Recently, the Hang Seng Index has surged for three consecutive days, capturing the attention of many traders. Analysts attribute this rally to better-than-expected macroeconomic data from mainland China, an earnings recovery in tech stocks driven by the AI boom, and a short-term easing of geopolitical risks in the Middle East. However, against the backdrop of this continuous surge, authoritative institutions warn that the Hong Kong stock market still faces deep-seated tail risks from resurging inflation and foreign capital flight beneath the surface of this rebound. We will now discuss whether it is advisable to chase the current rally in the Hang Seng market.

$A50指数主连 2603(CNmain)$ $恒生指数主连 2603(HSImain)$ $恒生科技指数主连 2603(HTImain)$

Let’s take a look back at the underlying logic of how the U.S. stock market operates:

Drivers Behind the Hang Seng's Surge

The recent strong rebound in Hong Kong stocks is driven by a combination of fundamental and capital flow factors. Economic activity data from mainland China for January and February, including industrial production and retail sales, exceeded expectations. Coupled with strong financial reports from tech giants and the momentum of the AI wave, market sentiment has significantly recovered. Furthermore, expectations of Sino-US mediation to reopen the Strait of Hormuz have eased risk aversion, and the "positive delta" buyback effect resulting from the closing of put options in the derivatives market has provided a crucial technical floor for the index.

Despite this strong short-term performance, institutions like Goldman Sachs point out that crude oil supply disruptions caused by the US-Iran conflict could keep oil prices elevated. This would exacerbate inflation and impose a "heavy tax" on global economic growth, thereby severely suppressing the valuation of Hong Kong stocks. Simultaneously, the inflation rebound has triggered an extreme "hawkish repricing," and surging real yields on US Treasuries have led to a frantic withdrawal of global systemic funds from equity markets. This creates a massive liquidity drain on the Hong Kong market, which is highly sensitive to foreign capital, suggesting that we should approach the current rally with caution.

$SP500指数主连 2606(ESmain)$ $道琼斯指数主连 2606(YMmain)$ $NQ100指数主连 2606(NQmain)$

The Shadow of the Oil Crisis

The most obvious and imminent danger currently hanging over equity markets—especially the highly foreign-capital-sensitive Hang Seng Index—is the disruption of oil and gas supplies triggered by the US-Iran war. According to Goldman Sachs' modeling, if global crude production remains constrained for 21 days and recovers slowly over the subsequent 30 days, Brent crude will stay at an elevated $98 per barrel from March through April. With this "21-day deadline" expiring this Saturday, current risks clearly tilt toward a delayed supply recovery.

Time is the market's greatest enemy right now, as the longer the geopolitical conflict drags on, the worse the trade-off between inflation and economic growth becomes. Historically, during severe oil supply crises—such as the 1973 Arab oil embargo, the 1979 Iranian Revolution, and the 1990 Gulf War—the S&P 500 dropped by an average of 12% during oil price spikes, with a median peak-to-trough decline of 23%. When the global economy faces the "heavy tax" exploitation of high oil prices, Hong Kong stocks, as an offshore market, cannot remain immune in terms of their corporate earnings expectations and valuation anchors.

$WTI原油主连 2605(CLmain)$ $小原油主连 2605(QMmain)$ $天然气主连 2604(NGmain)$

The Strongest Tightening Shock Since 2023

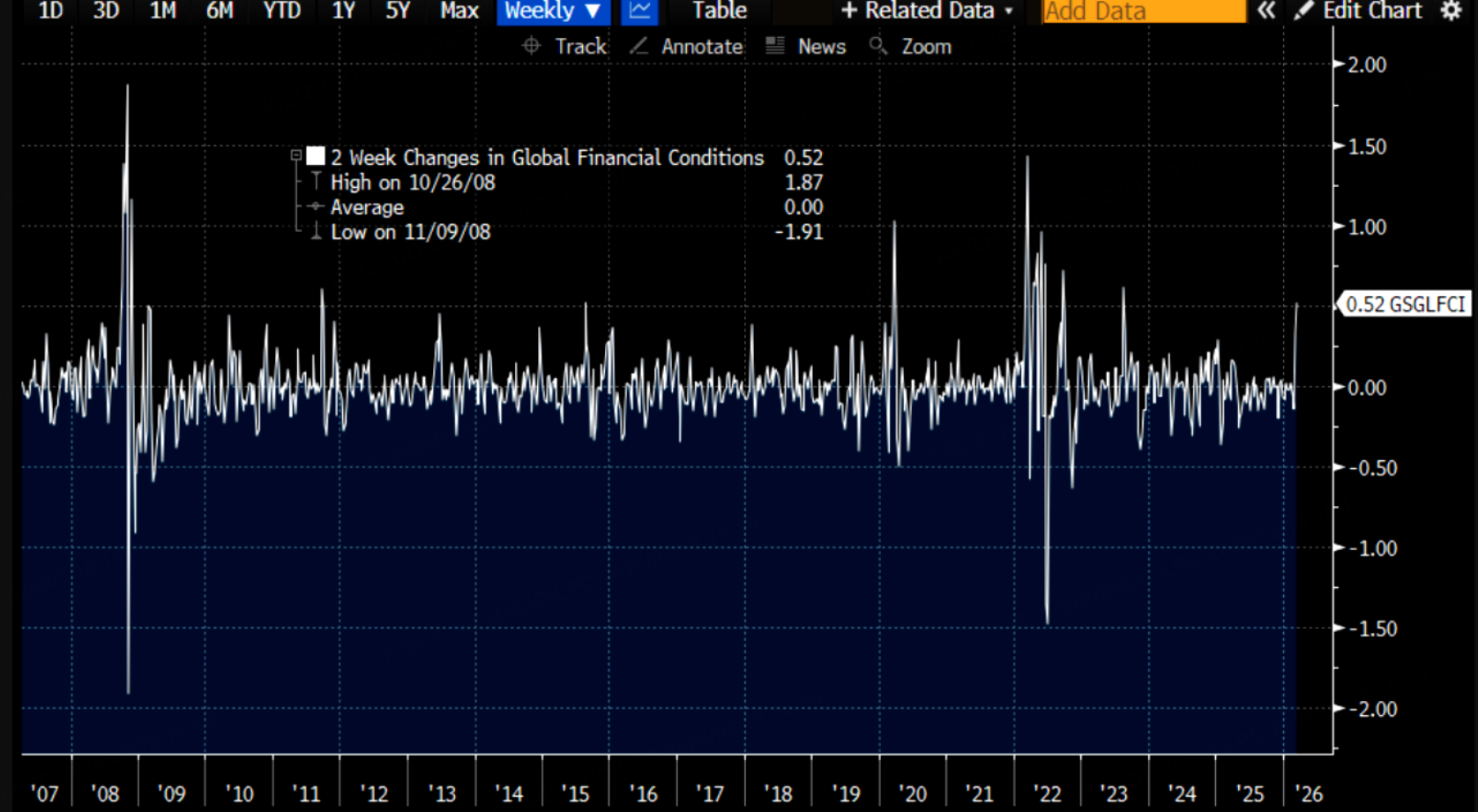

The resurgence of inflation expectations has led to a sharp reversal in the global macroeconomic narrative. Over the past two weeks, the previously solid "dovish consensus" has completely collapsed, and rate cut expectations were quickly priced out. The market has experienced its most dramatic "hawkish repricing" since 2000, with the Goldman Sachs Global Financial Conditions Index (GS Global FCI) spiking by over 50 basis points in a short period, marking the most intense tightening wave since August 2023.

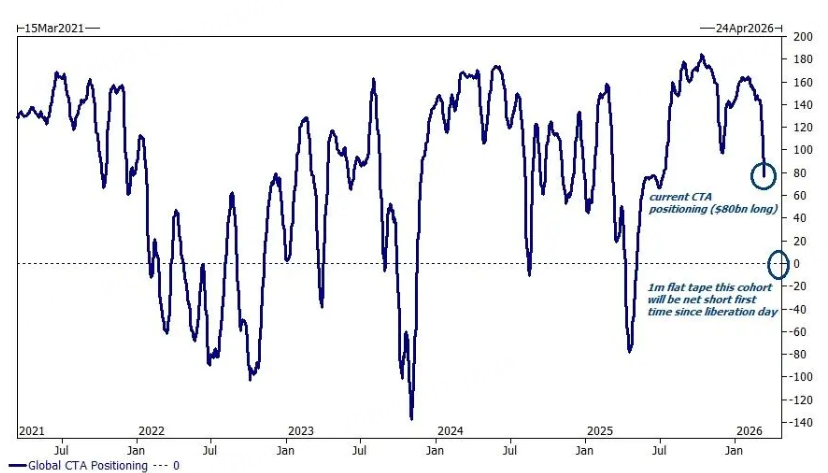

Under this extreme tightening, 10-year real interest rates in G4 countries, especially US Treasury yields, have surged, causing the sensitivity (beta) of equities to real rates to turn universally negative. Accompanying the spike in risk-free rates, global systemic funds are frantically fleeing. Data shows that Commodity Trading Advisors (CTAs) and trend-following funds have dumped about $80 billion in global equities over the past month, with another $100 billion sell-off expected in the coming month. Furthermore, the notional value of index futures sold by asset managers hit a 10-year high of $36.2 billion, and short positions in macro products are nearing the 97th percentile extreme of the past five years. A capital retreat and shorting force of this magnitude will inevitably create a massive liquidity drain on the Hang Seng Index.

Given such a harsh macroeconomic environment, why haven't global stock markets, including the Hang Seng Index, experienced a straight-down crash ? The answer lies in mechanical hedging within the derivatives market. During a slow decline, high volatility forces many funds to reduce their overall positions. As total risk exposure drops, the large number of put options previously established for downside risk hedging are no longer needed. When these put options are closed out, it is equivalent to buying back "positive delta" in the market, and this offsetting capital flow has actually acted as a buffer that supports the index's bottom line. However, this technical support born out of "deleveraging" is extremely fragile; once a support level, such as 6,600 points on S&P futures, is broken, selling pressure will snowball.

$黄金主连 2604(GCmain)$ $微黄金主连 2604(MGCmain)$ $1盎司黄金主连 2604(1OZmain)$

Conclusion and Outlook

In summary, the core variables currently driving global markets have yet to show substantial improvement. Although Goldman Sachs predicts that earnings growth will persist in the long run, increasing cash reserves and reducing portfolio risk is the wise move in today's complex environment. Projecting this logic onto the Hong Kong stock market, we can conclude that since the upward trends in crude oil and US Treasury yields may not be entirely over, this poses a significant downside risk for the Hang Seng Index. However, as long as navigation through the Strait of Hormuz can be restored, the US dollar index will fall due to the retreat of safe-haven flows, which would once again stimulate a rally in the Hang Seng. Ultimately, while the Hang Seng has seen short-term gains due to the AI wave and a slight easing of risks in Hormuz, its long-term trajectory will still depend on the evolution of the US-Iran war and the US dollar index.

Comments

Great article, would you like to share it?