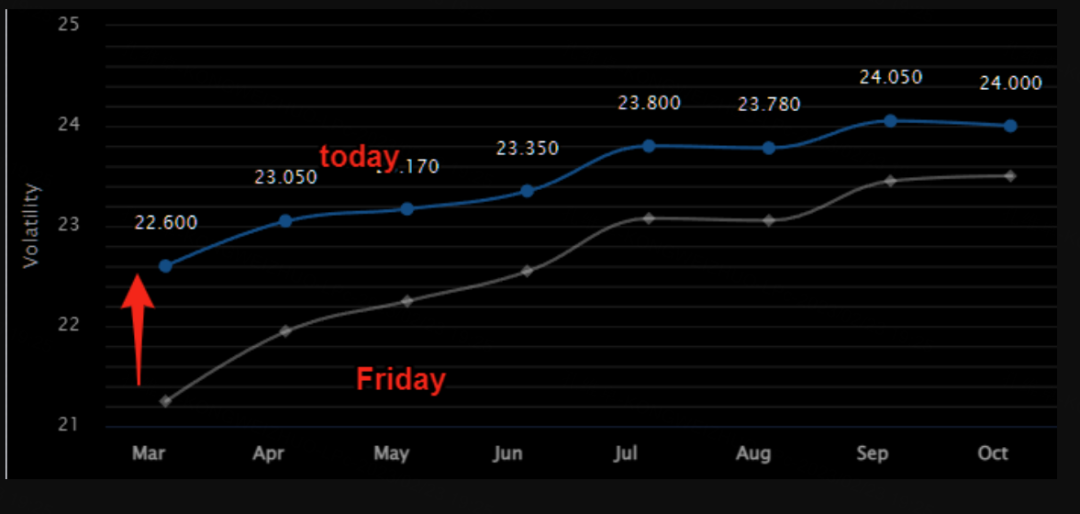

With the further pricing in of future hawks, the price structure of VIX index futures is also rising across the board, and a fluctuation will be triggered in the near future

What do you say about this ?leave me a message?

$E-mini Nasdaq 100 - main 2303(NQmain)$ $E-mini Dow Jones - main 2303(YMmain)$ $E-mini S&P 500 - main 2303(ESmain)$ $Gold - main 2304(GCmain)$ $Light Crude Oil - main 2304(CLmain)$

Comments