Recently, the core variable in crude oil trading has still been the evolving situation in the Strait of Hormuz. Based on the information currently available, a second round of negotiations between the United States and Iran has already been put on the agenda. That, in itself, is a very important development. It suggests that the Strait of Hormuz crisis is moving away from a war-based resolution path and gradually shifting toward a negotiation-based one. In other words, the situation is easing rather than escalating.

This shift matters because it directly changes the pricing logic of crude oil. If the market was previously trading on the assumption of escalating conflict, supply disruption, and uncontrolled risk, it is now beginning to price in easing tensions, advancing dialogue, and a decline in the risk premium. That also means the most important driver behind the earlier rise in oil prices is now changing.

From the standpoint of real-world constraints, prolonged congestion in the Strait of Hormuz would be complex and difficult for the United States to bear. At the same time, any larger-scale direct US strike on Iran would be equally complex and difficult for Iran to absorb. After the breakdown of the first round of talks, the US move to fully block the Strait of Hormuz in effect pulled in several major Asia-Pacific economies that are highly dependent on Middle Eastern oil imports, pushing up global crude oil costs as a whole. And such a sharp increase in costs would also be difficult for those oil-importing countries to bear. From this perspective, the room for the situation to continue moving in an extreme direction is actually quite limited, while a further shift toward negotiations appears to be the more realistic outcome.

$标普500(.SPX)$ $标普500ETF(SPY)$ $SP500指数主连 2606(ESmain)$ $微型SP500指数主连 2606(MESmain)$ $微型SP500指数2606(MES2606)$ $纳指100ETF(QQQ)$ $纳斯达克(.IXIC)$ $NQ100指数主连 2606(NQmain)$ $微型NQ100指数主连 2606(MNQmain)$ $道琼斯指数主连 2606(YMmain)$ $道琼斯(.DJI)$ $微型道琼斯指数主连 2606(MYMmain)$ $道琼斯ETF(DIA)$ $微型道琼斯指数2606(MYM2606)$

The market itself is already reflecting this change. Although the first round of talks has broken down, the Nikkei and the Korean market are still rising, US Treasury yields are still falling, and both Hong Kong and A-share markets have held up reasonably well. This cross-asset price action itself suggests that the market has already started to bet that the Strait of Hormuz issue may ultimately be resolved through dialogue. That expectation is also visible in crude oil: prices have once again fallen below the 20-day moving average, indicating that the upward momentum previously driven by extreme risk is weakening.

It Is No Longer Appropriate to Chase Oil Higher

Against this backdrop, the one thing crude traders most need to avoid is continuing to chase the market higher based on an escalation narrative. The earlier rally in crude oil was driven to a large extent by fears that the Strait of Hormuz situation could spiral out of control, leading the market to pre-price supply risks. But the current reality is that the crisis is not continuing toward a path of full disorder; instead, it is moving toward dialogue. Since the core logic supporting a continued strong upside in oil prices has already begun to loosen, blindly chasing the market higher at this point clearly involves more risk than reward.

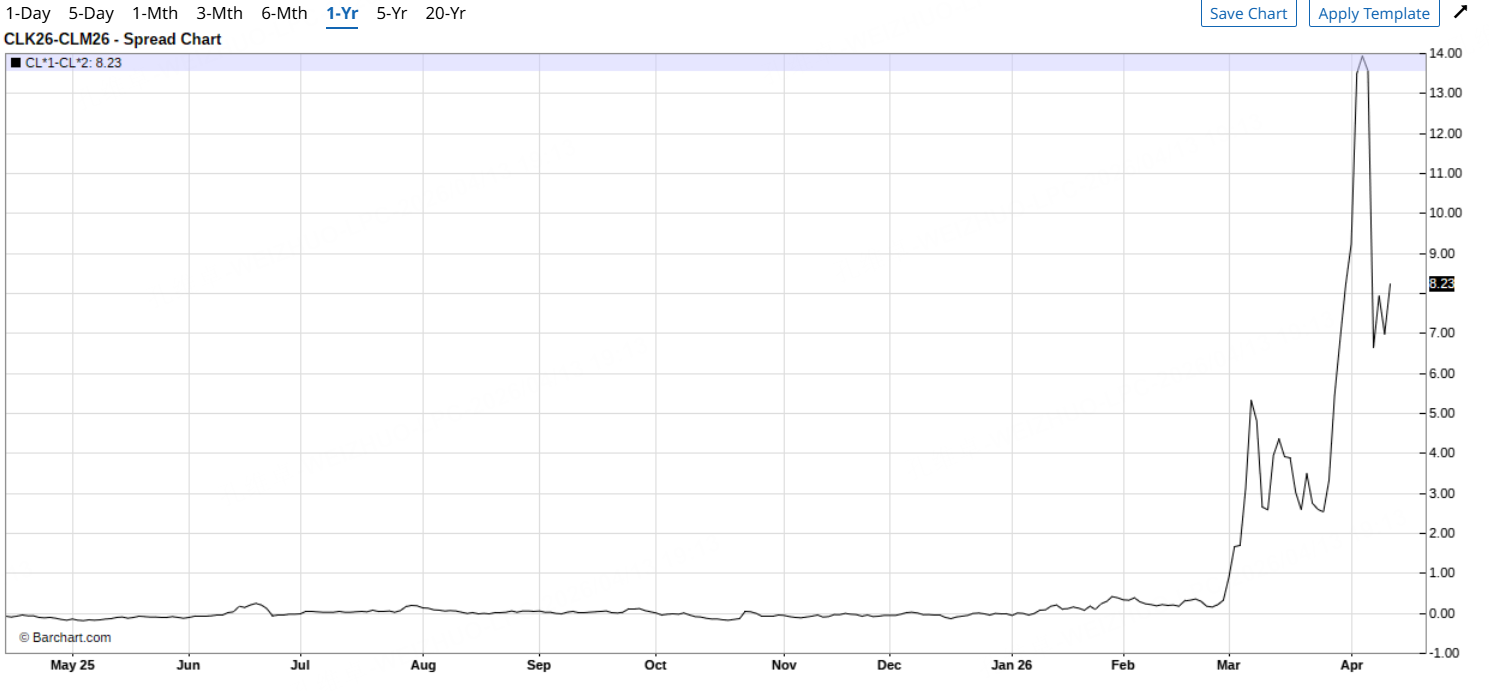

It is also important to note that WTI crude is currently exhibiting an extremely pronounced front-month backwardation structure, with the spread between near-dated and deferred contracts having risen to historically rare levels. Whenever spot premiums in oil surge to historical extremes, price action over the following two weeks often retraces in the direction of spread convergence. That view is consistent with current market behavior. From this angle, continuing to chase crude higher is no longer an attractive risk-reward proposition.

As for the current deferred-discount structure and the extent of the widening in the nearby-versus-deferred spread,

under such an extreme term structure, strategies that attempt to hedge by profiting from a further widening of the spread are no longer applicable at all. The probability that the nearby-deferred spread continues to surge meaningfully from here is already extremely low. Even if there is a brief additional spike, the upside space would be very limited. Therefore, at this stage, traders absolutely should not continue to chase crude higher blindly, nor should they keep going long the nearby-deferred spread in the hope that it widens further. The correct approach is to wait patiently for right-side confirmation and then go short the nearby-deferred spread once it begins to converge.

Ten Historical Episodes

We conducted a detailed review of ten classic historical episodes in which the front month premium over deferred contracts widened sharply and the overall term structure moved into extreme backwardation.

In August 1990, when the Gulf War broke out, roughly 4 million barrels per day of crude supply was suddenly cut off. Because uncertainty was exceptionally high in the early phase of the war, prices continued rising one week later, and only peaked and turned lower after Saudi production increased and follow-up actions were implemented.

In late August 2005, Hurricane Katrina caused widespread shutdowns of crude production facilities in the Gulf of Mexico, leading to a physical interruption in spot supply. But one week later, after the release of the Strategic Petroleum Reserve, the elevated premium converged rapidly and prices corrected materially, falling by roughly 5% to 10%.

In July 2008, at the peak of the commodity supercycle, oil hit an all-time high of $147. The extremely high price level began to destroy demand, and one week later prices dropped sharply by more than $10, marking the beginning of a historic bear market.

From February to March 2011, during the Arab Spring, the Libyan civil war caused a prolonged and genuine physical supply disruption. Because the outage was not just a short-term sentiment shock, prices did not show any obvious pullback one week later, and instead remained elevated and range-bound for several months.

In September 2019, Saudi Arabia’s core oil facilities were attacked. The front month contract gapped up by more than 15%, but one week later, strong expectations of production restoration calmed the market, and crude erased more than half of the post-attack gains.

In February 2021, an extreme cold wave in Texas forced millions of barrels of oil production offline, creating spot tightness. One week later, as temperatures rose and shale output recovered quickly, the extreme premium structure eased rapidly and prices pulled back slightly.

In March 2022, when the Russia-Ukraine conflict fully broke out, market panic triggered an epic premium structure, with spreads exceeding $20. But one week later, the market realized that Russian crude had not actually disappeared, and as panic faded, prices suffered a violent decline of more than 20%.

In October 2023, when the Israel-Palestine conflict broke out, a weekend attack caused the front month to jump. One week later, once it became clear that the conflict had not spread to core oil-producing countries, prices fully gave back the gains and even turned lower.

In January 2024, during the Red Sea crisis, shipping rerouting caused inventories in transit to rise sharply. One week later, the market adapted quickly to the new logistics normal, and oil prices moved sideways in a narrow range rather than breaking higher in a sustained way.

In April 2024, when direct conflict between Iran and Israel in the Middle East escalated, the market priced in the risk in advance. One week later, because both sides showed restraint and US inventory accumulation exceeded expectations, prices quickly fell by more than 5%, moving back toward fair value further out on the curve.

Although the triggers behind these backwardation episodes differed, they shared one common feature: all of them caused front-month contracts to surge in a short period of time, pushed the term structure clearly into backwardation, and rapidly widened the spread between nearby and deferred contracts. Looking at the outcomes, in 8 of these 10 cases, crude oil prices were clearly lower one week later, representing 80% of the sample. Their shared pattern was that both prices and spreads had over-priced risk in the earlier phase, but within about a week, prices began to return to more reasonable levels as policy intervention emerged, supply recovered, sentiment cooled, or the conflict failed to broaden further.

A Better Approach Is to Wait for Right-Side Confirmation and Then Short the Spread

If it no longer makes sense to chase crude higher, and it also no longer makes sense to stay long the nearby-deferred spread, then the next trading focus should not be to keep following the inertia of the previous phase. Instead, the market should begin preparing for the next phase of normalization. What traders should be waiting for now is not a further widening in the spread, but spread convergence, and the opportunity to short that convergence move.

The key here is not to act immediately on the left side, but to wait for a right-side setup to emerge. Even though negotiations are moving forward, the situation itself can still be volatile. So the more reasonable approach is to wait until the market genuinely confirms that the Strait of Hormuz crisis is moving toward a negotiated solution, and confirms that the risk premium is beginning to decline in a systematic way, before shorting the nearby-deferred spread.

Strategies More Suitable for the Current Oil Market

For that reason, we believe that the more appropriate strategies in the current crude oil market are neither to chase the outright price higher nor to continue chasing the long spread trade, but rather to make greater use of time decay and changes in volatility.

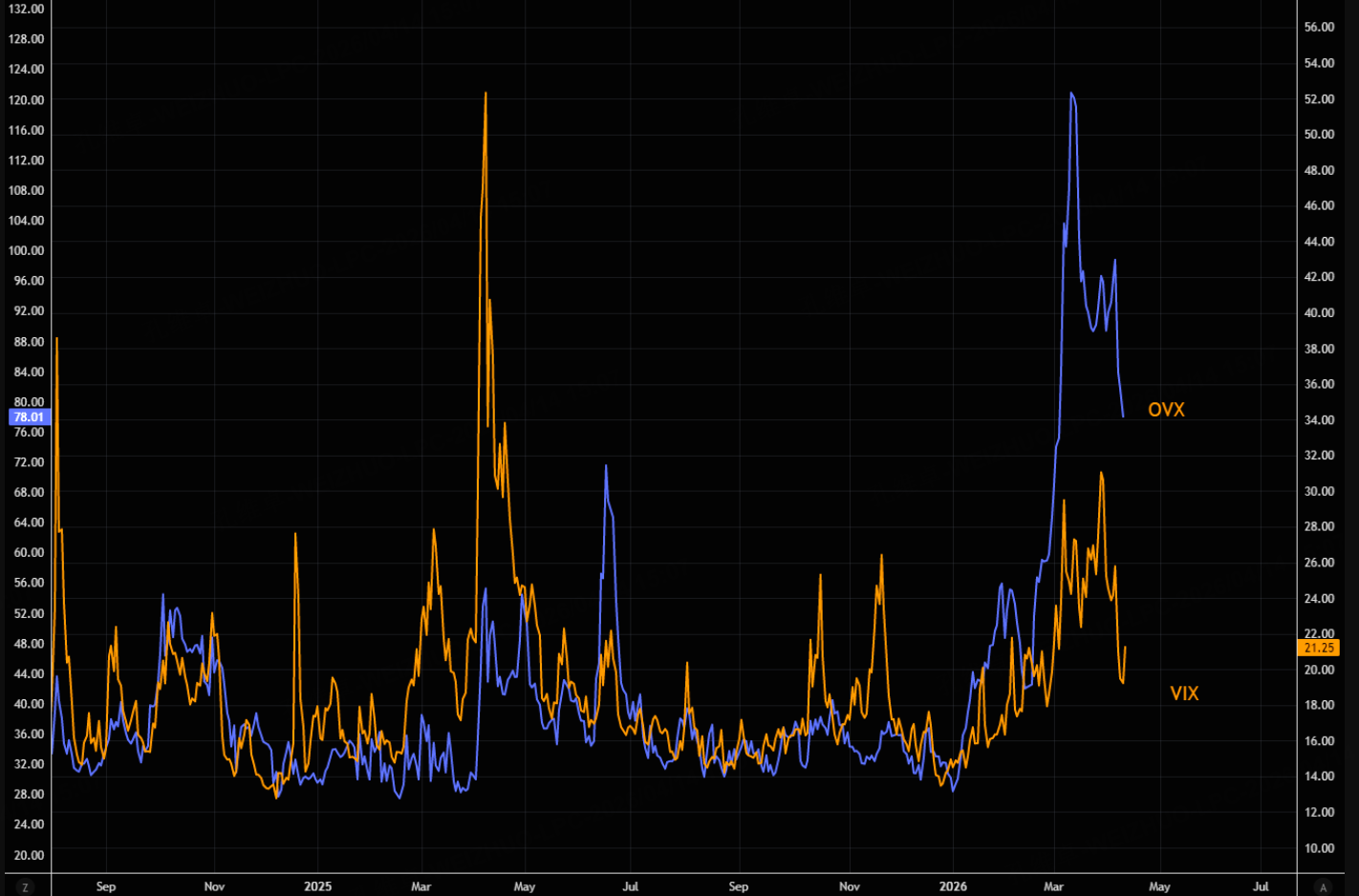

One possible approach is to sell WTI crude call options near the previous high on a rolling one-week basis. As long as negotiations continue, and as long as there remains hope for further talks, crude is unlikely to break materially above its previous high. Of course, this strategy itself still contains an element of directional betting, so position sizing must remain small. Alternatively, one can continue with the previously discussed short-volatility options strategy, which has already generated a profit of 40 points. At the same time, although crude volatility has already declined, its pullback has still been smaller than that of the VIX, suggesting there may still be room for further downside in volatility.

For futures traders, another strategy is to buy deferred crude oil futures, sell the current front contract—specifically the May contract—and buy the September contract to capture spread convergence, with a stop-loss triggered if WTI crude futures rise back above the 20-day moving average.

$美国原油ETF(USO)$ $WTI原油主连 2605(CLmain)$ $小原油主连 2605(QMmain)$ $WTI原油2605(CL2605)$ $原油ETF-PowerShares(DBO)$ $微型WTI原油主连 2605(MCLmain)$ $两倍做多彭博天然气ETF-ProShares(BOIL)$ $天然气主连 2605(NGmain)$ $天然气2605(NG2605)$

Comments