Is Trump Publicly Backing a Weaker Dollar? AreThe Dip Buyers Ready For The Market Soaring?

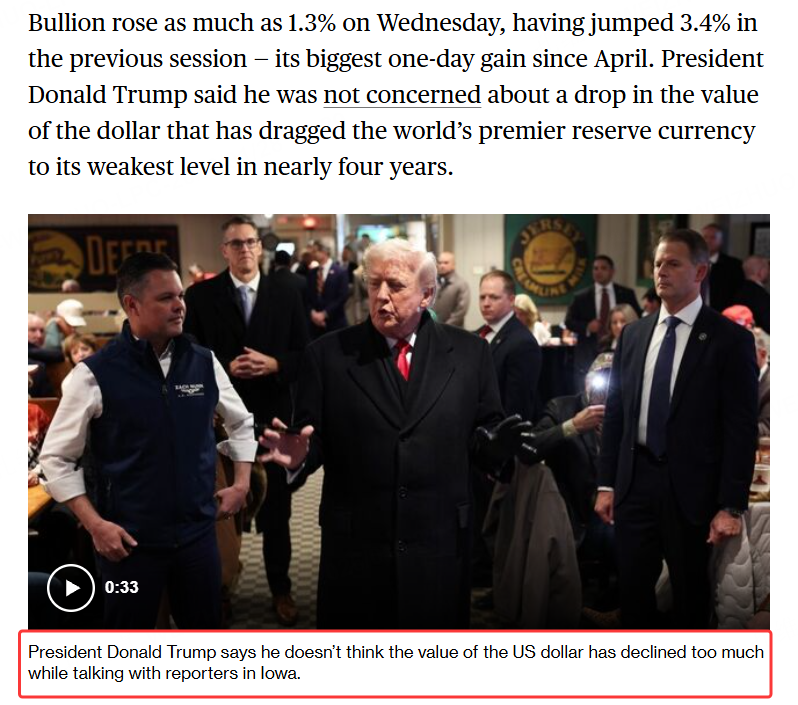

Earlier this Tuesday, a U.S. financial journalist asked President Donald Trump a question that has broadly worried Wall Street: “Are you concerned about the recent decline in the U.S. dollar?”

Trump’s response surprised the market: he said no, he thought it was great, and that the dollar should be allowed to find its own level because that is “fair”—adding that if you look at China and Japan, they always want their currencies to depreciate.

In market reporting, bullion rose as much as 1.3% on Wednesday after jumping 3.4% the day before (its biggest one-day gain since April), and Trump said he was not concerned about a weaker dollar even as the world’s premier reserve currency slid to its weakest level in nearly four years.

This statement clearly reads as tacit approval—or even welcome—for dollar weakness, and the interview content reshaped the underlying logic of the FX market overnight.

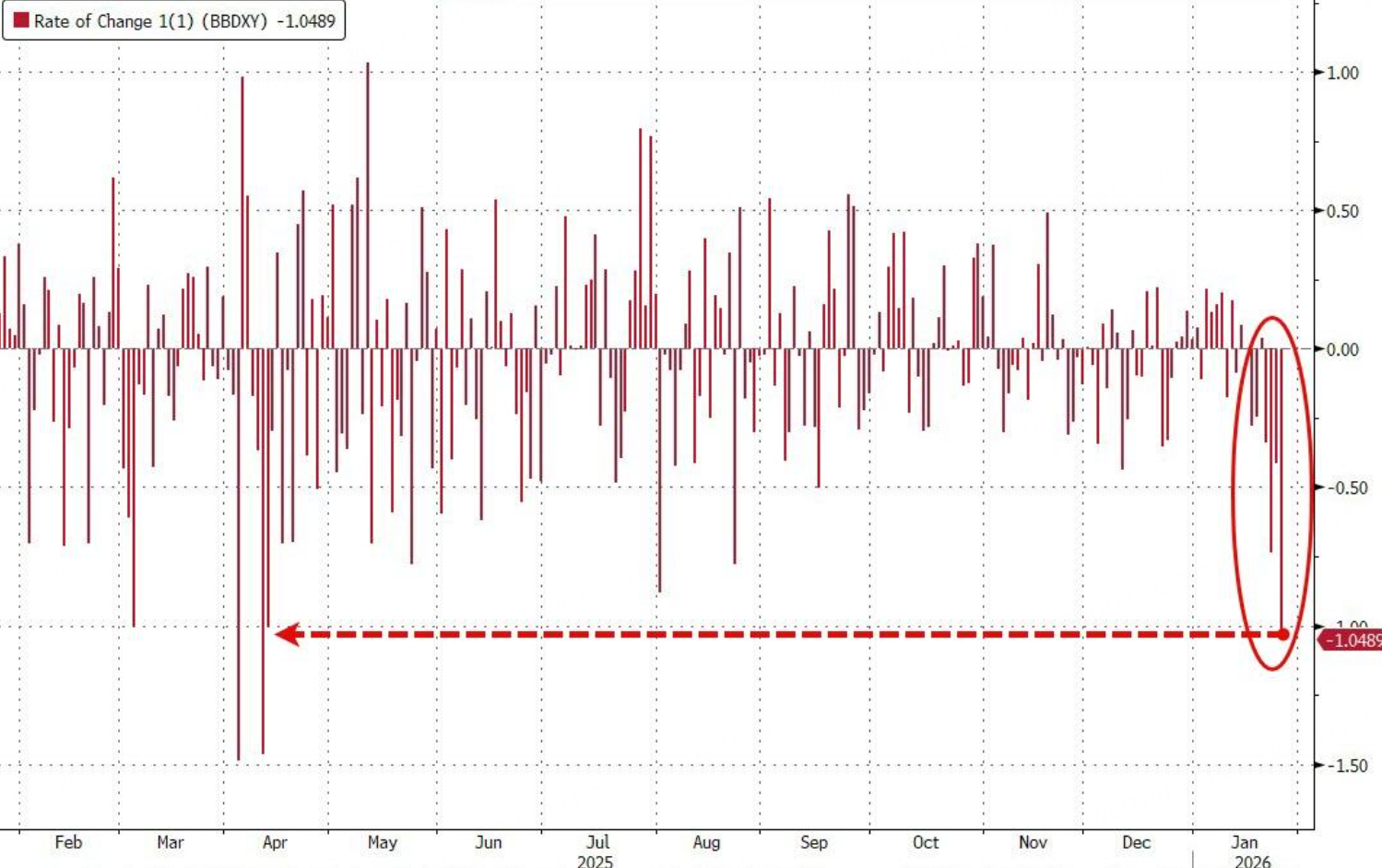

The Bloomberg Dollar Index dropped 1.2% in response, marking its biggest one-day decline since last year’s tariff-threat episode.

Technical risk: the dollar index looks dangerous

From a technical perspective, the U.S. dollar index is in a very precarious position right now; if the selloff accelerates and it crosses a technical “cliff,” it could set the main theme for global asset allocation for a long time to come.

$美元指数(USDindex.FOREX)$ $做空美元指数-PowerShares(UDN)$ $新兴市场美元国债ETF-Vanguard(VWOB)$ $美元ETF-PowerShares DB(UUP)$

Will the dollar “fall off the cliff”?

Although “a strong dollar equals a strong America” used to be a popular market belief, Stephen Jen (the former Morgan Stanley FX strategist who proposed the well-known “dollar smile theory”) recently wrote that we are entering a new historical phase: the U.S. economy remains strong, yet the dollar is weakening, signaling a new stage of depreciation, and the Trump administration’s objective is an exchange rate that benefits U.S. exporters.

I previously believed Trump’s disruptive actions were meant to support U.S. Treasuries and, by extension, push the dollar index higher, but recent market direction appears to indicate something else—namely that Trump prefers a weaker-dollar environment, and that regardless of whether the dollar index weakens, Treasury prices may not spiral out of control, likely due to a tacit understanding between Trump and major Treasury-holding countries: tariffs won’t be raised lightly, and those countries won’t dump Treasuries lightly either.

If Treasury prices can remain stable, then a weaker dollar index aligns with what the Trump administration wants—reviving manufacturing and exports. An overly strong dollar hurts exporters’ trade and also works against narrowing the trade deficit, and a dovish Federal Reserve is another factor that could drive a sustained depreciation in the dollar index

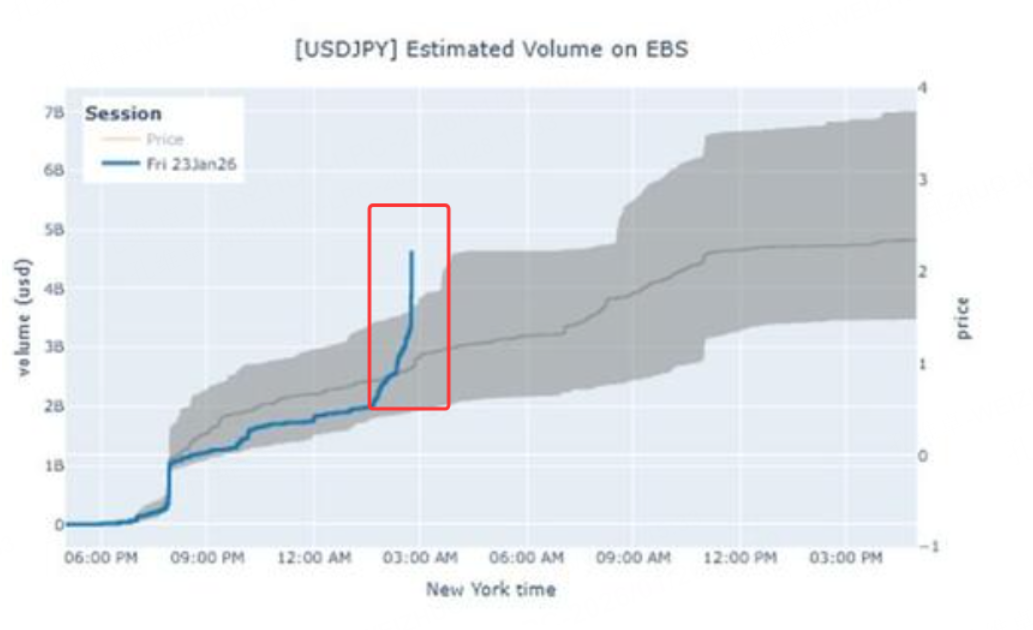

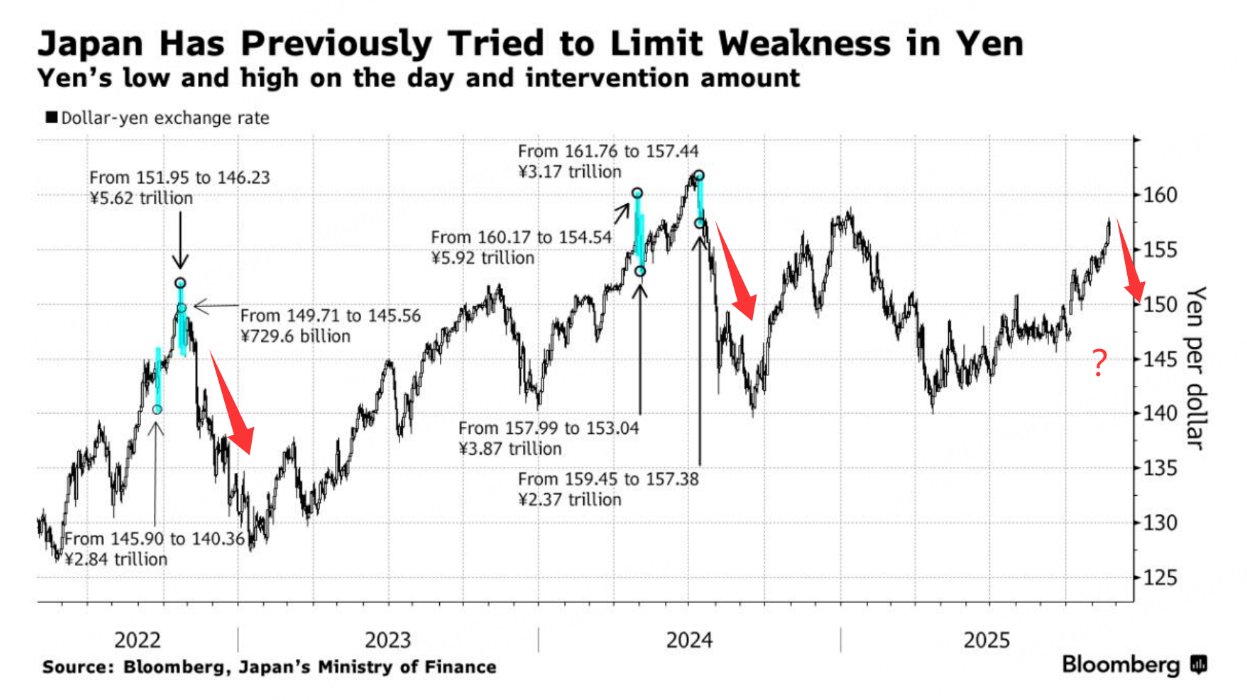

At the same time, note that during the previous sharp drop in the dollar index, yen trading volume surged unusually, and the yen also rallied strongly.

On Monday, when the dollar and the yen swung this sharply, FX traders received a “rate-check” inquiry from the Bank of Japan; the market typically treats such inquiries as a signal of potential government intervention in the yen, and after the last two interventions, the yen moved into a sharp appreciation trend.

So we need to be careful: if FX pricing shifts toward a weak-dollar regime, then after Trump’s repeated “TACO” behavior leads the dollar index to break down technically, the decline could accelerate, pushing USD/JPY lower (i.e., yen strength), and in that case the ongoing uptrend in gold, silver, commodities, and even U.S. equities plus Hong Kong/China A-share assets could continue.

$CME日元日经主连 2603(NIYmain)$ $SGX日经主连 2603(NKmain)$ $日元ETF-ProShares两倍做空(YCS)$ $日元ETF-CurrencyShares(FXY)$

But if the dollar index does not break down, instead bases at these lows and rebounds, then the rally in those assets could face turbulence.

Overall, the dollar index has recently become a key anchor for the direction of global-asset volatility, and it matters a great deal!

So if the dollar index remains weak, what opportunities can we consider participating in?

Opportunity 1: Gold, silver, and crude oil

When confidence in fiat currency wobbles, hard assets become a safe haven, and the market has already responded in a dramatic way: gold has broken above the historic level of USD 5,200 per ounce and is up about 20% year to date, while silver has been even more aggressive, surging more than 50%

For gold and silver, I still hold my prior view: until the issue of insufficient deliverable supply for March silver delivery is resolved, silver is unlikely to drop easily, so we can use the 5-day moving average as an entry reference—if silver breaks below the 5-day line, bulls stop out; as long as it holds above the 5-day line, continue to stay bullish on silver futures.

$白银主连 2603(SImain)$ $迷你白银主连 2603(QImain)$ $白银2603(SI2603)$ $白银ETF-iShares(SLV)$

For gold, as long as the dollar remains weak—and as long as S&P futures do not break below the 20-week moving average and trigger a liquidity crisis—gold should also be unlikely to fall sharply; similarly, treat the 5-day line as the bullish stop level.

$黄金主连 2602(GCmain)$ $微黄金主连 2602(MGCmain)$ $1盎司黄金主连 2604(1OZmain)$

Crude oil

A weaker dollar reduces the cost of buying raw materials, and when you add strong demand for energy and metals from the technology sector (especially AI compute/data-center buildouts), plus the fact that recent U.S.–Iran tensions have not been fully resolved, commodities are sitting in a dual tailwind environment.

Crude oil and copper are also benefiting under this backdrop, and anyone positioned to go long commodities should not miss the opportunity; for oil, we follow the prior approach and use the 60-day moving average as the bull-bear boundary for WTI crude.

$美国原油ETF(USO)$ $WTI原油主连 2603(CLmain)$ $小原油主连 2603(QMmain)$ $原油ETF-PowerShares(DBO)$

If WTI breaks above the 60-day moving average, then try a bullish calendar-spread strategy—go long the near-month contract (for example, March) and short the far-month contract (for example, June)—to express a bull-market time-spread arbitrage.

Opportunity 2: Hong Kong A assets and the RMB

As the dollar weakens, capital begins to flow back from the U.S. into emerging markets, and the rise in the Bloomberg Asian Dollar Index along with new highs in the MSCI Emerging Markets Currency Index both support that

$美元/离岸人民币(USDCNH.FOREX)$ $CME人民币主连 2603(UCHmain)$ $恒生指数(HSI)$ $恒生科技指数(HSTECH)$ $南方恒生科技(03033)$ $恒生科技ETF(03032)$ $恒生科技指数主连 2601(HTImain)$ $恒生指数主连 2601(HSImain)$

Within this logic chain, Hong Kong equities and China-related assets become potential biggest beneficiaries, and the PBoC’s substantial upward adjustment to the RMB daily fixing shows regulatory confidence.

Wee Khoon Chong (Senior Market Strategist for Asia-Pacific at BNY) noted that dollar weakness is the key catalyst for strength in the Asia-Pacific FX market and that sustained capital inflows are occurring; for Hong Kong stocks, improving liquidity and easing FX pressure form a solid foundation for upside.

We can also watch the current price action of Hang Seng Index futures: there are signs of a basing breakout, so we can stay bullish for now and simply use the daily breakout level as the loss stop point—if price falls back below the prior breakout area, stop out immediately.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.