Many people may not realize how cheap Chinese assets is coming to be after a long period of selling.

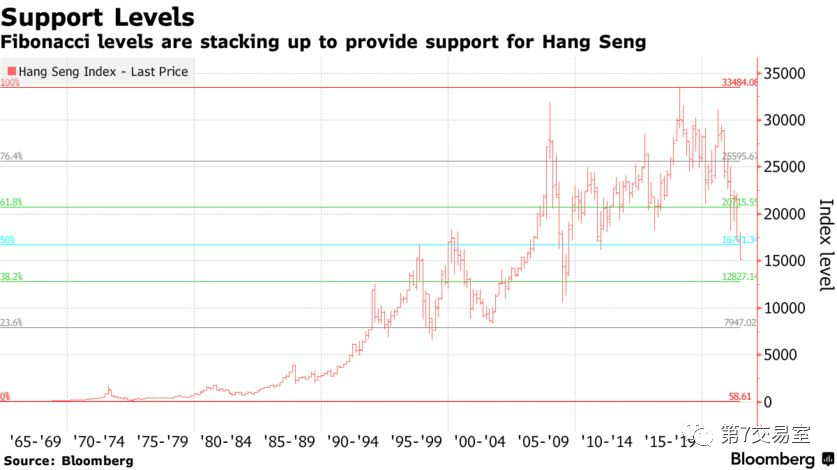

Take the Hang Seng Index for example. If we check the ultra-long-term monthly chart of the Hang Seng Index, we will find that Hang Seng has fallen below the upward trend line since the 1980s.

Horizontally, the Hang Seng Index is close to the low point of Lehman crisis of 2008, . Judging from the current trend of the global economy, this has obviously be undervalued in the negative news

Hang Seng's MACD bottom deviation has become more and more obvious. If we can grasp it correctly, it may be a cycle of oversold rebound for more than 2 months, and the risk-return ratio is greatly cost-effective.

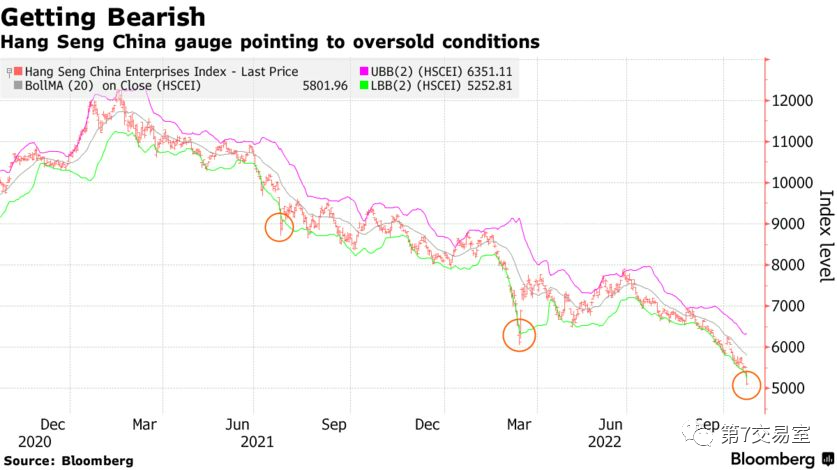

From the boll index of Hang Seng Weekly Line, the current decline has greatly exceeded the place where the lower edge of the index is twice the variance,

Every time there is a similar trend, the oversold rebound will last for more than 2 months. If there is no big bad news, it is obvious that this place needs short covering.

Let's look at Nasdaq Golden Dragon China Index again, and its current position has returned to the position in 2013, which is much lower than that of Shanghai Stock Exchange.

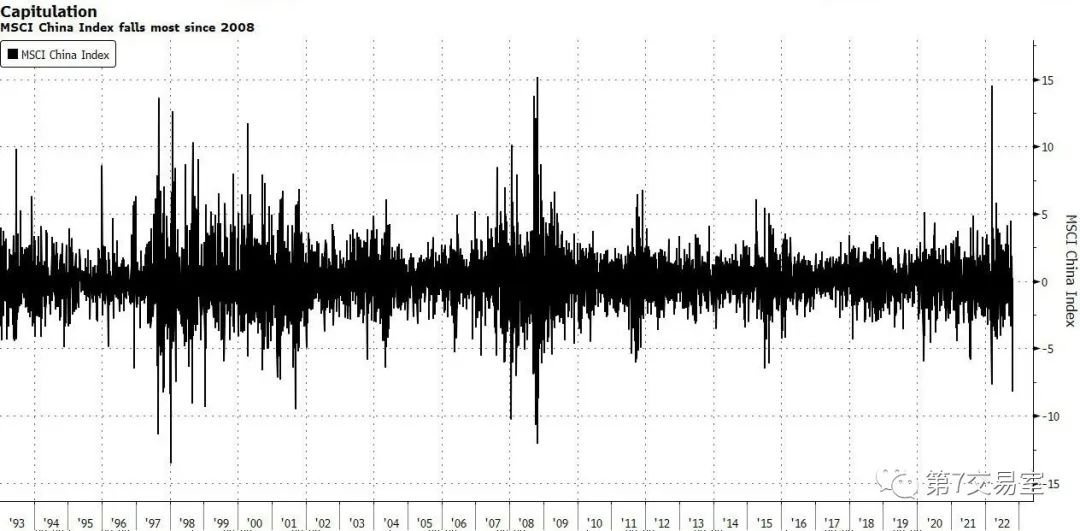

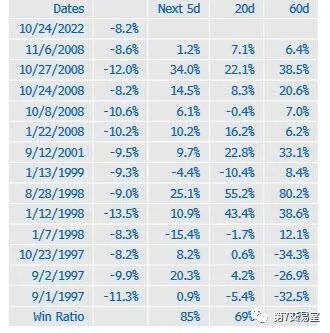

The MSCI China Index has fallen by more than 8%, almost the biggest daily decline since 2008

If we make a statistic on every time the MSCI China Index falls by more than 8%, we will find that the index return rate will keep rising in the next 5, 20 and 60 trading days, and the number of rises result is also increasing.

Is this winning rate very attractive?

The rise of the US dollar may have come to an periodical end

The global market began to save itself crazily

Since October 11th, many countries from Europe to Asia, such as Britain, Japan and South Korea, have taken various measures to rescue the market in response to the rising US dollar index.

This shows that the non-US market has become increasingly unable to bear the pressure of a strong US dollar, and it also means that the US dollar has probably not remained at a high level for a long time.

Because according to our observation, once the strong dollar attracts more hot money from major economies than these countries can bear and triggers economic crises in Europe and Japan, a financial turmoil no less than that of 2008 would erupt, with the consequence that the global economy would fall into recession and the United States would not escape.

Near the mid-term elections, the Fed, which is just right to balance the expectation of rising interest rates with the economy to the extreme, dare to detonate this time bomb before the election? This is bound to create more troubles for itself when the power of the two parties is transferred.

Therefore, we might as well boldly predict that the current interest rate ceiling of about 4.5% denominated by the 2-year US bond yield is the peak of this year's interest rate hike, while the end point of interest rate hike of more than 5% denominated in the swap market has been overdrawn to a great extent!

Historically, every time the Bank of Japan intervened in the exchange rate, the exchange rate of the Japanese yen against the US dollar rebounded in return , and the US dollar index retreated accordingly. Therefore, we have reason to believe that this timing is a tacit understanding maintained between the two big banks in the United States and Japan for a long time. Then this time should be no exception.

At present, the overvaluation of the US dollar index compared with other currencies has reached the highest level since 2002. If it is not handled well, the result will undoubtedly be a recession shock no less than that of 2008, but we believe that even if there is a hard landing, the Fed will not let it happen before the mid-term elections.

S&P has started to test the rebound at a higher position from the 20-day moving average, but you should be careful. According to the classic bear market cycle theory, when the US stock market hits the bottom of panic, it will hit the wall of worry upward. Because the bad news is not exhausted,

The same double dip has probably been completed on Hong Kong and chinese stocks. After bottoming out, the two markets of A Hong Kong are believed to have a brighter performance under the endorsement of a tougher and more stable economy.

What do you say?

$E-mini Nasdaq 100 - main 2212(NQmain)$ $E-mini S&P 500 - main 2212(ESmain)$ $E-mini Dow Jones - main 2212(YMmain)$ $Gold - main 2212(GCmain)$ $Light Crude Oil - main 2212(CLmain)$

Comments