First, I want to share a screenshot from my previous analysis of silver and gold price action.

In that earlier piece, I said silver’s short-term top—assuming the Fed did not turn more hawkish and there was no black-swan surge in the U.S. dollar—should be above 130, while gold could be headed above 5,000. A little over a week later, silver has already printed a new high, and gold has also surged well past 5,000.

$白银主连 2603(SImain)$ $白银2603(SI2603)$ $2倍做多白银ETF-ProShares(AGQ)$ $白银ETF-iShares(SLV)$ $微白银主连 2603(SILmain)$

Why I Believe The Coming Gold Surge Could Be Bigger Than You Imagine

But the situation has clearly changed in a major way. As we discussed before, there were two key downside risks around a silver top:

(1) the Fed chair being not Hassett but a hawkish figure, which would push the Fed overall in a more hawkish direction; and

(2) physical inventory for March silver delivery suddenly becoming sufficient, or a sudden resolution of the delivery squeeze.

Either of these could trigger a sharp decline in silver, and it is now clear that the first risk has materialized: Hassett has been confirmed not to be the Fed chair, and the chair turned out to be Warsh—widely regarded as a hawk

This outcome feels strange and highly dramatic. Immediately afterward, global markets saw heavy selling, including derivatives tied to gold, silver, copper, and iron, as well as the Hong Kong and A-share markets.

What I find particularly odd is that Waller—relatively more moderate—was also initially considered a leading candidate, yet Trump nominated Warsh instead of Waller. To improve his chances, Waller even cast a dissenting vote during the Fed’s decision to pause rate cuts, signaling support for cutting rates; but even after aligning himself with Trump’s stance, Trump still did not pick him.

In my view, Trump chose Warsh for two reasons.:

On the one hand, Trump likely believes Warsh will still follow his lead and continue pushing an accommodative policy path. On the other hand, Warsh may be somewhat inconsistent in what he signals: he may not fully agree with the “weak dollar” direction and may instead want to use a relatively more hawkish Fed as a counterbalance to preserve what remains of the dollar index’s credibility and to stabilize an increasingly fragile dollar index trend. This is a technical cliff, and Trump’s decision to nominate Warsh is a message to the market that he does not want the dollar index to fall off that cliff—consistent with my prior analysis.

$美元指数(USDindex.FOREX)$ $美元树公司(DLTR)$ $新兴市场美元债ETF-iShares(EMB)$ $美元ETF-PowerShares DB(UUP)$

So what should we do now? I think the more actionable opportunity at the moment is in silver. If silver breaks below the 10-day moving average—specifically, silver futures—then the approach is to short the front-month March contract while going long the deferred June contract, setting up a calendar-spread arbitrage trade. This is a classic bear spread strategy.

The recent topping pattern has already been broken, so everyone should focus closely on support at the 10-day moving average. Note that the 10-day moving average here also corresponds to the lowest point of that topping pattern, so if price breaks below it, the downside acceleration could be significant.

From a technical perspective, if silver has topped and shifts into a retracement path, the pullback could be substantial because the prior run-up was so large and the gold–silver ratio has fallen to an extremely low level for this century.

$黄金主连 2604(GCmain)$ $微黄金主连 2604(MGCmain)$ $1盎司黄金主连 2604(1OZmain)$ $迷你黄金主连 2604(QOmain)$ $美元黄金主连 2602(GDUmain)$ $微黄金2602(MGC2602)$ $黄金矿业ETF-VanEck(GDX)$

If the gold–silver ratio rebounds, then either gold accelerates higher or silver accelerates lower. The downside momentum in that scenario could be very strong, and a 50% drawdown cannot be ruled out—meaning a weekly move down into the 70–60 range.

Given the potential size of such a move, a three-month bear spread is relatively appropriate. Silver volatility remains high, and if a rebound occurs, stop-running can be aggressive. Selling the near month and buying the far month can reduce losses from adverse stop-runs during sharp declines, while also leaving room to manage the position if silver later resumes an upward trend

If the 10-day moving average support breaks, you can consider the Sell the near-month futures contract and buy the far-month futures contract. combination. If silver recovers and closes back above 10-day moving average support, cut the trade immediately. It is best to wait for the daily settlement/close before entering, to confirm where the close actually is and whether it is below the 10-day line.

Even if price closes above the 10-day line, do not rush to get bullish on silver above that level, because the risk in silver is currently very large; it may be better to watch gold, copper, and other commodities for opportunities near lower levels

At the same time, it is important to note that this decline does not necessarily confirm that gold and silver have definitively topped. There is that risk, but if Warsh suddenly signals a more dovish stance, the market could reverse again. Recent volatility is simply too high, so hedging should remain the first priority.

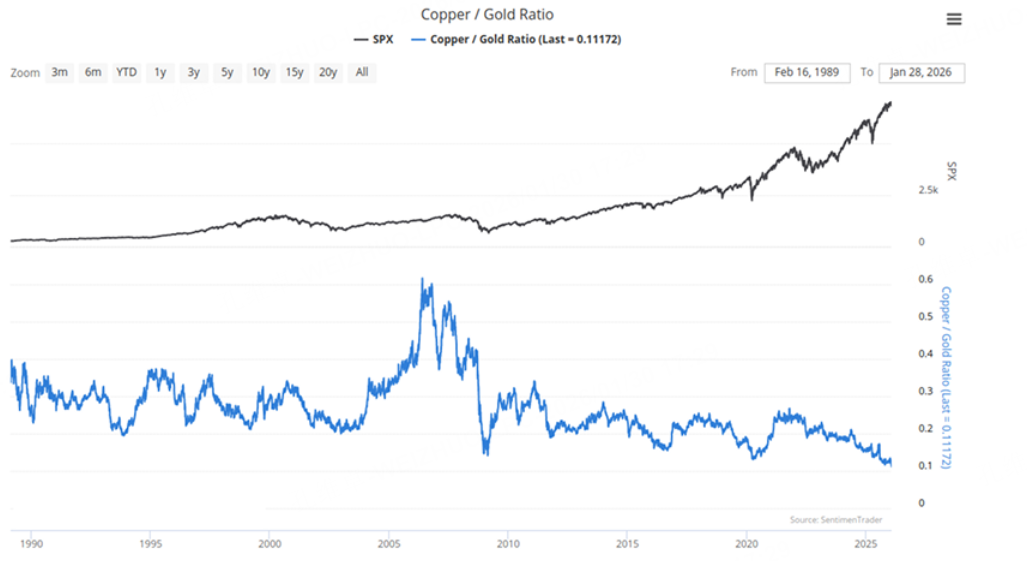

Historical backtest: gold may still rise; DXY stays weak

Based on our latest backtest, historically, after a sharp drop in the copper–gold ratio, gold has tended to have a high probability of rising, while the U.S. dollar index has tended to be relatively weak—reflecting a historical pattern.

$铜矿ETF-Global X(COPX)$ $COMEX铜主连 2603(HGmain)$

When the copper–gold ratio reaches the elevated levels shown above, historically, the probability that gold’s future returns are positive is high.

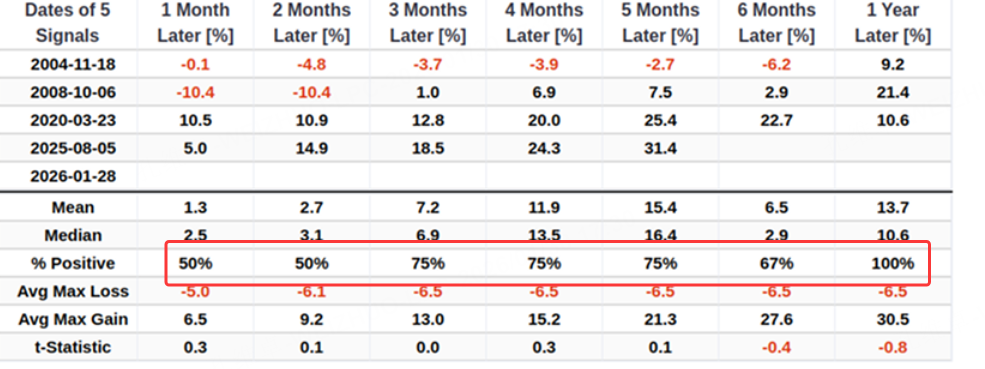

From a probabilistic perspective, gold historically showed a 100% likelihood of positive returns within 12 months after the signal was triggered, with a median return of 10.6%, implying that gold’s pullback cycle historically tends to be around two months.

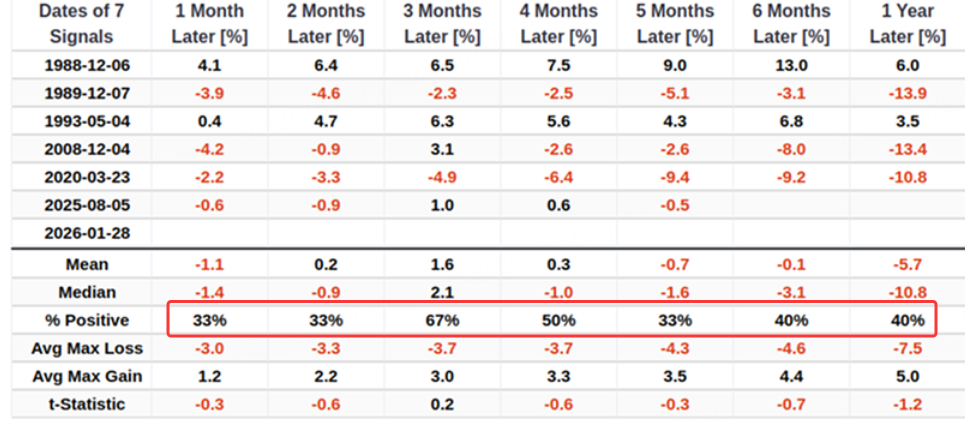

Meanwhile, the probability of positive returns for the U.S. dollar index is low across each horizon in the backtest, indicating that the dollar index is still likely to remain weak.

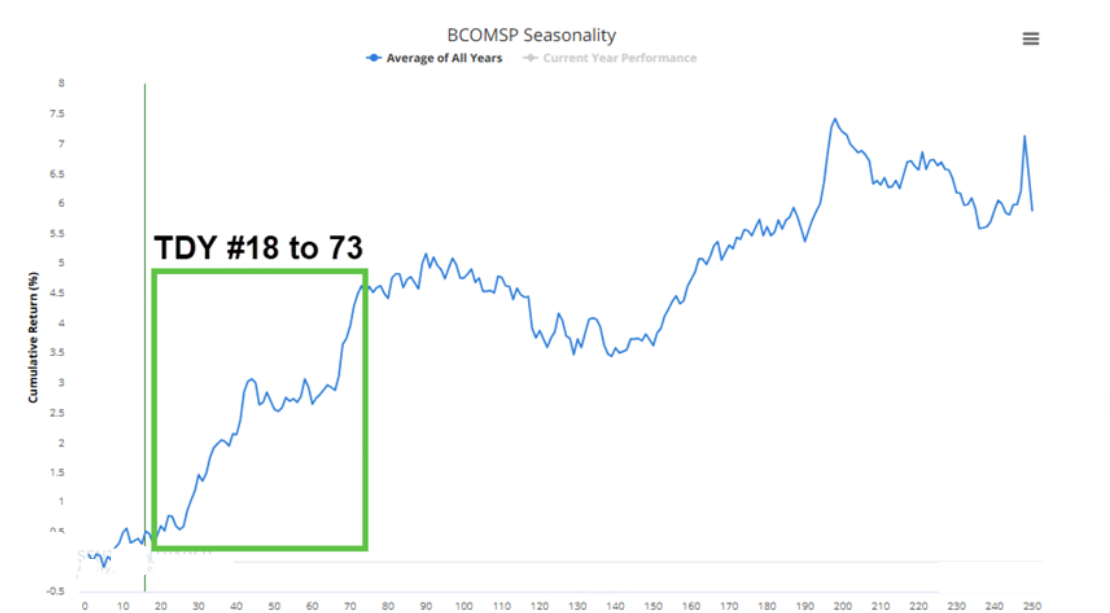

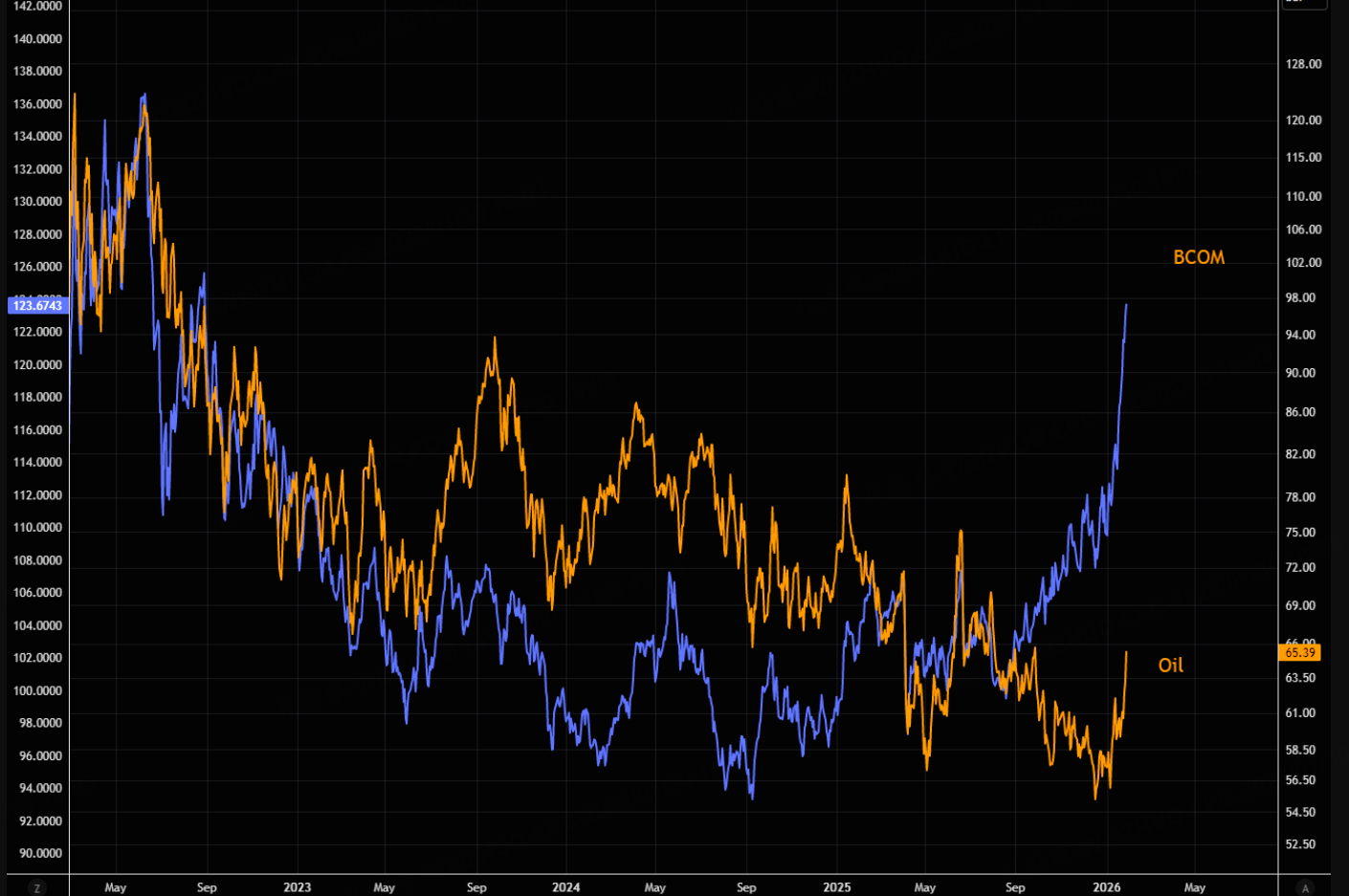

Commodities likely trend higher; oil and copper

In that case, commodities as a whole are more likely to move higher.

From the historical performance of the broad commodities index, the period from the Jan 28 close through Apr 17 tends to be seasonally strong, and February, March, and April are among the strongest months of the year.

$ProShares做空大宗商品ETF(SBM)$ $大宗商品做空ETN-Deutsche Bank(DDPXF)$

Within commodities, crude oil is a market that tends to move higher more easily, followed by copper.

$美国原油ETF(USO)$ $WTI原油主连 2603(CLmain)$ $小原油主连 2603(QMmain)$

Trading stance for now

That is all for today. Aside from the silver calendar spread, we can wait on gold for now, and after Warsh speaks, assess whether his tone is dovish or hawkish. If he is dovish, we can look for lower-level opportunities to get long and close the silver calendar spread, and we should not chase silver longs after that.

Comments

白銀和黃金價格走勢分析

Great article, would you like to share it?