During Thursday evening's live session, I emphasized that February represents a pivotal time window for U.S. stock indices.

Unlike other periods, this month often dictates the market's trajectory for the entire year. As if on cue, U.S. stock indices experienced a decline on Friday, marking another "Black Friday." While the drop was not severe, its implications should not be underestimated. I advise caution in managing your U.S. stock index positions to guard against potential volatility. For a more detailed analysis of this critical period and corresponding strategies, join me in this Thursday's 8 PM live session.

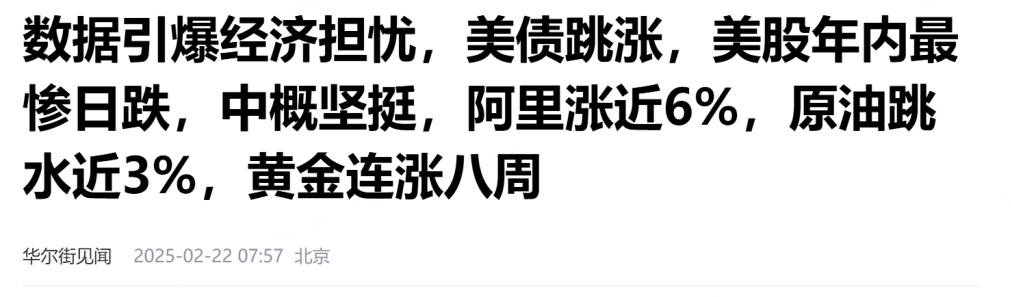

Economic Data Sparks Concerns: U.S. Bonds Surge, Stocks Plunge

On February 21, 2025, Wall Street witnessed one of the worst trading days of the year for U.S. stocks. Despite varying interpretations of Friday's downturn, it ultimately boils down to weak economic data and the Federal Reserve's cautious approach to rate cuts. This decline warrants heightened vigilance—further losses could escalate significantly.

From a technical perspective, U.S. stock indices remain above their 20-week moving average but are at risk of breaking below it next week. If confirmed, this would mark the end of the upward trend that began in October 2023 and signal the onset of a turbulent phase for U.S. stocks.

Historically, significant trend breaks in U.S. indices are often accompanied by short-term accelerated declines. Investors should prepare hedging strategies or wait for the market to bottom out before re-entering.

Additionally, February's high point is a key level to monitor this year. Without substantial monetary easing, breaking through this resistance will be challenging.

Shifting Opportunities: The Asia-Pacific Market Takes Center Stage

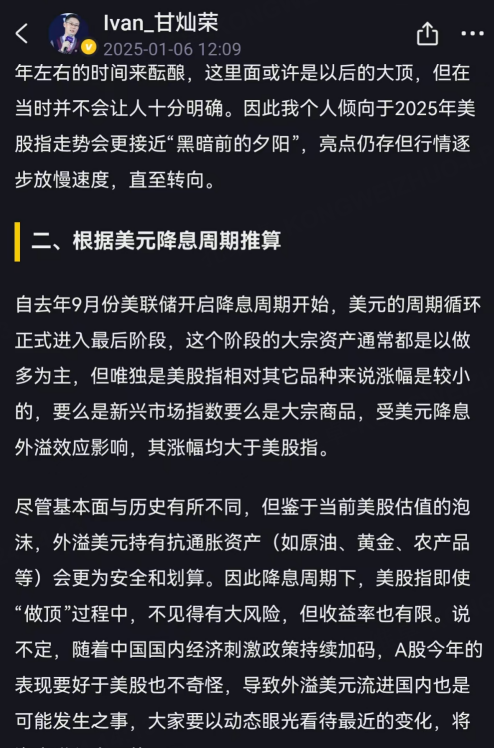

In my January 6 post titled "2025 Outlook: A 'Topping' Phase for U.S. Stock Indices," I predicted that as the U.S. dollar enters its final depreciation cycle, global capital would flow from Western markets to Asia-Pacific markets. This shift benefits indices such as China's A-shares, Hong Kong stocks, and Japan's Nikkei 225.

For overseas investors facing challenges in accessing China's A-shares directly, Hong Kong emerges as the most attractive destination. The recent surge in Hong Kong stocks reflects this trend. While a sharp correction in U.S. indices could temporarily drag down Hong Kong's market, the long-term trajectory remains upward. After any pullback, significant buying opportunities are likely to emerge.

At this stage, investors can start identifying promising targets and prepare to enter after adjustments occur. For those hesitant about individual stock selection, index futures or ETFs are also worth exploring.

The Final Phase of the Dollar’s Rate-Cut Cycle

Since the Federal Reserve initiated its rate-cut cycle in September last year, the dollar has entered its final phase of cyclical movement. Historically, this stage has favored long positions in major asset classes—except for U.S. stock indices, which have underperformed relative to emerging market indices and commodities.

Although current fundamentals differ from historical precedents, given inflated valuations in U.S. equities, holding anti-inflation assets like crude oil, gold, and agricultural products offers safer and more lucrative options compared to U.S. stocks during this period.

Even if U.S. indices remain in a "topping" phase with limited downside risks, their potential returns are constrained. Meanwhile, as China continues to implement economic stimulus measures, it wouldn't be surprising if Chinese equities outperform their U.S. counterparts this year—a scenario that could attract overseas capital into China's markets.

Market Volatility Ahead: Flexibility Is Key

As geopolitical and economic uncertainties persist under President Trump's administration (or other external factors), financial markets are increasingly susceptible to news-driven volatility. Different asset classes will react differently; for instance, commodities like crude oil and gold may experience sharper fluctuations than expected.

Such adjustments present excellent opportunities for portfolio rebalancing. Investors should maintain a flexible mindset to adapt to these dynamic changes effectively.

$E-mini Nasdaq 100 - main 2503(NQmain)$ $E-mini S&P 500 - main 2503(ESmain)$ $E-mini Dow Jones - main 2503(YMmain)$ $Gold - main 2504(GCmain)$ $WTI Crude Oil - main 2504(CLmain)$

Comments