-Global investors are still stumbling forward, and bearish sentiment pervades the market.

Bad news came one after another, causing a new round of selling in the global market:

1) The global inflation data is higher, and the inflation data released by Canada and the United Kingdom are stronger than expected (the inflation rate in the United Kingdom has returned to double digits, reaching 10.1%);

2) Fed officials hawkish speech, Minneapolis Fed Chairman Kashkari said that core inflation has not peaked (adding fuel to the fire); St. Louis Fed Chairman Brad said that the Fed should not respond to the stock market decline;

3) The number of new housing starts in the United States has not yet bottomed out, and it has dropped by 20.3% compared with the recent peak hit in April;

4) Fed Beige Book shows inflation remains high, with 13 references to "recession".

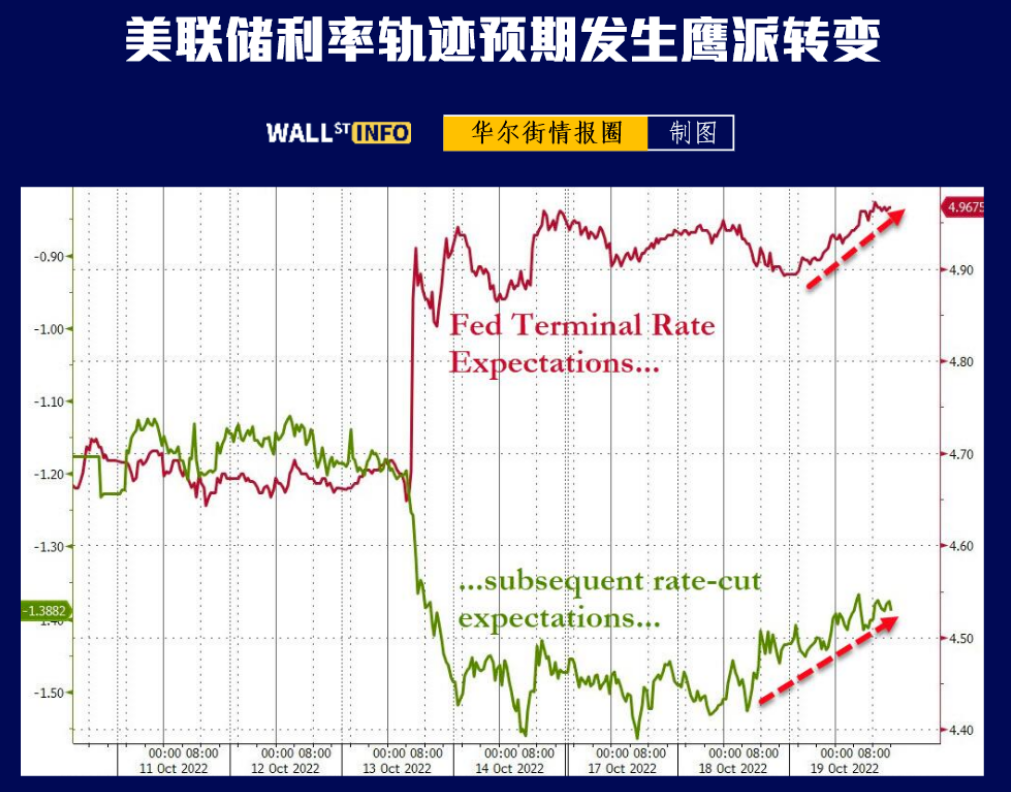

For the market, the third of the above four bad news is "good news", because "the bad news of economic data may cut interest rates and the Fed's expectation of raising interest rates". But last night, the data only played a short-term role. The market's expectation of the Fed's interest rate trajectory has undergone a hawkish change, and the expectation of the end rate has reached a high point of about 4.977%.

The market is currently pricing the probability of raising interest rates by 75 basis points in November is 91%, the probability of raising interest rates by 100 basis points is 12%, and the probability of raising interest rates by 75 basis points in December is 75%.

Affected by the above news, the global selling tide surged:

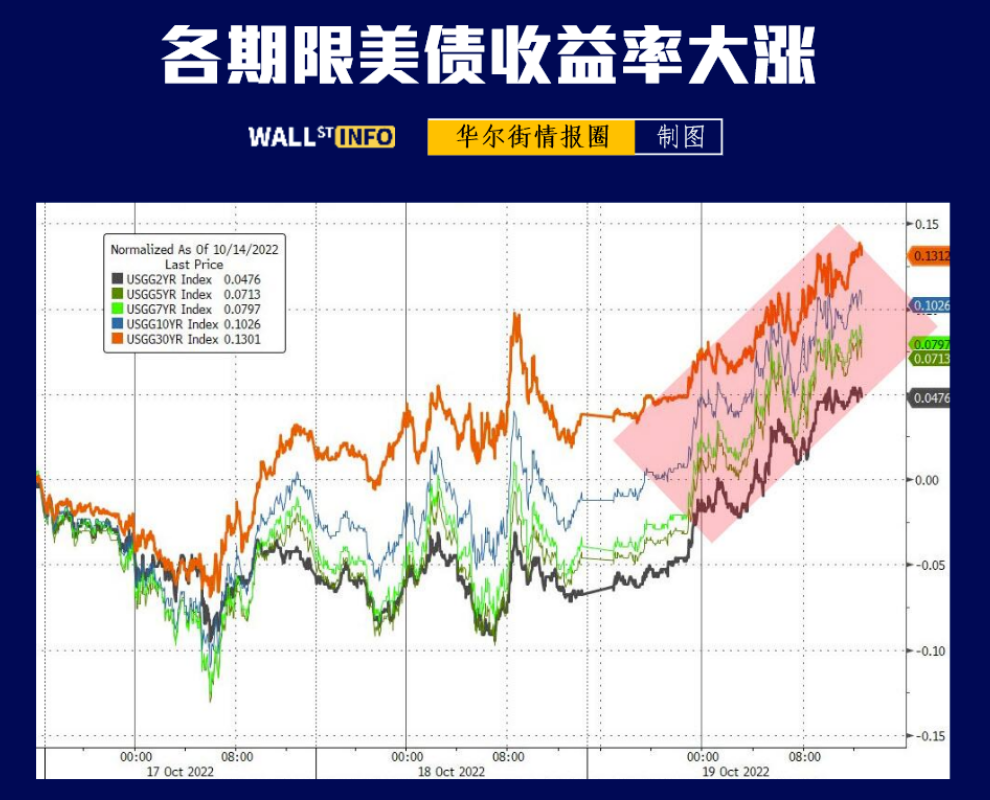

-The US Treasury bond market was the epicenter yesterday, and the yield of 10-year US bonds rose by 12.7 basis points to 4.13%, the highest since June 2008. Yields on policy-sensitive 2-year US bonds rose 12 basis points to 4.55%, the highest level since August 2007. Traders are concerned about whether the yield will effectively exceed 4.1%, and if it does, it may test the 2008 high near 4.25%.

-The US dollar rebounded from a two-week low as US bond yields rose.

-The yen fell to the key mark of 150, and traders paid close attention to the possibility of intervention by the Bank of Japan. Don't be surprised if the Bank of Japan intervenes again in the coming days, not to reverse the trend, but only to introduce some two-way volatility.

-Offshore RMB fell more than 400 points, hitting the lowest point since trading started in August 2010. For Asian currencies, RMB has always been an early warning signal.

-Gold prices fell by more than 1%, and the strong US dollar and soaring US bond yields put pressure on gold prices.

-US stocks reversed Tuesday's gains and the decline was controlled within 1%. The S&P 500 index fell 0.7% to 3,695.16 points; The Nasdaq fell 0.9% to 10,680.51 points; The Dow Jones index fell 0.3% to 30,423.81. Such a decline seems to be what the Fed wants most.

The market reaction largely reflects investors' expectations of how short-term interest rates will change before the maturity date.

Now, the only consolation is that the market hype about economic recession is "beginning to take shape". The atmosphere has set off here. If we don't hype the economic recession, the crisis will never end.

Two major news agencies around the world have released surveys on the economic recession:

According to the model data established by its economists released by Bloomberg News, the probability of recession in the US economy in the next 12 months reaches 100%, which is much higher than the previous value of 65%.

In the latest Wall Street Journal survey, more than 70 economists predicted that the probability of a recession in the US economy within one year was 63%, up from 49% in July.

Bill Holt, a financial writer, said, I think it is ridiculous for people to speculate about whether they will fall into recession, because it is obvious-we are already in recession. The game is over, and they (the Fed) are unplugging.

$E-mini Nasdaq 100 - main 2212(NQmain)$ $E-mini Dow Jones - main 2212(YMmain)$ $E-mini S&P 500 - main 2212(ESmain)$ $Gold - main 2212(GCmain)$ $Light Crude Oil - main 2212(CLmain)$

Comments