Gold Collapse as Powell Flags Risk of Higher Peak,What Is The Next

Since November last year, There has been a strong rebound in gold prices at home and abroad, The driving force for the rebound of gold price comes from the market's expectation that the Fed's interest rate hike will slow down, and the nominal interest rate of the US dollar will fall at a high level.

When inflation falls slowly, the real interest rate of the US dollar will also fall, which reduces the opportunity cost of holding gold and stimulates the rebound of gold investment demand. Geopolitical crises such as Russia-Ukraine conflict also brought some safe-haven buying, which supported the rebound of gold prices.

In addition, the European Central Bank will raise interest rates stronger than the Federal Reserve in the future, which will also lead to the weakening of the US dollar exchange rate and support the gold price.

However, from the short-term "non-landing" of US economic growth, the high obstinacy of inflation and the later-than-expected end of the Fed's interest rate hike, this means that there may still be room for rebound in the real interest rate of the US dollar, which means that the rise of gold price will be limited, and it is difficult to see a new high in the short term.

Historically, the central bank's purchase of gold is not enough to change the pricing logic of gold, the safe-haven buying brought about by geopolitical crisis is unsustainable, and physical consumption is not the decisive factor of gold price trend, and investment demand determines the medium and long-term trend of gold. Therefore, in the case of real interest rate rebound, the decline in gold investment demand leads to the pressure of gold adjustment.

The US economy "does not land" and it is difficult for the Fed to end tightening in the short term

Weak consumer spending dragged down the downward revision of US GDP in the fourth quarter, but it still remained resilient and did not fall into negative growth. On February 23rd, the US Department of Commerce released the revised data (final value) of US GDP in the fourth quarter of last year. After seasonal and inflation adjustment, the real GDP grew at an annual rate of 2.7%, which was weaker than the initial value of 2.9% released in January.

The downward adjustment of consumer spending, which accounts for about 2/3 of the US economy, is the main reason for the downward adjustment of the final value. The US Department of Commerce explained that the service industry expenditure in consumer spending has increased, which is partially offset by the decrease of commodity expenditure. The increase in expenditure on services mainly comes from health care, housing and public utilities, while the decrease in expenditure on commodities is reflected in durable goods and jewelry.

However, US corporate spending was stronger than expected in the fourth quarter of last year, with non-residential fixed investment growing at an annual rate of 3.3%, higher than the initial value of 0.7%, mainly reflecting the company's investment in buildings, drilling platforms and other structures, as well as the increase in intellectual property expenditure. In the fourth quarter of last year, disposable personal income was revised up to 8.6% from the initial value, and the real disposable personal income after inflation adjustment increased by 4.8%, revised up by 1.5 percentage points from the initial value. Personal savings were also revised up in the quarter, and the personal savings rate, which measures the percentage of personal savings to disposable income, was 3.9%, which was revised up by 0.5 percentage points from the initial value, suggesting that the negative drag of US consumer spending on US GDP is still weak for the time being.

At present, American real estate is in a downturn, but manufacturing industry is not in trouble yet. U.S. factory and durable goods orders fell in January as spending shifted to services. The final value of durable goods orders in January decreased by 4.5% month-on-month, which was flat with the previous value; Factory orders fell 1.6% month-on-month in January, slightly better than expected.

As the job market is still tight, the superimposed household consumption has not yet experienced negative growth, which means that the inflationary pressure in the United States has not been completely lifted. The inflation index that has received much attention has been comprehensively revised. The core PCE price index in the United States increased by 4.7% year-on-year in January, higher than the 4.4% in December last year; The month-on-month increase was 0.6%, which was also higher than the previous value of 0.3%

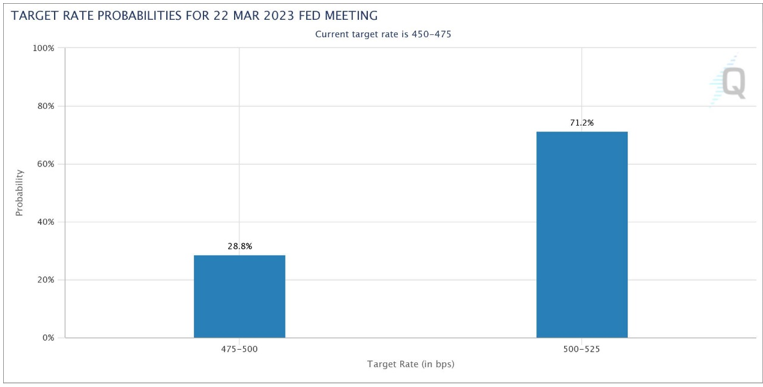

February's US CPI data is crucial, and any sign of sustained inflation may push the Federal Reserve to raise interest rates to a higher level than expected.

The recent higher-than-expected inflation data has intensified the pressure on the Fed to raise interest rates. Fed officials agree that interest rates should be higher and last longer at high levels. Inflation expectations, calculated by the yield of US inflation index government bonds, rebounded significantly in March and rose to 2.49% as of March 6.

On March 1st, Minneapolis Fed Chairman Kashkari, who has the right to vote at the FOMC meeting of the Federal Reserve Monetary Policy Committee this year, said that he is still "open" to whether to continue to raise interest rates by 25 basis points or accelerate the pace of raising interest rates to 50 basis points at the next FOMC meeting from March 21st to 22nd this year. Recent higher-than-expected inflation figures and a strong jobs report, these worrying data points suggest that we are not making progress as quickly as we had hoped.

The rebound of US dollar real interest rate inhibits the further rise of gold price

Before the end of the Fed's tight monetary policy, nominal interest rates such as US bond yields are still at a high probability. As of March 6, the yield on 2-year US bonds rose to 4.89%, after falling back to 4.06% on January 18; The yield of 10-year US bonds rose to 3.98%, after falling back to 3.37%.

In the context of the Fed's interest rate increase, even safer investment-grade companies have borrowed more than 5.7% on average in the bond market, compared with only 2% two years ago. While American companies with lower ratings pay an annual interest rate of about 9%, which is higher than the level of slightly less than 5% in March 2021.

Even if the Fed's interest rate hike is relaxed, the balance sheet of the Fed continues to shrink, which means that the liquidity environment of the US dollar will not return to easing because the Fed stops raising interest rates. In the week ending March 1, the balance sheet of the Federal Reserve was reduced to 8.39 trillion US dollars, after reaching a peak of 9.01 trillion US dollars.

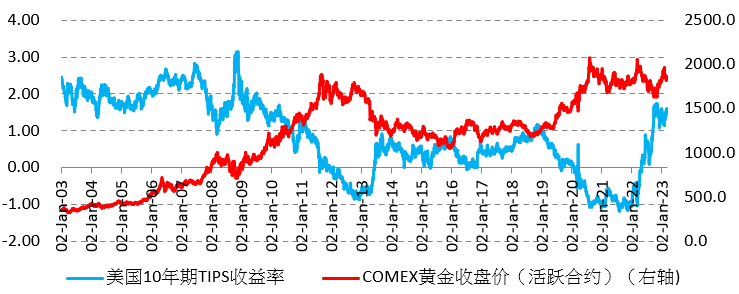

Therefore, under the tight liquidity environment of the US dollar, the real interest rate of the US dollar will have limited room to fall, and even when the Fed raises interest rates by 50 basis points in March, the real interest rate of the US dollar will rebound again. As of March 6th, TIPS yield, which reflects the real interest rate of US dollar in 10 years, rose to 1.49%, after falling to 1.14% on February 1st.

With the real interest rate of US dollar rebounding, the investment demand of gold fell again after a brief rebound in January and February. A recent research article by Erik Norland, executive director and senior economist of Chicago Mercantile Institute, clearly pointed out the relationship between the US dollar and the trend of gold price. "A weaker US dollar often boosts the price of gold. In the past 10 years, the price of gold has a consistent negative correlation with the Bloomberg Dollar Index."

The central bank's purchase of gold does not change the gold pricing model

Central banks, including China, have increased their holdings of gold in recent years amid ongoing changes in the dollar monetary system and concerns about the safety of dollar assets stemming from high inflation overseas and geopolitical crises. On March 7th, the statistics of the State Administration of Foreign Exchange showed that in February, the gold reserve was 65.92 million ounces, up 5.2% year-on-year and 1.2% quarter-on-quarter, which was the fourth consecutive month of increase. However, from the historical experience, the central bank's purchase of gold does not change the gold pricing model unless the global monetary settlement system is reconstructed. For example, after the collapse of the Bretton Deep Forest Monetary System in 1970s, the global gold price was greatly expressed.

In the short term, The "non-landing" of the American economy and the tight job market make it difficult for the inflation in the United States to fall quickly, the tightening cycle of the Federal Reserve to end, the nominal interest rate of the US dollar is at a high level, and the real interest rate of the US dollar, which is the opportunity cost of holding gold, also has room for rebound, which inhibits the investment and consumption of gold, thus inhibiting the further rise of gold prices. In the medium term, the future trend of gold depends on whether the US economy falls into recession and whether it will enter the cycle of interest rate cuts. The motivation to break through the previous high point is still insufficient.

Finally, let's talk about gold futures as a trading tool. Compared with other trading instruments, gold futures have a wide range of uses, such as diversifying investment portfolios and providing alternatives to gold bars, coins and mining stock investments; When the market fluctuates, gold futures quickly reflect the impact of political and economic events on gold prices, allowing investors to immediately manage risks and grasp more trading opportunities; In addition, it can hedge inflation risk or be used as currency.

Among the gold futures contracts, the Gold Futures Contract (GC) of Chicago Mercantile Exchange is one of the global gold pricing indicators, with abundant liquidity and an average daily trading volume of nearly 27 million ounces; In addition, electronic trading in the past 24 hours makes it easier to manage positions when global news and events affecting gold prices occur. Because the futures contract is closely related to the spot market, the gold futures of Zhishang Institute are settled in kind, which can reduce the sliding point cost; At the same time, it can also achieve higher capital efficiency, because participating in metal futures trading on an exchange can control larger nominal value futures contracts at a lower cost and enjoy margin concessions (margin requirements are reduced by & gt; 80%).

In addition to standard gold futures contracts, Chicago Mercantile Exchange also provides smaller mini gold futures contracts (QO) and mini gold futures contracts (MGC), so that investors have more choices, flexibly manage capital positions and implement more investment strategies.

$E-mini Nasdaq 100 - main 2303(NQmain)$ $E-mini Dow Jones - main 2303(YMmain)$ $E-mini S&P 500 - main 2303(ESmain)$ $Gold - main 2304(GCmain)$ $Light Crude Oil - main 2304(CLmain)$

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- mrzhuge·2023-03-10wowLikeReport

- Penthon·2023-03-10fightLikeReport

- Simonnov·2023-03-10IcLikeReport

- Plan R·2023-03-10OkLikeReport

- Kelistine·2023-03-10👌LikeReport

- roskee·2023-03-10thanksLikeReport

- JianHong96·2023-03-10okLikeReport

- HL Chua168·2023-03-10GoodLikeReport

- FK1234·2023-03-10💪LikeReport

- MGOH·2023-03-10okLikeReport

- Stockkid·2023-03-10goldddddddLikeReport

- YKent·2023-03-10👍🏻LikeReport

- 诚信是金rdl·2023-03-10okLikeReport

- AnT·2023-03-10OkLikeReport

- JYChew·2023-03-10okLikeReport

- Nlatykislove·2023-03-10[Smile][Smile][Smile]LikeReport

- Cory2·2023-03-09ThanksLikeReport

- H.P·2023-03-09👍👍👍LikeReport

- WooSM·2023-03-09LkLikeReport

- 农民人士·2023-03-09OkLikeReport