There was a small reversal in the global market on Thursday:

-The US stock market fell slightly, with the Dow down 0.02%, the S&P 500 index down 0.31% and the Nasdaq down 0.35%

-Gold price fell by nearly 1%

-Oil prices fell by 3%, and US crude oil futures fell below the 50-day moving average, triggering fund liquidation

-The US dollar index rebounded slightly

Although the market volatility is not large, the familiar pattern of "the dollar rises, everything falls" has appeared again. The reasons behind last night's market reversal need to be paid enough attention-the spoiler of the Federal Reserve appeared-and a sentence from Fed officials brought people back to reality.

At present, the market expects the Fed's end rate to be below 5%. Compared with Bullard's end rate expectation, it is obvious that the market is too optimistic. Recently, many people are afraid of missing opportunities and entering the market, but they need to understand a question-will the end interest rate expectations you see not change?

Bullard's speech is not a one-day market, and the market needs to continue to digest it, so it is necessary to study his speech carefully:

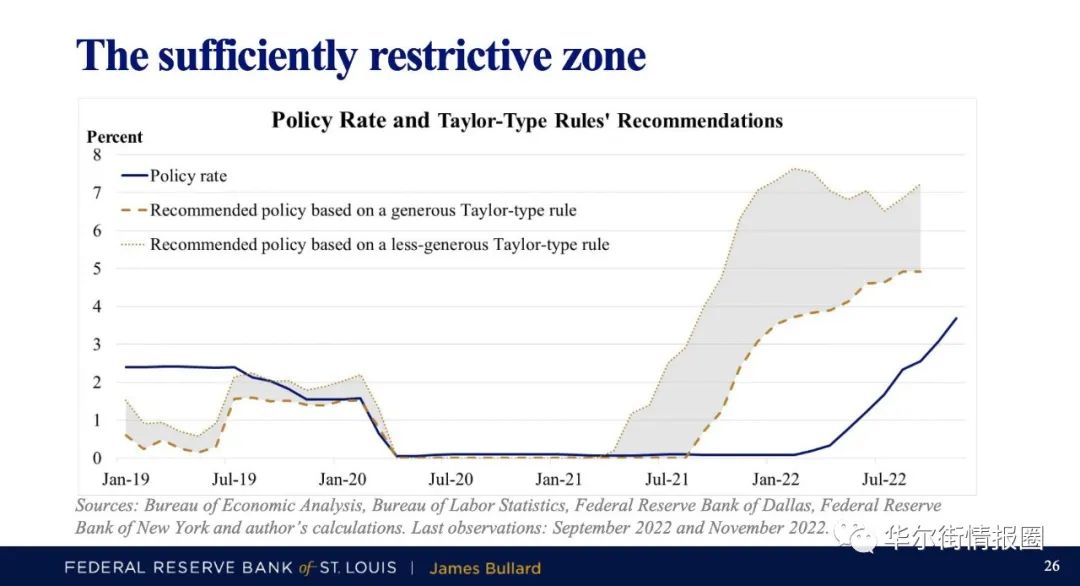

1. Bullard spoke at an economic conference in Louisville, Kentucky, not an impromptu interview with the media, so every word he wrote was carefully prepared. He even showed a chart-even using the "dove" hypothesis, the basic monetary policy rules require the Fed's policy interest rate to rise to about 5%, while the stricter hypothesis will require the interest rate to rise above 7% (implication: raising interest rates to 5%-5.25% is still optimistic, and the end rate is expected to be further raised).

PPT used in Brad's speech

Mr. Bullard showed charts suggesting that the so-called sufficiently restrictive rate could be between 5% and 7%, though he did not say how high he supported. The calculation is based on several different versions of Taylor's rule.

2. I will let Chairman Powell decide how much to raise interest rates at any time. If you add more now, it will be less in the first quarter of next year. If the increase is less now, there will be more in the first quarter of next year (implication: don't hype too much about how much to raise interest rates at a meeting, even if the increase of 50 basis points in December is not a signal of policy change).

3. It is obvious that there is a need to continue to raise interest rates. The latest report of lower-than-expected inflation only provides "preliminary" evidence that the downward trend of inflation is taking shape. The data showing that inflation slowed in October is "prone to the opposite situation in the next month", and the Fed has been "burned" by inflation far higher than its 2% target for two consecutive years (implication: don't look at inflation optimistically, it may reverse at any time, and more data are needed to support it).

4. If inflation falls faster than expected, the whole target range of policy interest rate may fall (implication: the current expectation of end interest rate is not the final expectation, and will change).

5. So far, the change of monetary policy stance seems to have only a limited impact on the observed inflation, but the market pricing reflects that inflation is expected to decline in 2023 (implication: the market performance is somewhat optimistic).

6. The market expects inflation to fall in 2023. If this happens, it may form a "very good trend" and avoid recession in the United States. 2023 may be a year when the process of falling inflation takes shape, and enterprises are reluctant to raise prices in order to keep the market quota. But "caution is necessary" because investors and Fed officials "have been predicting for the past 18 months that a fall in inflation is just around the corner" (implication: this is the best situation and the goal pursued by the Fed).

7. Interest rates will remain high for some time to avoid repeating the mistakes of 1970s (implication: don't hype interest rate cuts easily).

8. Although interest rates have risen sharply this year, the St. Louis Fed's financial stress index shows that the stress level is relatively low (implication: the effect of raising interest rates is not as expected).

In an interview with reporters after the speech, Bullard said that in the past, I thought 4.75%-5% would be fine, but based on the current analysis, I would suggest increasing it to 5%-5.25%.This is the lowest level. According to the analysis, at least this level can keep the interest rate in a restricted area.

Many media have described Bullard as the "hawk King" because he is a hawk within the Federal Reserve. However, he is a "close friend" of Federal Reserve Chairman Powell. He mentioned "respecting/listening to Powell's views" on many occasions. If his speech this year is repeated, many views are exactly the same as Powell's.

On the same night that Brad delivered a speech that shocked the market, Goldman Sachs also released a shocking report (a report on the theme of 2023 written by Dominic Wilson, an analyst at Goldman Sachs).

One sentence reads as follows: Rising interest rates and a stronger US dollar will dominate 2023, and the US dollar still has a lot of support, and the conditions for change have not yet been put in place.

Most people may not see anything, but it is "very surprising" to professionals, because more than 90% of investment banks on Wall Street expect the US dollar index to start reversing either by the end of this year or the first quarter of next year, but at different times.

$E-mini Nasdaq 100 - main 2212(NQmain)$ $E-mini Dow Jones - main 2212(YMmain)$ $E-mini S&P 500 - main 2212(ESmain)$ $Gold - main 2212(GCmain)$ $Light Crude Oil - main 2301(CLmain)$

Comments