Will the dollar continue to fall? What does the crude oil have to do with the US dollar?

Today, let's talk briefly about a strange situation: someone suddenly bet on the continuous decline of the US dollar.

Yes, you are not mistaken.

Although the US dollar index has stabilized and rebounded around 106, a large number of traders already believe that the decline of the US dollar probably does not stop there. They seem to be betting on such a script:A bigger round of dollar selling will start at any time, and the trend of the dollar index will appear in the typical form of head and shoulder top, thus turning downward in reverse.

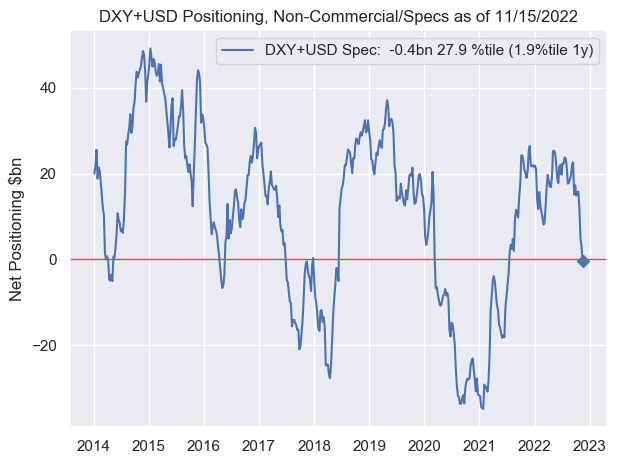

From the latest CFTC position data, there is a rare jump in the overweight of the asset management market in the US dollar short position, which makes the short position of the asset management market reach a new high in the past two years as of last week

From the historical trend, every time such a short bet appears, the US dollar either directly bottomed out, or rebounded sharply and then turned down, with few cases of continuous upward movement.

If you think that short positions on asset management may be the need of hedging strategy, look at non-commercial positions and speculative bets:

As of November 15th last week, the positions of non-commercial and speculative positions have suddenly changed from the sharp bullish positions in previous months to neutral positions, and the bullish positions against the US dollar have been reduced to around the 0 axis.

This is no coincidence, but if anyone thinks that the CFTC data has a delay effect and is not enough to reflect the truth, then take a look at this:

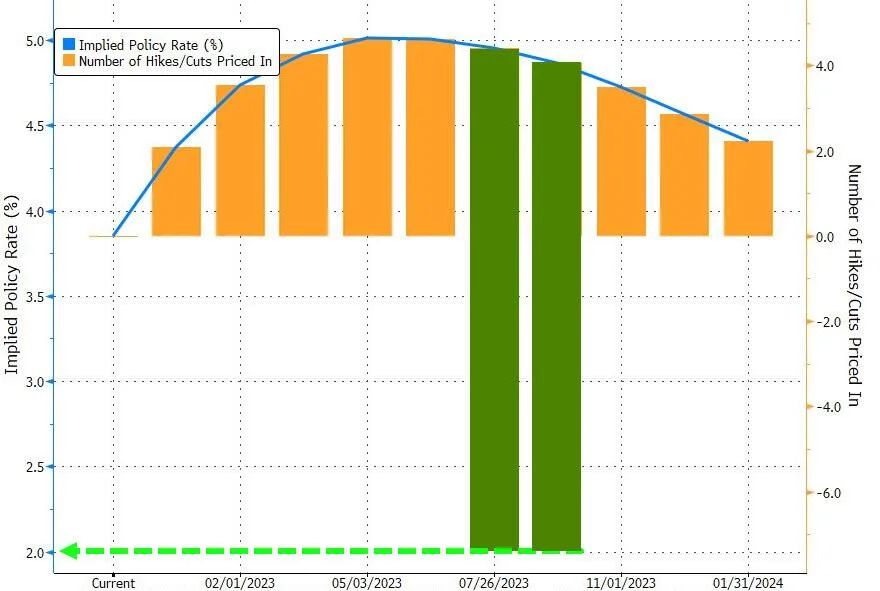

Just on Monday, in the obscure overnight rate futures options market, in the American banking system, on the September 2023 futures of the overnight repo rate of Treasury bonds, some people suddenly made a big bet that the interest rate of sofr would return to 2%.

According to the data released by Bollingbroke, a local US brokerage firm, the premium of this bet is about 4.5 million US dollars, and the target is that the policy interest rate before the option expires is about 2%; Oddly, however, the US swap market predicted an interest rate of 4.9% over the same period, a difference of nearly 300 basis points. This makes the whole interest rate futures market have a strange change in the price structure of the future Fed interest rate hike path:

The projections on the chart suggest that the Fed may even cut interest rates abruptly by next September after raising rates above 5 percent?

If the CFTC data may have timeliness reference error due to lag, then combined with the large bets on interest rate futures options, this bearish significance cannot but attract enough attention.

Moreover, according to the latest data from CFTC, the asset management market not only increased the short position of US dollar, but also reduced the net short position of Japanese yen and British pound, and increased the bullish bet on euro.

M&, an institution that manages about $440 billion; G also added long-term US bonds to his portfolio in the recently released position data. They said that the yield of US bonds will probably go down from now on, and the price of US bonds has fallen enough.

Obviously, more and more traders are betting on the reverse decline of the US dollar and the collapse of US bond yields.

Why?Prepare for the early impact of recession

Such a bet would not have been possible without the early shock of a Great Recession, so what caused the sudden rise in recession expectations?

There are two main reasons:

OneIt is the false prosperity of the American economy supported by debt expansion, but the fundamental rift has become bigger and bigger, and the result of recession has become very obvious. It is only a matter of time before the impact.

Second,There is a big problem with the liquidity of US debt. After nearly two weeks of continuous fermentation, the start button for the re-collapse of US debt is in the hands of the Fed, and if the Fed wants to passRecession to completely eliminate inflation and trigger a second earthquake in the global market is actually very simple, and judging from the global miserable model, the United States must not be the worst in the end.

Let's talk about the first reason.

We all know that although the GDP of the United States hovered twice on the edge of recession in the last three quarters, the GDP of the latest three quarters unexpectedly broke a good result of 2.6%. However, as a result, US stocks actually rose instead of falling against the background of rising interest rate expectations, which actually showed that the market doubted the Fed's continuous interest rate hike, and did not believe in the economic fundamentals of the third quarter.

According to the data of the Federal Reserve Bank of New York, in the third quarter of 2022, household debt increased at the fastest speed since the first quarter of 2008, that is, since the subprime mortgage crisis!

This data was just released this week. Last quarter, household debt increased by $351 billion, reaching a total of $16.5 trillion, an increase of 8.3% year-on-year. The terrible thing about this data is that people's borrowing behavior has not cooled down due to the interest rate increase data, and it also indicates that inflation will be more sticky in the future.

On the contrary, housing prices in the United States have shown signs of collapse before the Great Crisis in 2008.

Existing home sales in the United States plunged by 5.9% month-on-month in October. This is the ninth consecutive month that sales have declined. Sales of existing homes fell 28.4% year-on-year, the lowest level since 2008:

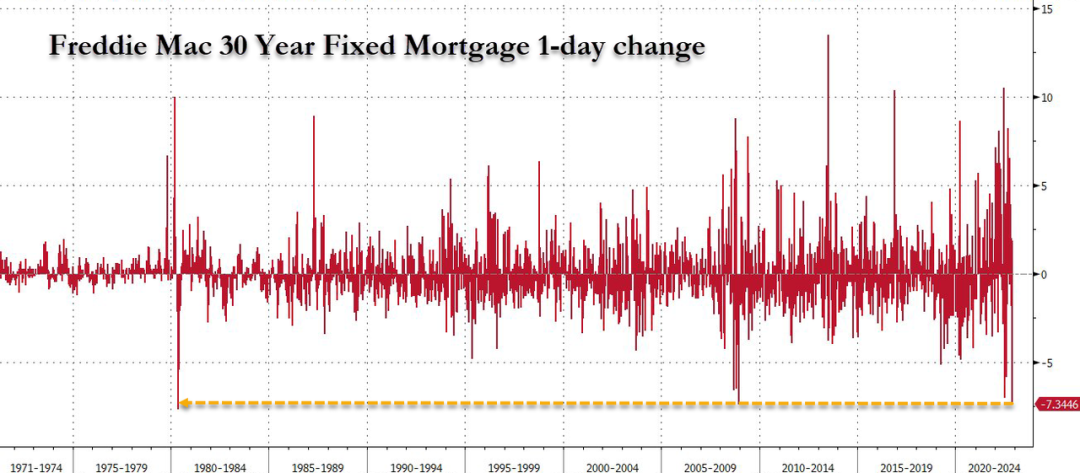

In the past week, mortgage rates plunged by nearly 0.5%, the biggest weekly decline since November 1981.

Under the cycle of raising interest rates, the mortgage interest rate is lowered against the trend. It can be said that American real estate developers and banks are fighting to the death, that is, to increase the sales of existing homes and once again lower their profit margins. The dilemma of American real estate industry is more horrible than that of China.

There are also layoffs with the same signs as in 2008. As we mentioned last time, American technology giants have laid off a large number of employees, including Amazon, Twitter, meta, etc. Almost all well-known American technology companies are laying off a large number of employees. According to rough statistics, 67,000 people have been laid off, and this is only the beginning.

A CNN editorial predicted that if the Fed keeps interest rates high for longer, we will see a tsunami of layoffs in 2023, and millions of people will lose their jobs.

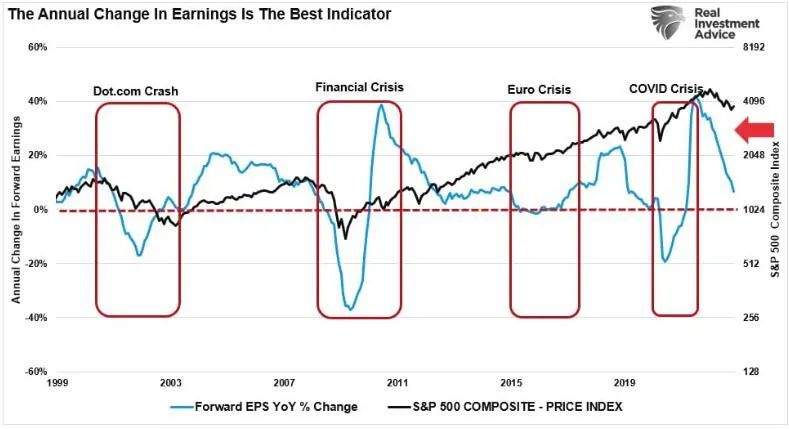

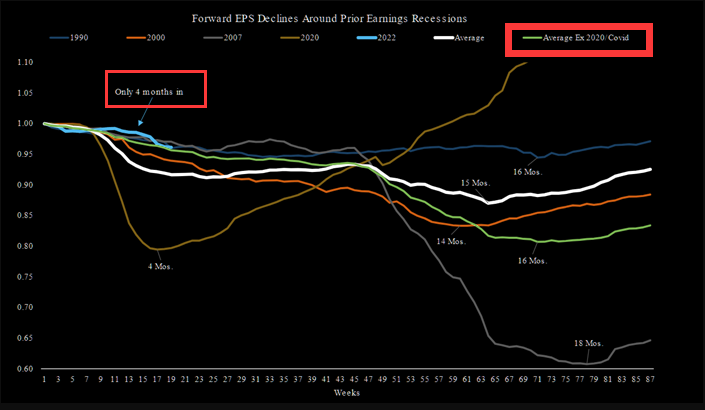

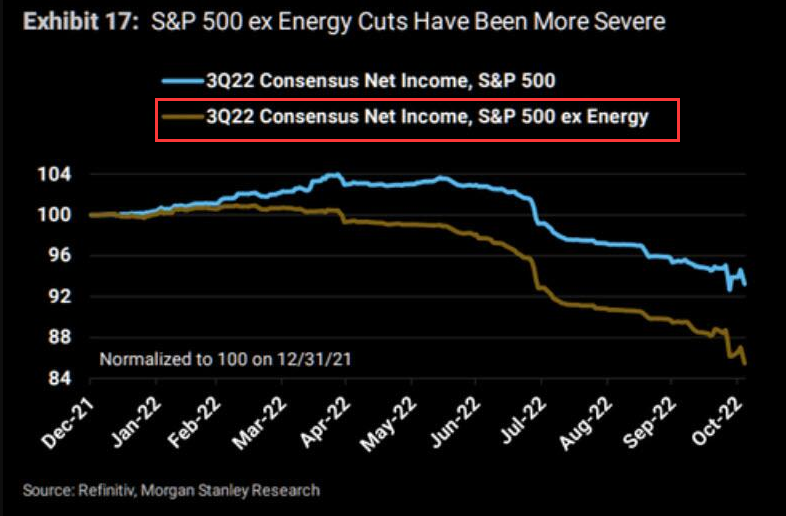

Let's take a look at the comparison of the annualized decline in EPS of S&P 500 companies in previous crises:

This decline still seems to be insufficient, and according to Morgan Stanley's statistics, assuming that the recession is really coming, there must be at least 10% room for the profit results of American enterprises to fall, and less than one-fourth of them have just finished in time.

Then another problem arises:

The false prosperity of GDP in the third quarter of the United States is probably supported by the profit of the energy industry and the consumer market that depends on borrowing. For a long time, consumption has accounted for more than 60% of GDP. However, under the weak wage growth, the dilemma of real estate sales and the high cost of living and production, why can Americans still maintain vigorous spending power?

The answer may be related to the advanced consumer culture and inflation in the United States. Under the background of soaring prices, Americans can only increase their debts to maintain their living standards, which is exactly the same as before the subprime mortgage crisis broke out in 2008.

When U. S. stocks have not gone out of the 2008 trend, the U. S. economy is already showing signs of a return to the Lehman crisis. Therefore, the probability of recession at the next stop should be above 80%

Let's talk about the second reason.

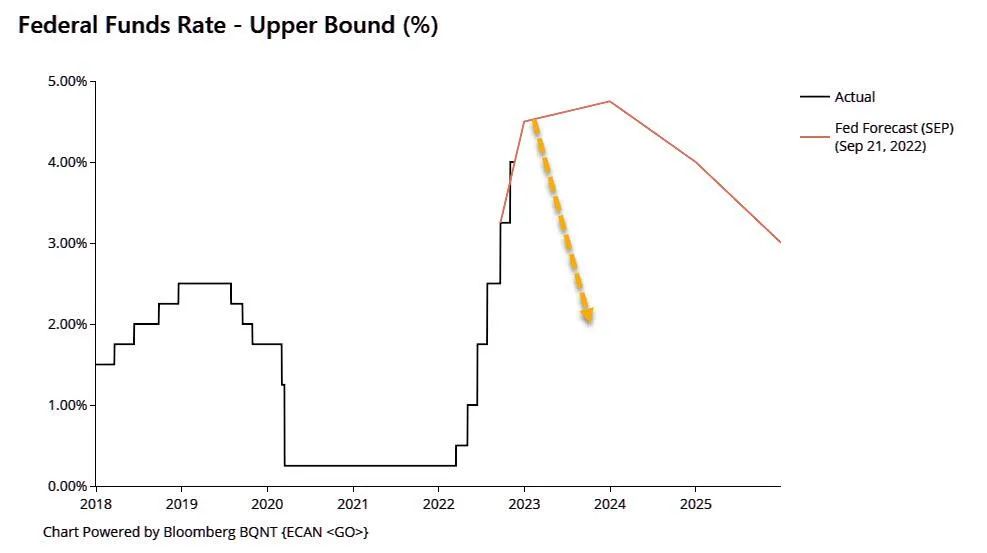

Looking back at the past history of interest rate hikes by the Federal Reserve, every sharp interest rate hike ended with a bigger economy, and even the recession would hit after the interest rate peaked and the interest rate cut started.

< img src= "https://static.tigerbbs.com/bac076e9279a24ce8417cc6619721cc4" tg-width= "793" tg-height= "470" referrerpolicy= "no-referrer" >

Then this time may be no exception, because from the perspective of US debt liquidity, the collapse is not a distant thing.

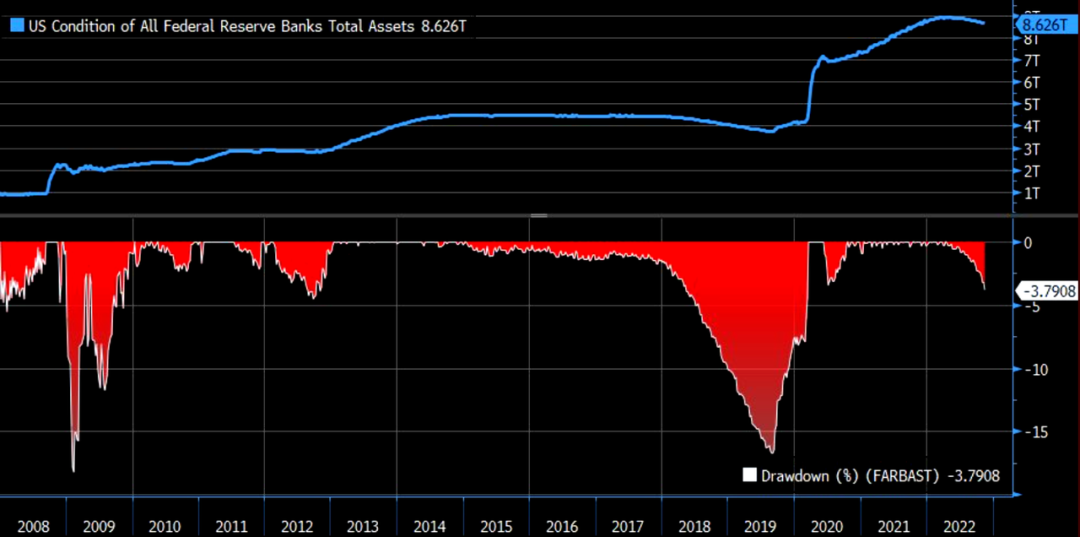

Shrinking the table is the discoloration of the market at the beginning of the year. And now dismiss the concept, Compared with the fastest rate hike in history by the Federal Reserve, the actual process of scale reduction is very slow, because they know that compared with the market, the rate hike is only an economic negative, and the scale reduction will directly trigger the stock market selling and lead to the recession coming ahead of schedule, so the Fed has been very careful in scale reduction.

This year is coming to an end, but the promised monthly reduction of 90 billion has been delayed. From the historical data, the assets of the Federal Reserve are still close to a high of 9 trillion

The speed of shrinking the watch is also slower than before.

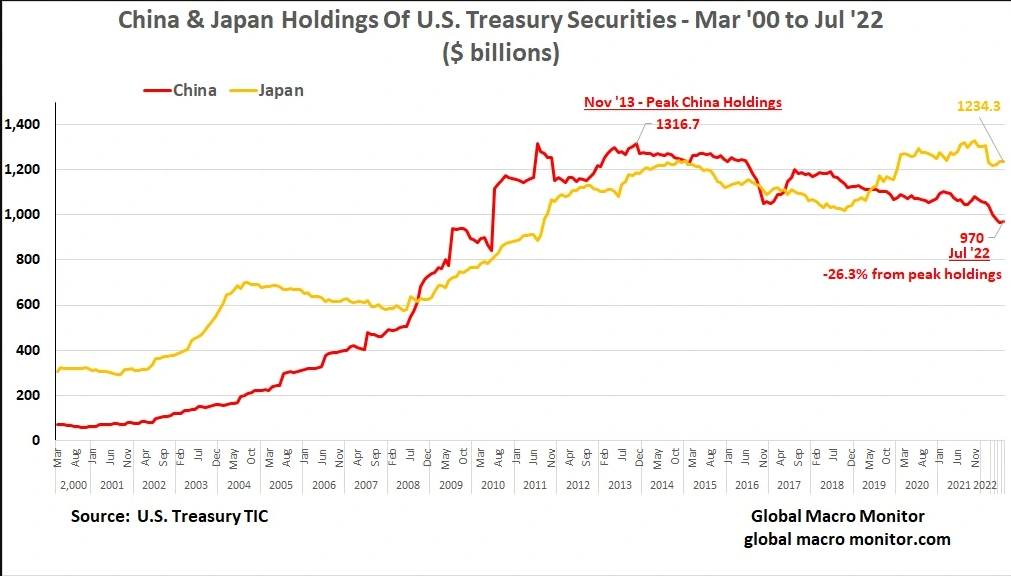

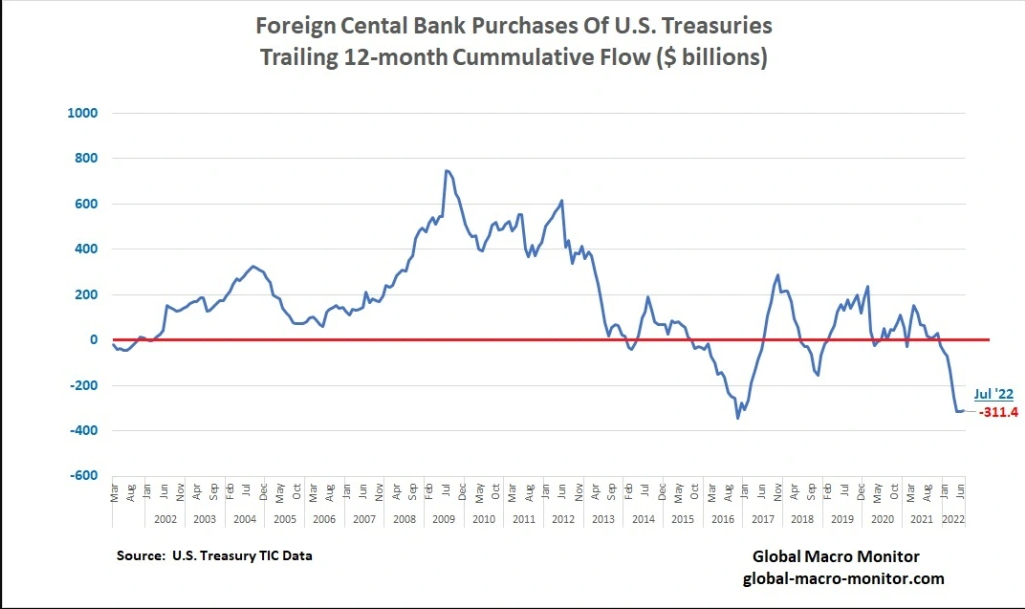

Because apart from the Federal Reserve's selling of US debt, Japan and China, the two major US dollar holders, continue to sell US debt.

Data released by the U.S. Treasury Department show that foreign holdings of U.S. Treasury bonds fell to the lowest level since May 2021 in September, led by Japan and China.

China's offshore dollar assets fell to $7.296 trillion from $7.509 trillion in August. Last May, foreign holdings were $7.144 trillion. Japan, the world's largest holder of foreign U.S. debt, saw its holdings of U.S. Treasuries fall to $1.120 trillion in September from $1.199 trillion last month.

In fact, not only China and Japan, but also overseas central bank holdings of US dollar bonds have been falling continuously this year. When the United States kicked Russia out of the US dollar payment system, it was very dangerous for major central banks to use US debt as foreign exchange reserves. What's more, under the expectation of recession, the future yield of US debt could not be guaranteed,

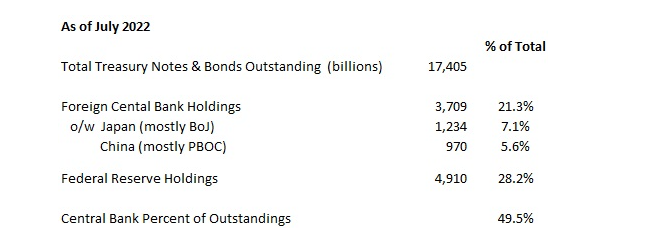

Let's take a look at the proportion of government bond purchases released by the US Treasury Department in July this year

Global central bank purchases accounted for 49.5% of US debt issuance, overseas entities accounted for 21.3%, and the Federal Reserve accounted for 28.2%.

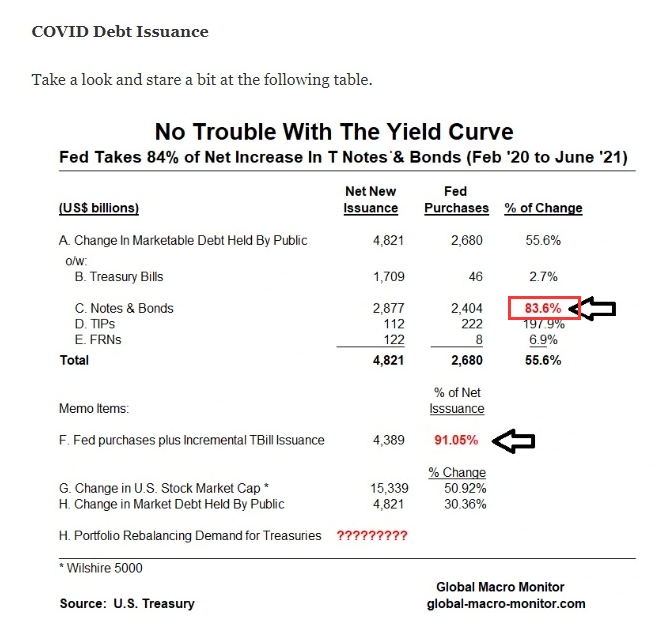

According to the document issued by the Ministry of Finance last year, the Fed's purchases accounted for 84% of the new short-and medium-term bonds of the Ministry of Finance from February 20 to June 21.

You see, the Federal Reserve has siphoned off almost all short-term government bonds. How dare it sell US bonds in a big way? Especially at present, when overseas central banks sell US debt and domestic households' debt burden is too heavy, it is doomed to be difficult to push forward the scale reduction.

After the latest CPI was released, inflation just showed signs of peaking, so as of November 16th, the balance sheet size of the Federal Reserve couldn't wait to start bottoming out, and the overall market value of US stocks also stabilized and rebounded.

However, this does not mean that the process of tightening the Federal Reserve is over. The start button that triggered the second collapse of US debt is always in the hands of the Federal Reserve. This seems to be the last choice of the powerful class in the US economy when there is nothing to do

There is a possibility that we can't disprove: now that recession is inevitable, if inflation is too sticky, it will stillIf it remains high, will the Fed press the switch of continuously shrinking its table and raising interest rates, and let the economy fall freely? This will not only completely eliminate inflation, but also enable the US dollar to complete the final harvest of international capital in a miserable mode. Anyway, when the global economic crisis breaks out, the worst thing will not be the United States, and US stocks will return to the previous low in a big deal. With the blessing of the return of international capital, it is possible to go out of the trend of bottoming out and rebounding.

As we said at the beginning, some people are betting heavily on the Fed's interest rate cut, which is probably betting on two market prospects: One is that the Fed has continuously reduced its table and raised interest rates in the past two quarters, which triggered the recession to hit ahead of schedule, so it cut interest rates ahead of schedule in the third quarter. Second, the Federal Reserve will maintain the current tight balance, slow down the steps of raising interest rates, and start to cut interest rates when the unemployment rate rises sharply, so that a soft landing can be realized. Because there is no tighter overweight, the US dollar will resume its decline after coming out of the last wave of rebound.

How to go, we can keep an eye on the changes of unemployment rate and inflation data. However, it is necessary to give you a wake-up call: the reason why the overall earnings of the S&P index are not so ugly at present is because of the profit contribution of the energy industry.

The bright eye of GDP and the increase of US fiscal revenue are closely related to the high crude oil and natural gas. It can be said that energy price is an important weight to ensure the continuous return of international capital to the United States.

Imagine that if the prices of natural gas and crude oil collapse completely, the imported inflation in Asia-Pacific and Europe will ease, and the real interest rate of non-US currencies will rise, suppressing the trend of the US dollar index. At that time, what will the United States take to cut leeks?

So we judge that the United States may be more willing to let high energy prices exist for a longer time than to let inflation fall. Then, in this way, the recession will be triggered by raising interest rates, and the final cut of the high dollar will be completed. It's more likely.

$E-mini Nasdaq 100 - main 2212(NQmain)$ $E-mini S&P 500 - main 2212(ESmain)$ $E-mini Dow Jones - main 2212(YMmain)$ $Gold - main 2212(GCmain)$ $Light Crude Oil - main 2301(CLmain)$

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- Kel9670ong·2022-11-26quite hard to predict4Report

- criticalbomb·2022-11-25thanks you very much ❤️❤️❤️8Report

- dnp·2022-11-26tq very much for sharing7Report

- WinnerTay·2022-11-26Too hard for me learn6Report

- Andie8392·2022-11-27thanks for sharing .. good post2Report

- Karma Rider·2022-11-27從來都沒有看過那麼厲害的PO文!3Report

- mel18·2022-12-02okLikeReport

- XIN.wyanny80c·2022-12-01WowLikeReport

- lyoshen·2022-11-28[smile]LikeReport

- Camper·2022-11-28[Cool]LikeReport

- JamesfromSG·2022-11-28👍🏼LikeReport

- OMZ·2022-11-27Yes1Report

- Alex Tan·2022-11-27ok1Report

- RocketBull·2022-11-27gfc1Report

- Awesome_derp·2022-11-27Ok1Report

- 一支升GoGo·2022-11-27👍LikeReport

- juenming1993·2022-11-27FLikeReport

- Wenyin·2022-11-27KLikeReport

- Johnleong·2022-11-27👍LikeReport

- Jasonyong123·2022-11-27👍🏻LikeReport